Payment digitalization in response to the challenges of a cashless society

Author: Boris Siljković, Sanel Mehmedi, Dženis Bajramović

Journal: Ekonomski signali @esignali

Article in issue: 2 vol.20, 2025.

Free access

Payment digitalization, as reflected in the topic of this paper, represents one of the key transformations with significant implications for improving the financial system and fostering economic growth, while responding to contemporary trends. The paper focuses on the process of payment digitalization through three sections, which directly affect complementarity and practical developments in the economies of Serbia and the Western Balkans. The findings indicate that Serbia and the Western Balkans lag behind developed European economies, and that cash still dominates as a method of payment in our region. This is corroborated by our field surveys conducted in Serbia and Montenegro (Kraljevo, Plav and Rožaje). These results are further complemented by a comparison with the prevalence of digital payments globally and within the EU. The study suggests that, without coordinated actions at all levels - from financial institutions to citizen education - the transition toward a cashless society will remain constrained, despite its potential to deliver innovations in security, privacy and inclusiveness.

Payment digitalization, contemporary trends, EU, Serbia, security, inclusiveness

Short address: https://sciup.org/170211627

IDR: 170211627 | UDC: 336.794(4-6EU:497.11); 004.738.5:336.7 | DOI: 10.5937/ekonsig2502153S

Digitalizacija plaćanja u susret izazovima društva bezgotovine

Digitalizacija plaćanja kroz održaj na naslov teme predstavlja jed-nu od ključnih transformacija koja proizvodi značajne implikacije na pobolj-šanju finansijskog sistema, rasta ekonomije i ide u susret savremenih tren-dova. Ovaj rad je koncentrisan na proces digitalizacije plaćanja kroz tri dela što ima direktan uticaj na komplementarnost, praktične trendove ekono-mija Srbije i Zapadnog Balkana. Istraživanje je pokazalo da Srbija i Zapadni Balkan zaostaju za razvijenim evropskim ekonomijama, sa konstatacijom da u našem regionu gotovina i dalje dominira kao metoda plaćanja. Ovo su pokazala i naša lična istraživanja u gradovima u Srbiji i Crnoj Gori, Kra-ljevu, Plavu i Rožaju. Sve ovo upotpunili smo i uporedili sa prisustvom digi-talnih plaćanja u svetu i EU. Rad kroz istraživanje je imao za cilj da bez akcija koje bi se sprovele na svim nivoima na relaciji od finansijskih institu-cija do edukacije građana bezgotovinskog društvo koje bi za rezultat imalo inovacije, kao što su bezbednost, privatnost i inkluzivnost sve u susret iza-zovima društva bezgotovine.

Text of the scientific article Payment digitalization in response to the challenges of a cashless society

Cashless services point toward a future in which contactless payments will become the dominant form of monetary transactions. Our research focuses on the extent to which banks and card-based payments are becoming predominant. It is increasingly likely that cash will soon become a relic of the past, fundamentally changing the way people use money in everyday life. During 2025, based on available research, more than two thirds of Serbia’s population used some form of digital payment. This provides a clear starting point for our analysis: such developments generate benefits not only for consumers - primarily through faster transactions and time savings - but also for businesses and the state, which have direct incentives to support them. In particular, the use of digital payments can reduce tax evasion (avoidance) and directly stimulate economic growth.

The next stage of our research examines the scope and frequency of using banking applications on mobile phones and smartwatches. This technological infrastructure forms the basis for implementing modern payment solutions, including Click to Pay, Google Pay and other online payment systems integrated within digital wallets.

Instant payments are increasingly used in online transactions and represent an additional payment channel that is expected to grow further in Serbia. This is a concrete contribution of the present paper. One key advantage is the use of Google Pay and Apple Pay, which facilitates simple and convenient payments and supports payment digitalization without the need to use a physical payment card. Traditional purchasing models are inevitably being disrupted by new technologies - an evolution we support with our own surveybased research conducted in Kra-ljevo, Zubin Potok and Leposavić. The results indicate that payment digitalization is creating a new reality in which speed, convenience and interactivity play a central role, particularly through contactless payments that are still in an early stage of adoption in these locations. We recommend that app-based payments should become a dominant category, with the primary benefits being time savings and increased efficiency for firms through faster revenue generation. In our view, this also contributes to higher tax revenues through improved transaction recording, which represents a direct contribution of this research.

