Application of econometric modeling techniques for foreign exchange rate forecasting

Free access

In a turbulent economic environment, being able toforecast the direction of exchange rates is a key factor behind hedging, investment, financing and capital budgeting decisions. The article focuses on the application of econometrics and mathematical modelling techniques for the purpose of forecasting foreign exchange rateы. A Support Vector Regression Model is used to produce a USD/RUB exchange rate forecast for the first quarter of 2016. The model proves to have high predictivepower, and therefore it might be of great use for FX market traders, investors and speculators.

Econometric model, foreign exchange rate, exchange rate forecasting, regression analysis, support vector regression (svr), support vector machine (svm)

Short address: https://sciup.org/140124627

IDR: 140124627

Text of the scientific article Application of econometric modeling techniques for foreign exchange rate forecasting

INTODUCTION

Many entities have an interest in being able to forecast the direction of exchange rates. Whether you are a business or a trader, having an exchange rate forecast to guide your decision making can be very important to minimize risks and maximize returns. Exchange rate forecasts are a key factor for a wide variety of decisions taken by businesses, including: hedging decisions, shortterm financing decisions, short-term investment decisions, capital budgeting decisions, earnings assessments, and long-term financing decisions. [7]

What is more, exchange rate forecasting is very important to evaluate the benefits and risks attached to the international business environment. International transactions are usually settled in the near future; therefore, exchange rate forecasts are necessary to evaluate the foreign denominated cash flows involved in international transactions. [8]

Over the recent years, forecasting the exchange rates has become a burning issue for the Russian economy: in November 2014, the Bank of Russia took a step towards a free float ruble by abolishing the dual currency soft peg, as well as automatic interventions. [6] At present, Russia employs a floating exchange rate regime, which means that the ruble exchange rate against foreign currencies is set by the market, i.e. the ratio between the demand for foreign currency and its supply in the FX market. Any factors disturbing this ratio initiate exchange rate fluctuations.

The Bank of Russia’s decision to set the rate free came only days after the rouble had suffered its biggest weekly drop in 11 years, amid fears that Russia could face a self-fulfilling currency crisis. After that, the ruble became extremely volatile. In June, the ruble’s three-month implied volatility, a measure of exchange-rate swings, was at 20 percent, the highest globally, according to data compiled by Bloomberg. [5] Throughout the year, the “price” range of dollar was from 49 to 70 rubles. In a turbulent economic environment like this, a reliable exchange rate forecast would increase the confidence of Russian businesses; it would also contribute to the accuracy, reliability and efficiency of micro- and macroeconomic planning and forecasting.

However, forecasting the exchange rate is a huge problem. Firstly, it is not clear what factors are the key determinants of the exchange rate. Exchange rate dynamics may be influenced by changes in export and import prices, inflation levels and interest rates in Russia and other states, economic growth rates, investors’ sentiment and expectations in Russia and world-wide, changes in monetary policies pursued by central banks in Russia and other countries. [10] Clearly, it is practically impossible to account for all of them. Moreover, the accuracy and reliability of exchange rate forecasts based on commonly used forecasting models (particularly linear ones) is really doubtful. In fact, many researchers point out that short-term movements in exchange rate are unpredictable and cannot be projected in a systematic fashion. [2] The situation in the Russian foreign exchange market in 2015 seems to provide the perfect opportunity to check whether some modern mathematical modelling techniques actually work in a turbulent environment and can resolve the problem of exchange rate forecasting.

METHODOLOGY

Deciding which of thousands of market signals to ignore and which to act on poses a challenging problem which potentially lends itself well to techniques in machine learning. Support Vector Regression models, also known as Support Vector Machines, have been shown to outperform a number of learning algorithms in FX prediction [9]. The nonlinear predictive power and input size independent generalization error afforded by SVMs make them well suited to high dimensional classification problems [9]. Of the learning algorithms applied to FX forecasting in the literature, hybrid combining models, such as Genetic Algorithm SVMs, achieve the best overall results. On theoretical grounds, it has been shown that SVMs have a few interesting properties which may support the notion that SVMs generally perform better than ANNs. However, on empirical grounds, based on experimentation results, no solid conclusion could be drawn regarding which model performed the best on the EUR/USD data set. [1] Therefore, I decided to apply support vector regression to see whether it yields adequate results. To measure the accurateness of the forecast, I used the root mean standard error (RMSE). In fact, RMSE is the most popular indicator which enables researchers to see whether the model produces accurate forecasts; the higher the RMSE, the less accurate the forecasting model. [8]

The basic idea of the SVM is finding a maximum margin classifier that separates a training set between positive and negative classes, based on a discriminant function that maximizes the geometric margin. The model selection for the prediction models is generally based on the bias-variance dilemma, which denotes the trade-off between the amount of variation within different estimators on different values of a specific data set (variation) and the difference between the estimator’s expected value and the true value of the parameter being estimated (bias). [1]

