Progressive taxation of dividends: The dynamics of fiscal effects and risks in 2022–2028

Author: Borisov O.I.

Journal: Economic and Social Changes: Facts, Trends, Forecast @volnc-esc-en

Section: Public finance

Article in issue: 1 т.19, 2026.

Free access

The transition to a progressive scale of personal income taxation in Russia has affected not only labor but also investment income. The newly created preferential tax regime for dividends has sparked considerable debate and divergent views on achieving a balance between tax equity for ultra-high incomes and maintaining an attractive investment climate. The aim of our study is to assess the fiscal effects of the recent dividend tax reform and to identify the long-term effects and risks associated with various scenarios for its further adjustment, drawing on international experience. An econometric model for evaluating the fiscal consequences of the shift to progressive dividend taxation is constructed based on an analysis of data on declared dividend income and tax revenues across the constituent entities of the Russian Federation. The scientific novelty of the research lies in synthesizing the results of our study of international mechanisms for preferential dividend taxation to identify sources of potential risks and systemic vulnerabilities that should be considered when developing proposals to improve dividend tax policy. The paper systematically categorizes and critically analyzes international practices and empirical research on possible approaches to dividend taxation, while also assessing the fiscal implications of their potential implementation for the Russian budget. We identify directions for optimizing the personal income taxation of dividends, taking into account the need to adhere to the principles of tax neutrality and equity. The research pays particular attention to the risks associated with the development of tax avoidance schemes. This provides the basis for further building analytical models to identify constituent entities of the Russian Federation with the possible use of “dividend-based” tax avoidance strategies by individual entrepreneurs.

Dividends, tax neutrality, profit distribution, fiscal federalism, tax policy, income taxation, tax preferences, progressive taxation

Short address: https://sciup.org/147253449

IDR: 147253449 | UDC: 336.226.112.2, | DOI: 10.15838/esc.2026.1.103.11

Text of the scientific article Progressive taxation of dividends: The dynamics of fiscal effects and risks in 2022–2028

Being at the intersection of corporate profit taxation and personal income taxation, dividend taxation involves striking a delicate balance between eliminating double economic taxation on one hand, and preventing tax avoidance and inequality on the other. To mitigate the negative effect of double economic taxation of dividends, global practice has developed various approaches – from integrating corporate and income taxes to fully exempting dividends from taxation. However, investors can receive income not only in the form of dividends but also from the sale (or other disposal) of shares (capital gains). Achieving balance in taxing these types of income is crucial for upholding the principles of tax neutrality (ensuring that investment decisions are not affected by tax considerations) and fairness (ensuring that taxpayers with similar incomes bear a similar tax burden) (Goncharenko, 2024).

Russia’s transition to progressive rates of personal income tax (PIT) has resulted in preferential taxation of most investment income (including dividends) compared to earned income. However, on a global scale, dividends are increasingly viewed as ordinary income that should be taxed at standard income tax rates. For example, in Norway, the dividend tax rate was raised by 2 percentage points to reduce the gap between marginal tax rates on capital income and wages: “Income from stocks and shares is highly concentrated among those with high incomes and wealth, and an increased dividend tax will therefore contribute towards a more redistributive income tax”1.

In the USA, there is also discussion about equalizing tax rates on dividends and earned income for wealthy taxpayers who receive the largest share of dividend income (raising the rate from 20% to 39.6%)2. At the same time, there are proposals to lower the dividend tax rate from 20% to 15% to stimulate economic growth through taxes on investment income3.

In Russia, there is also intense debate about the optimality of the current tax regime and directions for its reform. The proposals being put forward cover virtually the entire spectrum of possible options: from exempting dividends from taxation to setting a rate of 35% to achieve greater tax fairness. The lack of consensus underscores the importance of rethinking international experience, considering alternative models and their modifications to suit Russian current economic development goals.

The aim of the research is to provide, based on accumulated empirical data, an assessment of how the transition to a progressive PIT scale has affected tax revenues from dividends, and to identify sources of potential risks that should be considered when evaluating proposals to improve their taxation. Research objectives: to conduct a retrospective analysis of the fiscal consequences of transitioning to progressive dividend taxation; to provide a prospective assessment of the consequences of lowering the threshold for the 15% PIT rate on dividends for the period 2025–2028; to assess, based on the author’s systematization of foreign methodological tools for dividend income taxation, feasibility of their implementation in the Russian tax system.

