Issues of introducing a basic income into the Russian national pension system

Author: Bobkov V.N., Zakharov I.N., Sherstobitova Yu.A.

Journal: Economic and Social Changes: Facts, Trends, Forecast @volnc-esc-en

Section: Theoretical and methodological issues

Article in issue: 1 т.19, 2026.

Free access

This study aims to develop the provisions of the basic income concept for its application within the pension system of the Russian Federation. The research is grounded in a theoretical and methodological framework for applying basic income instruments, necessitated by the system's loss of financial equilibrium. This imbalance stems from demographic challenges, shifts in employment patterns, and the proliferation of benefits not underpinned by insurance-based entitlements, which collectively underpin the relevance of this inquiry. The study identifies and analyses regular and other allowances within the current pension system that exhibit characteristics of basic income. It advances a rationale for segmenting the domestic pension system into three distinct tiers: a solidarity-based (distributive) tier (basic pension income), an occupational insurance tier (insurance pension), and a supplementary tier (allowances for specific categories of beneficiaries). A key proposal is the separate administration of the basic pension income within the pension system. This consolidated component would encompass: within compulsory pension insurance – the fixed payment to the insurance pension; and within state pension provision – the social pension for disabled citizens alongside a range of social allowances. Furthermore, it is proposed to integrate into this basic pension income the social supplement that raises a pensioner's total material security to the level of the pensioner's subsistence minimum established for the Russian Federation as a whole. The universal nature of the basic pension income would ensure its provision to all pensioners, including those previously engaged in precarious forms of employment who have not fulfilled the minimum criteria for qualifying for an insurance pension. The study also puts forward potential funding sources for the basic pension income and explores the feasibility of reallocating the freed-up portion of the insurance tariff within the occupational insurance tier of the pension system. Cumulatively, the payment of the basic pension income, alongside these structural changes, would enhance the purchasing power of recipients of an average insurance pension. This would bring it into alignment with both the national strategic objectives of the Russian Federation in pension provision and internationally recognized social security standards.

Compulsory pension insurance, state pension provision, insurance pension, insured persons, pension system, basic income, basic retirement income

Short address: https://sciup.org/147253450

IDR: 147253450 | UDC: 369 | DOI: 10.15838/esc.2026.1.103.12

Text of the scientific article Issues of introducing a basic income into the Russian national pension system

The research was supported by Russian Science Foundation grant 25-18-00228 “Basic pension income: Risks and opportunities of introduction in the Russian Federation”,