Payment Digitalization and Practical Trends in the Economies of the Region and Serbia

The introductory segment of this section addresses the growing shift away from cash and the development of various models of digital payments. The role of the internet in the development of electronic business is dominant, as e-commerce entails conducting business transactions online. Electronic payment systems facilitate the completion of purchases once consumers decide to buy a product or service, enabling payments between buyers and sellers in the most efficient, fastest and safest way (Savić et al., 2024). The evolution of money management - from mobile banking to new online platforms - means that contemporary payment trends shape daily life for both businesses and citizens, thereby fostering more efficient operations. QR codes, mobile applications and ewallets are becoming ubiquitous in everyday transactions between individuals and companies. The overall result is lower costs, reduced risk of errors and a tangible contribution to curbing the shadow economy, which in turn supports economic growth and the advancement of the green economy. In this way, payment digitalization opens access to new regi- onal markets, allowing Serbian firms to place products and services more easily, while offering consumers a wider choice and simpler shopping across the Western Balkans.

As a concrete contribution, we present evidence that clearly demonstrates the rapid expansion of mobile banking and the number of registered users of digital services in Serbia, based on the latest data from the National Bank of Serbia.

Table 1. Number of mobile and electronic banking users and volume of payment transactions in Serbia (2023 and 2024).

|

Number of mobile banking users |

2023 |

2024 |

|

4 million |

4.6 million |

|

|

Number of registered users of electronic banking |

2023 |

2024 |

|

4.1 million |

4.4 million |

|

|

Volume of payment transactions |

2023. Year |

2024. Year |

|

109.3 million |

251.9 million |

Source: “Mobile and electronic banking usage in Serbia continues to grow, reaching record numbers in 2024”, Serbia Business, 07.03.2025. Accessed 06.12.2025. https://serbia-business. eu/mobile-and-electronic-banking-usage-in-serbia-continues-to-grow-reaching-record-numbers-in-2024/.

If we compare trends in the region more directly, recent analyses by the World Bank/International Bank for Reconstruction and Development show that the region is experiencing expansive infrastructure development, which contributes to faster and cheaper transactions. Looking back, in the period from 2017 to 2021, account ownership increased from 7.6 million adults to 9.3 million. Cashless transactions per capita in the participating program economies also experienced a sharp rise, with growth rates between 80% and 150%.

To further substantiate the topic, we conducted a dedicated survey in Montenegro (the municipality of Plav). Using a questionnaire on a sample of 25 respondents, we aimed to gain insight into citizens’ habits in adopting contemporary digital financial tools. Respondents answe-red a set of questions covering the use of cash, payment cards, mobile payments, and the banks they use, with the goal of understanding the use of different payment methods (Kosta-dinović, 2024; Trklјa, et al.2024).

Table 2. Results of the survey on the use of cashless payments in Plav.

|

Question |

Answer |

Number of respondents |

Percentage (%) |

|

Payment method |

Cash |

25 |

100% |

|

Payment card |

21 |

84% |

|

|

Mobile payment |

14 |

56% |

|

|

Types of payment cards |

Debit |

12 |

48% |

|

Credit |

9 |

36% |

|

|

Prepaid |

4 |

16% |

|

|

Frequency of card use |

Often |

14 |

56% |

|

Occasionally |

7 |

28% |

|

|

Rarely |

2 |

8% |

|

|

Does not use |

2 |

8% |

|

|

Places where payments are made |

Shops |

25 |

100% |

|

Restaurants |

12 |

48% |

|

|

Gas stations |

1 |

4% |

|

|

Shops |

0 |

100% |

|

|

Banks respondents use for ATMs |

CKB |

12 |

48% |

|

Hipotekarna banka |

7 |

28% |

|

|

NLB |

6 |

24% |

|

|

Use of contactless payments |

Yes |

21 |

84% |

|

No |

4 |

16% |

|

|

Do respondents use cryptocurrency or cheques? |

Cryptocurrency account |

0 |

0% |

|

Cheques |

0 |

0% |

Source: Authors’ survey, 2025.

The results show that all respondents continue to use cash when making purchases, indicating the persistence of traditional payment practices in smaller communities. However, a majority of respondents (21 out of 25) also use payment cards, with debit cards predominating (12 respondents), followed by credit cards (9) and prepaid cards (4). Mobile payments are used by 14 respondents, demonstrating a gradual acceptance of digital methods in everyday life. Most respondents have used contactless payments at least once, which indicates contemporary tendencies in citizens’ financial behavior. Respondents use payment cards for different purposes - most commonly in shops, for paying bills, in restaurants, and at gas stations. The banks whose ATMs respondents most often use to withdraw cash are Crnogorska komercijalna banka (CKB), Hipotekarna banka and NLB, reflecting the infrastructure and availability of financial services in Plav.