The scientific interest lies in the developed counterfactual model for assessing the fiscal consequences of transitioning to progressive taxation, which allows for an empirical fiscal assessment of PIT revenues from dividends in Russia. The novelty also includes the results of a critical analysis of the feasibility of implementing elements of foreign methodological tools for preferential dividend taxation in Russia. In the context of proposals for further changes to dividend taxation, foreign practices and empirical research are systematized, and the fiscal effects for the Russian budget are assessed. Directions for optimizing dividend income taxation are identified, considering the need to adhere to the principles of tax neutrality and fairness. Particular attention is paid to identifying risks in the development of tax avoidance schemes.

Literature review

Regarding the fairness of preferential taxation of investment income, two principal approaches can be distinguished.

A number of researchers characterize dividends “as ‘super-incomes’, since the average level of dividend income per recipient significantly exceeds the average wage per worker”4. “The source of such super-incomes are dividend payments, income from owning and selling securities and other property, and other income not related to wages” (Panskov, 2020). At the same time, “significant dividend income is paid out to individuals owning shares (stakes) in enterprises in the fuel-energy and metallurgical sectors, as well as enterprises producing mineral fertilizers, etc.” (Topchi, 2022). For these reasons, “an increased rate should be set on total annual income, including income in the form of dividends, interest on deposits, on shares, from the sale of property and securities” (Panskov, 2020). Uniform taxation of all personal income regardless of its origin would make the process of determining tax liabilities more transparent and simplify tax administration (Ordynskaya, Cherkovets, 2023).

Those who contribute to this viewpoint propose not only to “ensure equality of taxation for different types of income” and to unify the taxation of wages and capital income but also to introduce additional tax brackets for ultra-high incomes (Semenova, 2025), or simply to increase the tax on dividends to 35%, as for income from large winnings5. Such proposals aim to make dividend taxation contribute more to reducing inequality, as the implemented reform has had almost no impact on income concentration and key income stratification indicators (Gini and Palma ratios, share of low-income population).

Other researchers, conversely, propose to improve the investment climate by “temporarily removing the restriction ... for setting the 13% rate and not setting the 15% rate” (Popova, 2022), resulting in dividends being taxed at a lower rate than capital gains from share sales. To encourage citizens to make long-term rather than speculative investments without reference to other characteristics of securities, some even propose introducing a regressive scale for dividend tax depending on the investment period: taxing dividends at an 8% PIT rate if shares are held for more than 3 years, 3% for more than 5 years, and 0% for more than 7 years (Milogolov, Berberov, 2022).

Both positions are largely unsupported by empirical data; however, foreign empirical studies show that reducing the maximum dividend tax rate provides only a modest stimulus for investment due to moderate investment elasticity (Koivisto, 2023; Isakov et al., 2020; Lee, Hong, 2020). There is also a slight increase in capital and labor inputs in small and micro-businesses, along with improved productivity (Jacob, 2020), and individual shareholders supervise the efficiency of resource allocation more actively (Kong, Ji, 2021; Kong, Ji, 2024). However, all these effects are relatively shortterm and ultimately lead merely to budget losses (Ghilardi, Zilberman, 2024).

A drastic increase in the dividend tax rate (as in France in 2013, when the rate rose from 15.5% to 46%) leads to a sharp reduction in dividends and the use of saved funds for increased investment, especially when good growth opportunities exist (Matray, Boissel, 2020). Analysis shows that virtually no company reduced investment after the tax increase. Thus, the assumption that higher dividend taxes suppress investment is refuted. On the contrary, tightened dividend taxation can, under certain circumstances, stimulate profit reinvestment.

Research methods and data

For counterfactual modeling of the fiscal consequences of transitioning to progressive taxation, we use retrospective empirical analysis of statistical tax reporting data from the Federal Tax Service of Russia (FTS) for the Russian

Federation as a whole and by constituent entities: data from forms No. 5-NDFL, No. 7-NDFL (2016–2024), No. 5-P (2012–2024), No. 1-NM (2023–2025).