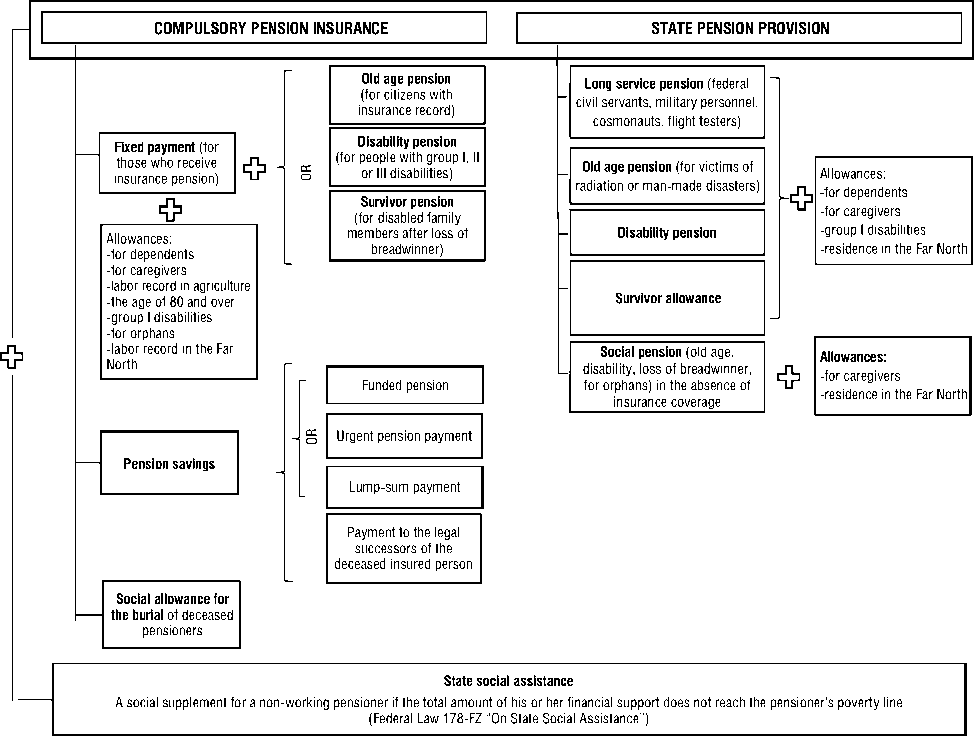

Russia’s modern model of the national pension system (hereinafter referred to as the PS)1 is a multitier provision of citizens with social guarantees in certain life circumstances (old age, disability, loss of breadwinner, long service, etc.) with multiple forms of implementation of government obligations, protection from absolute monetary poverty in accordance with international standards (Fig. 1).

This model is based on a solidary distribution of financing state pension obligations among the economically active and able-bodied population of Russia2. The PS is focused on fulfilling the

Figure 1. Multitier model of the Russian national pension system

Compiled based on: On insurance pensions: Federal Law 400-FZ, dated December 28, 2013. Available at: http://www. (accessed: May 26, 2025); On state social assistance: Federal Law 178-FZ, dated July 17, 1999. Available at: (accessed: May 26, 2025); On state pension provision in the Russian Federation: Federal Law 166-FZ, dated December 15, 2001. Available at: (accessed: May 26, 2025); (Zakharov, 2024).

constitutional guarantees of the welfare state (social justice, financial security of the population, protection from absolute monetary poverty), ensuring the standard of living of citizens in accordance with international standards3. It is a macroeconomic model of budgetary and financial redistribution of monetary resources between generations (Solovyev, 2023).

The sources of financing in the current PS model are differentiated into insurance premiums, federal budget funds, voluntary contributions from individuals and organizations, income from investing citizens’ pension savings, and other sources not prohibited by the legislation of the Russian Federation4.

Pension reforms of recent decades5 aimed at transforming the institutional parameters of the Russian pension system6 were intended to strengthen its financial balance7 (Sedova, 2018) and improve the standard of living of all categories of the disabled population8 (Solovyev, 2014). The ratification of the ILO Social Security (Minimum Standards) Convention No 1029 by the Russian Federation has consolidated the increasing social orientation in the field of compulsory pension insurance and state pension provision of Russia.

In the current pension system of Russia, state social assistance in the form of a social supplement to a pension (SS) is important, as it guarantees protection from absolute monetary poverty to pensioners who do not have a paid job10. It is provided as part of both compulsory pension insurance and state pension provision. The total amount of the pension recipient’s financial support cannot be less than the pensioner’s poverty line (PPL). The amount of the social supplement to the pension is determined so that the total amount of pensioner’s financial provision, including this supplement, reaches the value of the regional PPL. The federal social supplement (FSS) is paid if the total amount of a non-working pensioner’s financial provision does not reach the value of the PPL, in case it is lower than the general value of the PPL in the Russian Federation. The regional social supplement (RSS) is paid if the pension in a constituent entity of the Russian Federation is higher than the same indicator in the Russian Federation (in 2025, 15250 rubles)11. From January 1, 2026, the authority to administer the RSS was transferred to the Social Fund of Russia (SFR)12. In 2025, FSS was implemented in 59 regions of the Russian Federation and the city of Baikonur, and RSS was implemented in 30 regions. The annual number of recipients of the social supplement has shown unstable trend and ranged from 5.2 to 6.2 million people13. In general, from 2015 to 2024, the number of recipients of FSS increased to 2.9 million people14, the number of RSS recipients increased to 3.2 million people15. The share of citizens with incomes below the absolute monetary poverty line among non-working pensioners increased to 14.9% in 2024, which is 2.4 percentage points higher than in 2015. The average size of the regional social supplement was 5180.0 rubles16, the FSS was 3050.0 rubles17. It is worth noting that over the past 10 years, the average size of the SS has increased by 40.24%.