To strengthen the originality of our research contribution, we also conducted a survey in the municipality of Rožaje. The findings indicate that cards are most frequently used in restaurants and at fuel stations. By contrast, women most often use cards at kiosks, pharmacies and cosmetics stores. The most commonly used cards are issued by Lovćen Banka. Trends observed in this municipality suggest that people aged 35–54 often have cards because of loans and installment-based payments (e.g., furniture purchases) due to scheduled electronic deductions. To better understand the local context, we noted that larger retail chains such as Voli, Elkos Group (ETC) and Idea have card terminals, while many local shops do not. It is also noticeable that some cafés in the city center do not accept card payments; butcher shops and open markets generally do not either, which is also the case in some other towns in Montenegro. Our fieldwork further shows that furniture salons in Rožaje often do not offer card payments, whereas fuel sellers do have terminals (Eko pumpa and M-Petrol). Overall, the survey results suggest that the traditional cash-based payment method remains dominant, alongside a strong expansion of card-based digital payments, while payments via mobile applications still lag and cheque payments are disappearing as an instrument of cashless payments. To further support our research objective, we compared these findings with survey-based analysis from Kra-ljevo. In that municipality, bank cards are mostly used at gas stations and cafés, while cash is still most commonly used in shops and restaurants. The use of cheques as a means of payment is very limited. Overall, a pronounced tendency can be observed toward a shift from cash to contemporary digital payment methods, alongside the general observation that cash remains in active use.

Table 3. Results of the survey on the use of contactless payments.

|

Respondents’ age groups (n=10) |

|

|

Age group |

Number of users |

|

Under 18 |

0 |

|

18–40 |

4 |

|

40–50 |

3 |

|

50+ |

3 |

|

Type of cards used |

|

|

Card type |

Number of users |

|

Visa |

5 |

|

MasterCard |

4 |

|

Dina |

1 |

|

American Express |

0 |

|

Payment method in shops |

|

|

Method |

Number of users |

|

Card |

4 |

|

Cash |

6 |

|

Cheque |

0 |

|

Payments in restaurants |

|

|

Method |

Number of users |

|

Payment cards |

5 |

|

Cash |

5 |

|

Cheque |

0 |

|

Payments at gas stations |

|

|

Method |

Number of users |

|

Cash |

3 |

|

Payment card |

7 |

|

Cheque |

0 |

|

Mobile m-banking application |

|

|

Answer |

Number |

|

Da |

3 |

|

Ne |

7 |

|

Use of cheques |

|

|

Answer |

Number |

|

Da |

1 |

|

Ne |

9 |

Source: Authors’ compilation, 2025.

When viewed numerically, cash remains the dominant category among 56% of respondents. Cash payments dominate in shops (60%) and restaurants (50%), and are least used at gas stations. Across these analyzed categories, the average frequency of cash usage amounts to 56%.

As a final reflection on our field research, we draw on the analytical segment of another study and reiterate the view that, given that card, phone, and even smartwatch payments have been available domestically for some time, it is timely to recognize that Serbia is likely to become part of a modern global society in which cashless payments are predominant (Siljković et al., 2025).

Overview of Cashless Payments Worldwide

The main trends in payment digitalization in 2025 include real-time payments and the widespread use of mobile wallets, where security - and the capability to implement it effectively -plays an important role in supporting global economic growth. Another development is the gradual penetration of crypto-assets into cashless payment models; based on our practical experience, we recommend continued caution, as this trend depends to a large extent on the political and economic momentum of the world’s largest economy, the United States. A 2025 report on e-commerce trends indicates persistent digitalization and a consumer society accompanied by impressive technological progress. The report we consulted focuses on the complexity and opportunities defining global e-commerce in 2025. The global market trajectory is clear and rapid: economic growth is accompanied by an increasing number of internet users, expected to reach 3.6 billion by 2029, according to Statista.