The fiscal consequences of transitioning to progressive taxation regarding dividends ( LFiscr ) can be estimated as the difference between actual tax receipts from dividends and the estimated amount that budgets could have received if the PIT rate had remained flat:

№iscr = ^ (T ratcc’13 t=2022

acc,15 + T r,t

—

T/n, (1)

where: T“ tcc,13 and Т^,15 are the actual amounts of PIT from dividends within 5 million rubles and above, respectively, received in 2022–2024;

T^1 т Да1 is the estimated amount of tax revenue that could have been received if the flat PIT scale had been retained.

To average the effect, we take into account the aggregate actual FTS data for 2022–2024 from form No. 7-NDFL. However, it provides only aggregated data on dividends taxed at the 15% rate, which does not allow separating dividends paid to residents and non-residents. Since this is necessary for modeling the fiscal effect, we introduce an additional variable ( 9r ), reflecting the average share of dividends paid to non-resident individuals taxed at 15% in the structure of dividends paid by Russian organizations in region r in 2016–2021:

у2021 15

n ________ ^ t=2016 D1r,t ________

°Г = Х^М^^^ (2)

where: DI^t , DI^ and DI^ are the aggregate dividends taxed in region r at rates of 13%, 15%, and other rates stipulated by double tax treaties, respectively.

The following calculations can then be made:

KT™ = Т^-Ст^ , (3)

T^c,15 = (1 - вг ) х T 15 t - С^ , (4)

т^ = (ы™ + (1 - ег ) х Dl l’ ) х х 0,13 - С^ - Сг^

where: Т 13 is the amount of PIT calculated in region r in year t from dividends within 5 million rubles paid to residents (i.e., taxed at 13%);

Т ^5 is the amount of PIT calculated in region r from dividends paid to residents exceeding 5 million rubles, and to non-residents (i.e., taxed at 15%);

Cr^ and Cr^ are the amounts of corporate profit tax withheld on dividends from subsidiaries and subject to offset against dividends taxed at rates of 13% and 15%, respectively.

The results of the structured model can be analyzed using descriptive statistical methods (absolute and relative growth rates, mean and median regional changes, assessment of effects concentration across regions).

To forecast changes in PIT amounts resulting from the reduction in the threshold for applying the 15% PIT rate in 2025, we extrapolate data on PIT amounts for the same period of the previous year:

rp acc,13 rr>acc,15

^ tot _ _0r4O24_ „азе,13 _^_r,2024_ „acc,15 ,£4

Jr,2025 — „acc,13 * Jr,9M2025 + „acc,15 * 1 r,9M2025 , (6)

7r,9M2024 7r,9M2024

where: 7 ^,2025 is the predicted total amount of PIT that will be received by the budget in region r in 2025 from dividends taxed at rates of 13% and 15%.

To forecast PIT revenues from dividends for 2026–2028, we use data from scenario forecasts by the Russian Ministry of Economic Development on the projected profit of profitable organizations6:

7* tot totot ^SC,t

ISC,r,t = 2 r,2025 A p $ ,

where: T^ t is the forecasted total amount of PIT from dividends in year t in the baseline or conservative scenario ( SC );

Psc t and Psc , 2025 are the forecasted profit of profitable organizations in year t in the baseline or conservative scenario ( SC ).

The qualitative component of the research is based on the author’s systematization and classification of foreign methodological tools for dividend taxation. A comparative analysis of foreign approaches to dividend taxation is used, with an assessment of the fiscal consequences of their introduction in Russia based on statistical tax reporting data.

Research results

The modeling results show that, due to the transition to progressive dividend taxation in 2022– 2024, the Russian budget system received approximately additional 186.1 billion rubles (PIT from dividend income increased by 11.46%, to 1.81 trillion rubles compared to 1.62 trillion rubles with the flat scale). Although this increase is a purely static result, it allows estimating the maximum potential benefit from the transition to progressive taxation, whereas the actual increase may be smaller if high-income individuals adjusted their behavior or found ways to optimize their tax burden.

At the regional level, the average increase in PIT from dividends paid to tax residents was about 9.1%, and the median change was about 10.1%, meaning that in half of the Russian regions, the income increase from transitioning to progressive dividend taxation exceeded 10%. However, this result varies significantly depending on the share of high-income individuals in the total number of taxpayers.

Nearly 60% of the nationwide increase in PIT from dividends came from three regions: Moscow, where tax revenues from dividends grew by 78.7 billion rubles (an increase of 12%, accounting for about 42% of the nationwide increase); Saint Petersburg (18.3 billion rubles, or 11%7, about 9.8% of the nationwide increase); and Moscow Region (13.16 billion rubles, or 11%).