With the current structure of pension recipients and insurance premiums payers, characterized by a significant excess in the number of employees over the self-employed and other categories working for themselves, the cost ratio for paying insurance pensions through insurance premiums and interbudget transfers is approximately 80:20 (in %)18. The share of the inter-budget transfer was 19.83% in 2024. Federal budget funds were transferred to the PS for the payment of pensions (including state pension provision), other pension supplements, benefits and compensations financed from the federal budget (36.53%); to compensate for the shortfall in budget revenues to the Social Fund of Russia due to the establishment of reduced insurance premiums for compulsory pension insurance, temporary disability insurance and maternity insurance (27.73%); for valorization (increase) of the estimated pension capital (20.16%); for compulsory pension insurance (13.21%); for reimbursement of expenses for payment of insurance pensions due to the inclusion of non-insurance periods in the insurance record (2.29%); for the advance payment of pensions to citizens recognized as unemployed, and payment of funeral grants (0.08%).

The expansion of various social guarantees provided by the state19, aimed at improving the standard of living of certain categories of pensioners, increases the imbalance of compulsory pension insurance. A supplement to the fixed payment (FP) being 100% of the FP20 was paid in 2024 to 4.5 million pensioners aged 80 and over (20.0% of the total number of pensioners): 946.1 thousand men and 3.59 million women21. A similar supplement is paid to recipients of insurance pensions with group I disabilities. In 2024, there were 1236.2 thousand people with a group I disability registered in the SFR22. Since 2025, a compensation payment to unemployed able-bodied persons caring for disabled citizens23 has also been introduced into the pension in the form of an additional increase in the fixed payment to the insurance pension and the retirement allowance under the state pension provision24. In 2024, care was provided for 2.6 million people25 and compensation was 1200 rubles. Since 2025, the allowance for caregivers has been indexed along with the pension. The share of its recipients in the total number of all pensioners is 6.3%.

For persons who have worked in agriculture for at least 30 calendar years, a 25% increased fixed payment to the old age insurance pension and disability insurance pension has been established. In 2024 there were 732.5 thousand such people26.

The 50 and 30% increased fixed payment, respectively, is appointed after reaching the insurance record in the Far North and equivalent areas. For residents living in areas with severe climatic conditions that require additional financial and physiological costs, the pension (fixed payment) is increased by the appropriate regional premium rate, depending on the area of residence. In 2024, there were 3.03 million people pensioners living in the Far North and equivalent areas, of which 2.78 million27 are recipients of insurance pensions.

Demographic problems and changes in the nature and structure of employment in Russia pose significant threats to PS, leading to an increase in its imbalance. They are also prerequisites for its transformation and will be described below.

The research issue is to find a way to resolve the contradiction between demographic and structural threats to the pension system and the standard of living of pensioners, due to its increasing imbalance, and the possibilities of overcoming them by separating the tools for developing and managing the non-insurance and insurance parts of the pension system.

The object of the study is the pension system, which includes compulsory pension insurance and state pension provision in the Russian Federation. The subject of the study is a set of economic relations that will develop in the process of introducing the basic income (BI) tools into the PS.

The aim of the work was to develop the provisions of the BI concept in relation to the development of the theoretical and methodological foundations of its introduction into the Tax Code of the Russian Federation.

The following tasks were solved in the course of the study: 1) description of the results of scientific discussions and experience of using the BI in social systems; 2) assessment of the risks of developing the PS in the medium and long term without making changes to it; 3) identification of regular payments in the current PS that correspond to the concept of the BI, and justification for dividing the PS into three tiers: solidarity-based (distributive) tier (basic pension income), occupational insurance tier (insurance pension), and supplementary tier (for certain categories of beneficiaries); 4) determination of ways to introduce BPI into the PS.

The hypothesis of the study is that the proposed model of introducing the BPI into the PS has real grounds, corresponds to the national goals28 of Russia and international standards in the field of social protection of pension recipients.