Although SVM was originally introduced for classification purposes, SVMs can easily be extended to the task of regression and time series prediction, for which the focus of this research lies on. The constrained optimization problem is transformed to minimizing a certain cost function q as a function of the soft-margin constant C. This cost function q has at most Е deviation, also known as the tube size of the SVM, from the actual values Уг for all JC^. The cost function is defined as [1]:

The vector is the predicted outcome for the desired outcome У1 . If the absolute difference between the predicted outcome and the desired outcome is equal or larger than £ , measured by the ε-insensitive loss function ^(У^У?) , the penalty function C^.L^yO , also known as the empirical risk , increases and penalizes that error by the amount of the soft-margin constant C . Introducing the slack variables ^ i and Kt , that denote errors larger than +s and —£ respectively, the constrained optimization problem is now defined as [1]:

у, 4- (w. %t) + Ь4< е + £

fw > 0

I performed SVR analysis in R Statistics (using CRAN e1071 package). I used the USDRUB_TOD as the index for my analysis. USDRUB_TOD is the instrument which enables the trader to buy or sell US dollars (in lots) for Russian rubles, with the deal being executed on the day of trading (“today”). That’s one of the most short-term instruments on MOEX.

The input range for the model included 226 observations of the daily closing values of USDRUB_TOD in 2015. The summary statistics of the dataset is given in Table 1.

Table 1. SVR model input statistics

|

Data type |

closing USDRUB_TOD, daily |

|

Number of observations |

226 |

|

Mean value, RUB |

61.57 |

|

Daily volatility (standard deviation), % |

1.81 |

Sources: MOEX official website, author

These values were used as a training dataset of n = 226 points. The result was a non-linear fitted line with a root mean squared error of approximately 1.68 rubles, which is a really good fit. However, that was the untrained version. In order to improve the performance of the support vector regression, I tried to select the best parameters for the model. Initially, I performed an epsilonregression, but I did not set any value for epsilon, so it took a default value of

0.1. There is also a cost parameter which can be changed to avoid overfitting. [3] Therefore, I used the grid search method, that is – trained a lot of models for the different couples of epsilon and cost, improving the RMSE, and chose the best one. The trained model has the following properties:

-

• SVM-Type: eps-regression

-

• SVM-Kernel: radial

-

• cost: 256

-

• gamma: 1

-

• epsilon: 0.1

-

• Number of Support Vectors: 142

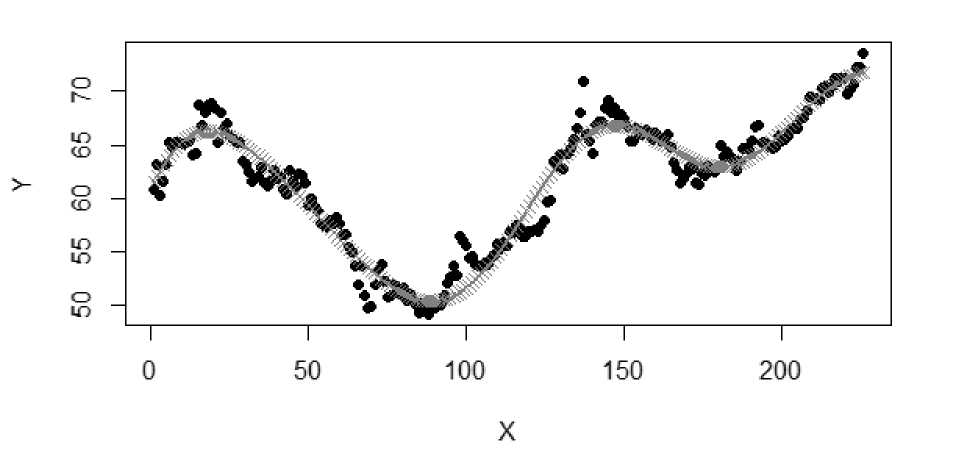

Training enabled to improve the accuracy of the fit: RMSE of the tuned model was 1.47 rubles. The tuned SVR model is depicted on Chart 1.

Chart 1. Tuned SVR model

Source: author

Finally, the tuned model was used to generate a forecast for the first quarter of 2016. The input values included 62 USDRUB_TOD observations; the summary statistics of the dataset is presented in Table 2.