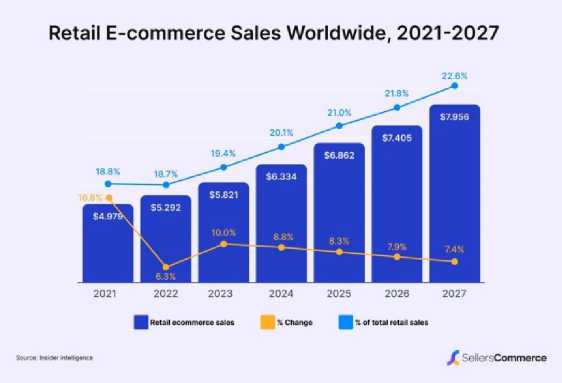

The strength of the global economy is also reflected in the fact that worldwide e-commerce exceeds USD 6.86 trillion in 2025. A stable upward trend is expected to push the market to almost USD 8 trillion by 2027. Inflation in 2022 and 2023 eroded a large share of real gains in the market. In 2025, 21% of all retail purchases globally are made online; by 2027 this share is expected to reach 22.6%. This change is not only about total consumption, but also about frequency, access, and the normalization of digital behavior. An indicator of this shift is the 2.77 billion online buyers worldwide - about 33% of the global population - and forecasts suggest that this number will continue to grow. Among the leading economies, China ranks first with 904.6 million buyers, followed by the United States with 288 million (Edwards, 2025). In our view, new markets and emerging economies will increasingly find their place and share, driven by mobile access, social commerce and fast international delivery. From this perspective, a natural direction for future research would be to examine what these developments mean for businesses in Serbia.

Research on global payment trends -particularly those of the European Union, which is geographically closest to us - shows that the share of cash has declined significantly from 68% in 2019 to only 40% in 2024. This indicates a dramatic shift in consumer payment behavior. In value terms, cash accounts for only 24%, suggesting that electronic payments are increasingly used for higher-value transactions (web source).

Figure 1: Retail e-commerce sales worldwide, 2021–2027

Source: Edwards, K. (2025). Global e-co-mmerce overview: 2025 Insights, 16.07.2025, E-commerce Germany News, Available 07.12.2025,

Cashless Payments in Serbia and the Western Balkans

Across all forms of cashless payments, Serbia holds a leading position in the Balkans. According to a 2024 analysis, the region’s e-market (e-co-mmerce) is expected to reach EUR 2.6 billion, with projections to grow to EUR 3.98 billion by 2029. The region faces specific challenges that constrain faster development of cashless payments - such as cash on delivery -which is also confirmed by our personal experience: during grocery delivery in the Voždovac municipality of Belgrade, the Glovo courier did not have a POS terminal and requested cash payment. This experience is directly at odds with developed European markets, where digital payments are the behavioral norm for customers (Angelovska Stankov, 2024). A noticeable trend in our research is that users adopt mobile payment systems faster than computerbased electronic payment systems. ICT literacy among younger populations - and older populations who are learning and following contemporary digital trends - contributes to the growing number of users of mobile payment systems.

The future of payments also includes the emergence of the so-called digital euro, a digital form of the European currency. Currently, at the end of 2025, the digital euro is still in the development phase. In the near term, banks are expected to offer the digital euro through digital wallets, while public institutions will enable payments that are free of charge and available both online and offline (Elliott et al., 2025).

One increasingly common solution at all levels is the application of sophisticated software solutions aimed at improving business operations, particularly decision-making processes (Mehmedi et al., 2022). In this direction, our further research would support the view that implementing new software solutions is among the key factors for increasing profitability, competitiveness and long-term economic growth of companies in Serbia and the Western Balkan countries. Information technologies and the globalization of markets - phenomena we witness today - change consumer behavior and, in turn, push companies to create new value and improve their performance in reaching potential customers (Bakator et al., 2024).

Table 4. Business digitalization (software solutions) in Bosnia and

Herzegovina.

|

Reduction in operating costs |

Effect on employment (increase) |

Increase in turnover after implementing digital technologies |

|

19.4% of companies |

89.1% of companies |

46.5% of companies |

Source: (Turulja et al., 2021.)

Conclusion

The general conclusion from the preceding analysis is that the Western Balkans and Serbia lag behind developed markets; nevertheless, the potential for growth is substantial. The key to success lies in achieving the standards of digital-wallet models applied in advanced economies – models that can be followed or, where appropriate, adopted from best practice. Our position is that investment in digitalization is warranted despite the costs, because it increases profitability and revenues both at the individual and company levels. A deeper interpretation shows that the Western Balkans’ lag in payment digitalization is evident, with cash still dominant. Mobile wallets, cash-less payments and instant systems are increasingly a behavioral standard that produces positive economic effects, improves tax collection and contributes to suppressing the shadow economy. Ultimately, payment digitalization can deliver innovations in digital techniques, security, privacy and financial inclusion, ensuring that all segments of society can participate equally in the benefits of digitalization. The presented results therefore also leave room for further research.