The novelty of the research lies in the development of theoretical and methodological foundations and specific practical approaches to the introduction of BPI in the Russian Federation in the medium term, meeting modern threats and opportunities in the field of social policy.

Theoretical and methodological foundations of the research

In the context of increasing challenges for national social institutions29 (Stepanova, 2021; Nemtsova et al., 2025), the issue of their adaptation to rapidly changing socio-economic conditions30 (Gorlin, Lyashok, 2022; Voronin, Stolyarov, 2020) and the search for alternative social security measures for pensioners (Safonov et al., 2023) are of increasing scientific interest.

Researchers are actively raising the issue of the expediency of combining in national pension systems their main theoretical models: the Bismarck insurance model31 and the non-insurance Beveridge model32. Publications note the expediency in modern conditions to use a more efficient basic income system33 in non-insurance pension systems rather than the Beveridge comprehensive social protection model34 (Beck et al., 2024; Furmanska-Maruszak, 2019; Hoynes, Rotshtein, 2019; Reed et al., 2022).

Numerous studies are being conducted in the international scientific community on the possible introduction of the concept of basic income (or its elements) into national social security systems. The basic income is defined as a universal monetary payment (to all citizens – a universal BI), regularly received by an individual without condition (unconditional BI) or in accordance with certain payment conditions (transitional forms of BI). Scientific research concerns the theoretical component of this issue (Bobkov et al., 2024; Gentilini et al., 2020; Ortiz et al., 2018; Van Parijs, 1992), and its applied aspects (Bobkov et al., 2021a; Bobkov, Odintsova, 2022).

Researchers analyze both the positive and problematic effects of implementing the BI concept (Belyaeva, Remarenko, 2020; Kapeliushnikov, 2020; Cowan, 2017; Crisp, De Wispelaere, 2022; De Wispelaere et al., 2025; Widerquist, 2018). Its main achievements are a reduction in the absolute monetary poverty of certain categories of citizens, an increase in the standard of living of recipients and a decrease in inequality between different social and socio-demographic groups, a reduction in the cost of managing pensions, social allowances and other support measures, etc. Challenges include the growth of additional costs for providing payments, an increase in the tax burden on the employed, the manifestation of dependency attitudes among certain categories of the population, etc.

The various approaches proposed by the researchers to the introduction of the BI focus on the effective inclusion of this new institution in the social policy of countries and the achievement of socio-economic indicators that meet international standards with its application (Castro, West, 2022; Lain, 2022). The proposed forms of BI introduction range from radical, replacing existing payment and benefit systems35 (Kolesnik, 2018; Ostapenko, 2016; Groot, 2002), to compromise, complementing and expanding existing social assistance systems36 (Kvashnin, 2019).

Despite the controversy, researchers agree that the implementation of the BI concept is a necessary prospect for the future, and at the current stage it is proposed to integrate its individual elements (transitional forms) into the existing social security system and gradually neutralize the consequences of threats to public social policy (Bobkov et al., 2021a; Zakharov, 2024).

Thus, in the OECD countries, basic pensions have been introduced at the first level of pension systems. In Denmark and the Netherlands, where the cost parameters in pension systems are similar to those in Russia their amounts for residents were 35.9 and 29.1%37 of average gross earnings, respectively. The possibilities of using BI in pension systems, including international experience and Russian research, are discussed in scientific papers (Bobkov et al., 2021a; Smirnova, 2024).

Demographic constraints and structural changes in employment, which serve as prerequisites for the transformation of management tools for the collection and allocation of resources in the

Russian PS and the introduction of the BPI into it, are manifested in the following. Demographic changes in Russia are the most discussed constraints (Frumina, 2023) and risks affecting socio-economic development. They are expressed in depopulation and aging, leading to a decrease in the proportion of the working-age population (Porfiriev et al., 2022). The forecast of the Institute of Economic Forecasting of the Russian Academy of Sciences in the long term indicates an inevitable decline in the population of Russia. Thus, 146.2 million at the beginning of 2024 may decrease to 142 million in 2035 and 136 million in 2050, even with optimistic assumptions regarding the birth rate, death rate and migration growth (Shirov, 2024).