Table 2. Tuned SVR model forecast input statistics

|

Data type |

closing USDRUB_TOD, daily |

|

Number of observations |

62 |

|

Mean value, RUB |

74.46 |

|

Daily volatility (standard deviation), % |

1.81 |

Source: MOEX official website; author

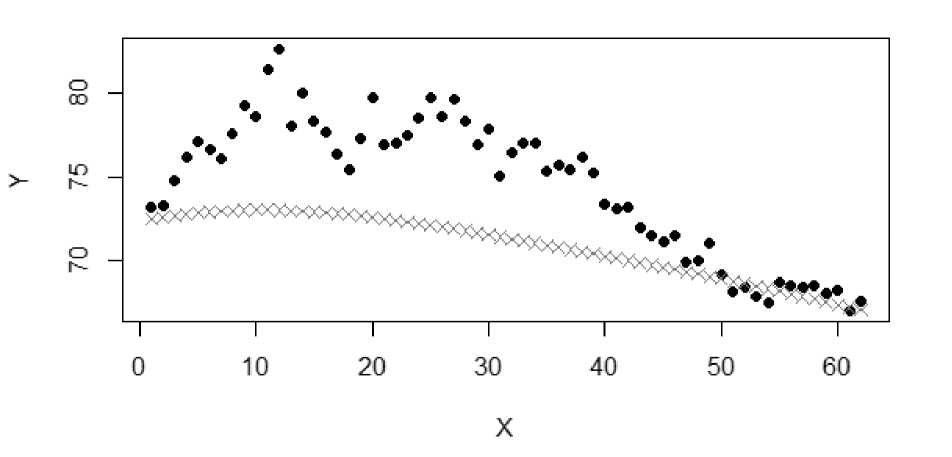

These input values were put to the tuned SVR model to produce the projected values of Y. The forecast is plotted against the actual data on Chart 2.

Chart 2. Testing the SVR model: forecasted & actual values for Q1 2016

Source: author

As follows from the chart, the model produces a non-linear range of predicted values for USDRUB_TOD for the first quarter of 2016. On the whole the predicted values are a bit less than those observed in reality, but the fitted line matches the general trend and the forecast for the end of the quarter matches the reality in a pretty accurate manner. The RMSE of the forecast equals 5.68 rubles.

CONCLUSION

As follows from my empirical research, Support Vector Regression model provides rather accurate exchange rate forecasts – even in an extremely turbulent environment. This technique provides an opportunity to overcome the problem of selection of factors that should be included in the model and at the same time involves complex algorithms to achieve the best results. The model also does not depend on the quality of inputs and does not contain intrinsic contradictions. Previous research indicates that feature and kernel selection are key determinants of an SVM's predictive power. [1]

It should be noted, however, that SVR models appear to be the most efficient in the short-term or mid-term horizons, particularly when the testing sample is small. Therefore, the quantity of input points might affect the results. To apply the model for long-term datasets, one should make sure that the training set is sufficiently large for the model to provide adequate results. In addition, although the exchange rate values predicted by the SVR model are really close to the actual figures, the model still tends to soothe extremities and level off harsh swings in the market trend. Moreover, the model developed in this article is a time series one: rather than reflecting some economic laws or relationships, it just matches the trend over time. Therefore, it cannot be used for analyzing key factors that determine the exchange rate, as well as for regulatory or policy making purposes. However, it is a very handy method for traders, speculators, FX market analysts and all other economic agents that require a reliable exchange rate forecast. Thus, I strongly believe that new complex forecasting techniques for foreign exchange rate forecasting, like SVR, have a bright future ahead of them.

References Application of econometric modeling techniques for foreign exchange rate forecasting

- Alamili, M. Exchange Rate Prediction using Support Vector Machines//LAP LAMBERT Academic Publishing. 2011.

- Department of Treasury and Finance of Western Australia. Exchange Rate Forecasting Review//Government of Western Australia. 2009.

- Kowalczyk A. Support Vector Regression with R, 2014//SVM Tutorial

- Ping-Feng Pai, Chih-Shen Lin, Wei-Chiang Hong, Chen-Tung Chen A Hybrid Support Vector Machine Regression for Exchange Rate Prediction.//Information and Management Sciences. 2006.

- Robinson J. Russia Free-Float Skeptics Gather as Ruble Seen on Shorter Leash//Bloomberg. 2015.

- Russian Central Bank declares change in policy and lets ruble float freely//Russia Beyond the Headlines. 2014.

- Suslov, M., Tregub, I. Modeling the currency exchange rate. Methods and principles//Economics. 2015. №1. pp. 67-70

- Susmel R., Kalimipalli M. Switching Stochastic Volatility and the Short-Term Interest Rates//Journal of Empirical Finance. 2004. №11.

- Ulrich C., Seese D., Chalup S. Foreign Exchange Trading with Support Vector Machines, Advances in Data Analysis//Berlin. 2007.

- Политика валютного курса Банка России//Официальный сайт Банка России. 2015.