Forecasts of demographic parameters of the pension system also model the depopulation in Russia and a change in population structure by 205038 (Kashepov, 2023). The share of people over 60 will increase from 27.6%39 (2024) to 34% (47.1 million people) by the end of the forecast period, and over 65 – to 25% (34.8 million people) (Shirov, 2024). The demographic forecast of the Federal State Statistics Service in all its variants also shows an increase in the proportion of those over the working age to 27%40 by 2046 and an increase in the dependency ratio (considering only the population over the working age) to 468 per 1000 by 204641.

The second key threat to PS and the stimulating vector of its adaptation to new conditions is a change in the employment structure. If in 2025 the number of self-employed citizens will amount to 13.5 million people42, then by 2050 it may grow to 29 million people. The employment structure is being transformed, the employed may make up 38.8%, and the self–employed – 61.1%43 (Vashalomidze, 2024). An acute problem is that currently only 4.4% of self-employed citizens have entered into voluntary legal relationships for compulsory pension insurance, formed their pension rights and paid insurance premiums, the rest are potential recipients of social pensions paid under the legislation on state pension provision from inter-budget transfers and providing a standard of living significantly below the pensioner’s poverty line.

Taking into account the fact that 95.6% of the self-employed currently remain outside the scope of compulsory pension insurance and can replenish the number of recipients of social pensions when they reach the age of disability, we can expect a significant increase in the number of recipients and, consequently, a rapid increase in the number of pensioners with a low standard of living.

In the future, with continued demographic trends, changes in the employment structure, liberalization of the responsibility of policyholders and employees for the formation of pension rights, as well as an increase in the social orientation of the state, the share of its transfer will certainly grow, strengthening both the non-insurance mechanism for financing, forming, and exercising pension rights (Solovyev, 2025) and the non-insurance nature of the PS itself in general.

This implies the need and possibility of separating the formation and management of non-insurance and insurance payments in the pension system. In the multitier model of the Russian PS, there are regular, inherently noninsurance payments that could become parts of the BPI.

One of them is a fixed payment to the insurance pension (FP), provided by a share of insurance premiums paid by policyholders and the selfemployed. In the previous legislation in 2001– 201444, it was called the basic amount of the insured part of the labor pension (BPIP). The task was to bring it to the pensioner’s poverty line, regardless of the size of the insurance pension. The purchasing power of the pensioner for the basic part of the pension has been constantly increasing. In 2009, it was 62.5% of the PPL45. However, in 2010, the pension legislation was changed, the basic pension was included in the insurance pension and was called a fixed payment to the insurance pension (FP)46, which, in fact, represented the abolition of the basic pension and the task of bringing it to the PPL. A fixed payment is established for citizens simultaneously with the appointment of an insurance pension, with the exception of certain categories of recipients47 who have exercised the right to choose a pension48. In 2025, the base amount of the FP is 8,907.70 rubles49 (58.4% of the RF PPL). For the people with group III disabilities and those who have lost a breadwinner, the size of the FP is 50% of its base size. We believe that, considering the above demographic trends and changes in the employment structure, it would be necessary to return to the isolation of fixed payments in the insurance part of the PS in the form of a BPI funded from sources other than insurance premiums (Nekrasov, 2020).

Another element of the regular payment, which could become a part of the BPI, is state social assistance in the form of a social supplement to the pension (SS).

In the state pension provision, the prototype of the BPI should be considered a social pension for disabled citizens who could not form the necessary amount of pension rights to enter the pension insurance system or did not have such an opportunity (for example, lifelong disabled people, children with disabilities).

In the case of the formation of a BPI from the above-mentioned regular payments, the FP (its basic amount and the established allowances for certain categories of recipients) will be withdrawn from the insurance pension. This means that it will be necessary to identify a single source of financing for this payment, which differs from the existing ones, which currently also include additional insurance and non-insurance sources that do not worsen the total amount of insurance pension already paid under compulsory pension insurance. In 2023, 1,452.4 billion rubles were allocated from the federal budget for the payment of insurance pensions50 (including 317.9 billion rubles for compulsory pension insurance), and 980.7 billion rubles were provided in 202251.

In the long-term PS, the benefits provided for the payment of insurance premiums52, early and preferential pension models for professions and positions in certain sectors of the economy that are not fully provided with insurance (corporate) financing53, and the obligations assumed by the state to increase the financial security of pensioners54 need to be reviewed. It is advisable to maintain insurance premium rates for certain types of activities (for example, those with harmful and difficult working conditions), and gradually reduce benefits for a number of others.

In our opinion, there are significant reserves to ensure the equivalence of pension obligations assumed by the state to citizens and the pension rights of insured persons, and to improve the standard of living of pensioners, both in the possible increase in insurance premium rates in certain types of work, and in more consistent compliance with insurance principles in the compulsory pension insurance system. Currently, it has established numerous preferential pension models for a number of categories of recipients of pension insurance payments. All this will allow balancing compulsory pension insurance in the long-term Russian PS.

Thus, as a result of increased pressure from external factors in relation to the pension system, affecting the retirement of citizens and increasing state responsibility for their financial well-being, as well as due to problems in the distribution of funds accumulated within the pension system, prerequisites have emerged for the transformation of the current solidarity insurance model of pension insurance and state pension provision. It is advisable to divide the PS into three tiers: a solidarity-based (distributive) tier, which is protective in nature and is ensured by the introduction of a BPI, an occupational insurance tier based on the payment of an insurance pension, and a supplementary tier, which includes allowances for certain categories of pensioners 55.

All three tiers of the prospective model of the Russian pension system will have a separate management with interrelated conditions for the establishment and payment of various parts.

A comparison of the current and prospective PS models is presented in Table .

As a result, the proposed basic part of the prospective pension system of the Russian Federation is transformed from a solidaritybased insurance model into a solidaritybased distributive model founded on the principle of social solidarity of generations of

Comparison of the current and prospective PS models in Russia

Model Composition Source of financing Terms of appointment Goal CD E о Solidarity-based insurance (for insured persons) FP1) IP2) Insurance premiums, Transfers Mandatory age Insurance record Pension rights (IPP3)) Replacement of lost earnings and protection Social security (for insured persons who have not developed their labor and insurance records) Social pension Inter-budget transfers Mandatory age Lack of insurance pension rights Permanent residence in Russia Lack of paid employment4) Protection from absolute monetary poverty Social protection SS5) Allowances Inter-budget transfers Insurance premiums for individual allowances Need Mandatory age Presence of dependents Insurance record Protection from absolute monetary poverty ф E CD CD О Solidarity-based distributive (public) BPI6) Taxes (including rental payments to budgets of different levels) Payment for all citizens who have reached the mandatory retirement age, or who belong to professional or social categories who are eligible for a pension in advance Protection from absolute monetary poverty Occupational insurance payment based on compulsory pension insurance IP FP7) Insurance premiums Mandatory age Insurance record Pension rights (IPP) Increased financial security depending on labor and insurance records Supplementary payments SP Inter-budget transfers Allowances for certain categories of pensioners; Long-term savings8) Increased financial security depending on special circumstances and long-term savings 1) Fixed payment. 2) Insurance pension. 3) Individual pension points. 4) For citizens from among the small-numbered peoples of the North who have reached age 55 and 50 (men and women, respectively) who permanently reside in areas inhabited by small-numbered peoples of the North, and citizens who have reached age 70 and 65 (men and women, respectively), foreign citizens and stateless persons who have permanently resided in the territory of the Russian Federation for at least 15 years and have reached the specified age. 5) Social supplement to the pension. 6) Basic pension income. 7) Funded pension. 8) Long-term savings program. Ministry of Finance of Russia. Available at: (accessed: June 14, 2025). Source: own compilation.

economically active population, where regular state-guaranteed pension payments are provided by general taxes or other sources and distributed among recipients in accordance with approved rules in a fixed amount.

The solidarity-based distributive model founded on the introduction of the BPI is aimed at providing constitutional guarantees for citizens, preventing absolute monetary poverty of pension recipients, which is ensured by the universality of this model, i.e. coverage of all recipients of insurance and social pensions. It is proposed to withdraw the public part of the Russian pension system from the system of compulsory pension insurance and state pension provision into a separate system of basic pension income, replacing a fixed payment, social pension and social supplement to pension. According to the authors, the management of the basic pension income system should be carried out by the Pension and Social Insurance Fund of the Russian Federation.

Data and methods of their use

The data used were departmental statistics and analytical data from the Pension and Social Insurance Fund of the Russian Federation, the Pension Fund of Russia, the Social Insurance Fund of Russia, statistical data from Rosstat, legislative and regulatory acts in the field of compulsory pension insurance, state pension provision, and social assistance.

The following methods were used in the study: analysis and comparison of indicators of the Russian state pension system, including its development strategy56; synthesis of the findings and data from other studies on the problem under study; theoretical and methodological modeling of the BI introduction in the PS.

Results and their discussion

The prospective public part of the PS with the use of the BPI allows protection from poverty for an increasing part of the employed who do not ensure their pension rights and recipients of pensions less than the pensioner’s poverty line.

The introduction of the BPI assumes a monthly monetary payment to citizens who have reached the mandatory retirement age57 or are classified into professional58 or social categories59 of citizens who are eligible for a pension in advance60.

Its size, based on its purposes, is set at least equal to the general pensioner’s poverty line of the Russian Federation (RF PPL). Linking the BPI to the value of the RF PPL establishes its size significantly higher than the fixed payment and social supplement to the pension, as well as the size of the social pension. This will allow excluding the FSS and other allowances for fixed payments adopted to increase the financial security of certain categories of pensioners (allowance for labor record in agriculture, allowance for caregivers, etc.) with new pension appointments.

Setting the BPI minimum as RF PPL will ensure constant pensioners’ payments and uniform legislation when changing their place of residence. The adopted decision will allow eliminating unnecessary administrative procedures and complicated budget planning related to the establishment of a social supplement for low-income categories of pensioners, and providing greater opportunities for pension system digitalization. In the constituent entities of the Russian Federation, where the size of the regional PPL is higher than the RF PPL, it is proposed to retain the constituent entities’ powers to compensate for the PPL excessing the BPI.

The introduced BPI will be appointed regardless of the fact of paid employment for citizens who acquire the right to an insurance pension and reside in the territory of the Russian Federation:

– old age on a general basis61 – men aged 65 and women aged 60,

– disability – from the date of establishment of a persistent health disorder by the medical and social expertise bodies,

– loss of breadwinner – from the date of death of the breadwinner,

– in advance (professional and social categories of citizens) – when special insurance record62 and (or) age reached63,

– in advance due to a great insurance record – from the date when the length of insurance record is 42 years for men, 37 years for women.

In case the requirements for the appointment of an old age insurance pension are not met when men reach 65 and women reach 60, we consider it advisable to establish a BPI for citizens who have been living in Russia for at least 15 years. If a citizen leaves Russia for permanent residence, it is advisable to terminate the payment of the BPI.

The issue of establishing a BPI for immigrants (Chernykh, 2020) and persons with acquired citizenship remains debatable. As an additional requirement for the latter, it is proposed to introduce the condition of living in Russia for a fixed number of years continuously.

The introduction of the BPI into the pension system, of course, raises a rather acute issue of increasing the cost of ensuring public obligations by the state64 (Bobkov, 2021b; Gontmakher, 2019). In this regard, attention should be paid to the fact that the share of pension expenditures in Russia’s GDP is lower than in a number of countries with similar-sized economies and similar pension systems. In 2023, the budget of the Social Fund of Russia for expenditures on pensions and other benefits amounted to 8.1% of GDP, including the share of pension payments of 5.9% of GDP. OECD countries with similar insurance contribution rates have pension costs that exceed the Russian level (Solovyev, 2025). The largest share of GDP spent on state pensions is in Greece and Italy (about 16%), then there are Austria and France – 13–13.5%, Germany, Denmark, Japan, Spain – 9.6–10.4%, the Netherlands – 5%65.

Overall, the cost of state pensions is estimated to be between one quarter and one third of total government spending in OECD countries. The comparison confirms that an increase in the share of pension expenses in Russia will not be exclusive.

The occupational insurance pension will be aimed at improving the financial well-being of pensioners to the level of international standards66 and approved regulatory indicators67 in the Russian Federation. Due to the withdrawal of a fixed payment from pension insurance to the basic income system, the released share of the insurance tariff68, previously allocated to finance a fixed payment to an insurance pension, can be recorded in an individual personal account, and the collected insurance premiums redistributed to additional indexation of insurance pensions. As a result, the pension rights of insured persons will be fully accounted for, which will increase pensions in the future. The occupational insurance pension is a further development of the current compulsory pension insurance, where personalized accounting of the pension rights of insured persons is provided by compulsory insurance contributions from policyholders and voluntary co-financing of the insurance tariff by the employee.

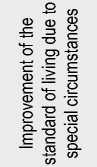

The structure of payments to pensioners after the implementation of the basic income tools in the pension system of the Russian Federation will be as follows ( Fig. 2 ).

Thus, both horizontal and vertical coverage of all socio-demographic groups by state social guarantees will be ensured. The minimum protection from absolute monetary poverty will be provided by the BPI, which will avoid possible penalties in accordance with the law “On Enforcement Proceedings”69 and will preserve minimal property70. The establishment of the insurance pension as the second tier of social protection will allow citizens to increase income close to the level of international standards71 and targets of the Strategy for the Long-term Development of the Pension System of the Russian Federation. A higher standard of living for pensioners will be facilitated by the establishment of non-BPI allowances related to compensation for living in the Far North, areas equated to them, and supplementary social security for professional categories of workers72.

Figure 2. Proposed multitier model of the Russian PS with the BPI institute

/\

Long-term savings

Supplementary payments (allowances for certain categories of pensioners)

Funded pension, urgent pension payment

Insurance pension

Basic pension income

---------------------------------------------------------к

Citizens

The insured

Participants in pension savings programs

Professional categories

-------------------------------------к

Citizens The insured

Citizens

Horizontal coverage by social groups

Source: own compilation.

Conclusion

Summing up the results of the study, we conclude that the hypothesis put forward is confirmed: the proposed model for introducing the BPI into the PS has real grounds, meets the targets of Russia and international standards in the field of social security of pension recipients. The scientific discussion concerning the prospects for the development of the pension system, as well as the identified trends in the demographic and employment areas in Russia, emphasize the importance and relevance of examining the issues under study now and for the future. The research clarifies the requirements for the mechanism of introducing the BPI not less than the general PPL in the Russian Federation.

The proposed structure of the Russian PS model is three-tiered, consisting of a solidaritybased distributive (basic pension income), occupational insurance (insurance pension) and supplementary parts. As a result, pension benefits will be ranged in terms of categories of recipients and the level of social security from basic protection from absolute monetary poverty to the improvement of the standard of living of pensioners considering the special circumstances of previous employment, health status, household composition, etc.

In our opinion, the results of the conducted research, if applied in practice, allow us to get closer to achieving the key national development goals of the Russian Federation in the long term:

– ensuring the replacement rate73 of old age insurance pension of up to 40% of lost earnings with a standard length of insurance record and average wages;

– ensuring an average old age labor pension at least 2.5–3 times more than the pensioner’s poverty line, and in a longer term, achieving a socially acceptable level (in 2024, it is approximately 3.7 times more than the PPL)74;

– maintaining an acceptable level of insurance burden for economic entities with a unified insurance premium rate for all categories of employers;

– ensuring the balance of pension rights generated with the sources of their financial support.

In the future, it is necessary to model the resources and pension payments required in the prospective pension system of the Russian Federation and their distribution between the noninsurance and insurance parts of the pension system and among the recipients.