Among other regions with the largest increases in the PIT tax base from dividends are the Krasnodar Territory (5.4 billion rubles, or an 11.6% increase), the Sverdlovsk Region (5.15 billion rubles, or 11.6%), and the Republic of Tatarstan

(4 billion rubles, or 11%). The highest growth rate was in the Kaliningrad Region (2.5 billion rubles, or 13.7%), which may be explained by the active development of the special economic zone and the re-registration of holding companies there.

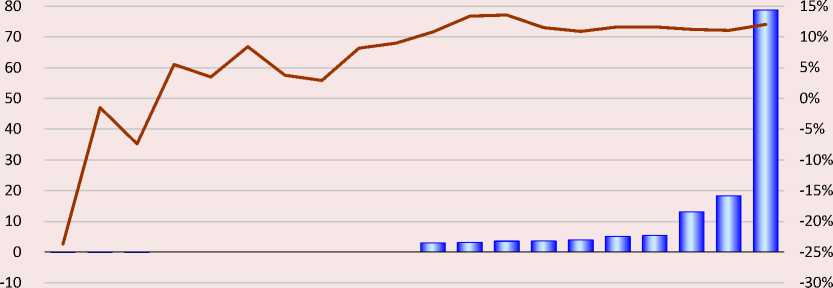

In three regions, total tax revenues from dividends, conversely, decreased ( Fig. 1 ): republics of Ingushetia (by 23.7%, or 17.9 million rubles), Tyva (by 7.4%, or 7 million rubles), and North Ossetia-Alania (by 1.5%, or 7.3 million rubles). A peculiarity of these regions is that a relatively small portion of dividend income falls into the top bracket of the progressive scale (15%).

Figure 1. Regions with the smallest and largest changes in tax revenues from dividends due to the transition to the progressive PIT scale

Absolute change in tax revenues, billion rubles Relative change in tax revenues, %

Calculated based on: FTS Russia form No. 7-NDFL data.

д%““1 =

^ sub I Tfe d _

sub,flat 't

T sub, flat

Starting in 2025, the threshold for applying the 15% rate was halved (from 5 million rubles to 2.4 million rubles); however, no significant increase in tax revenues is expected. On the contrary, they may decrease by 79 billion rubles (from 905 to 826 billion rubles). The largest decrease will be in tax receipts from dividends up to 2.4 million rubles (by 30%, from 151 billion rubles to 106 billion rubles), while dividends above 2.4 million rubles will decrease by only 4.5% (from 753.7 billion rubles to 720 billion rubles). The decline is mainly associated with an objective 6.9% reduction in the balanced financial results of companies’ activities8 and, consequently, lower dividend distributions. At the same time, the lowering of the threshold for the 15% rate led to an increase in the share of dividends taxed at this rate from 83.3% in 2024 to 87.2% in 2025.

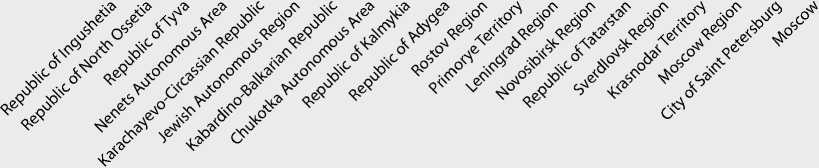

However, the regional results of adjusting the tax scale are mixed. Revenues from dividends taxed at the 13% rate will decrease by 20–40% in most regions

(65 out of 85 analyzed); in 5 regions they will decrease by 10–17%, and in the remaining 16 by 41–82%. For dividends taxed at the 15% rate, conversely, tax revenues will increase in 40 regions (including more than doubling in 6 regions – Chechen Republic (585%), Republic of Dagestan (174%), Jewish Autonomous Region (173%), Republic of Sakha (Yakutia) (126%), Kostroma (125%) and Vladimir (106%) regions), while they will decrease in 45 regions (including more than halving in 4 regions – Orel (73%), Vologda (59%), Kaliningrad (51%) regions, and Republic of Buryatia (51%)). Consequently, tax revenues will increase in about one-third of regions and decrease in two-thirds ( Fig. 2 ).

Divergent results of the adjustment once again confirm that taxpayer behavioral responses to changes in dividend taxation largely depend on company size, number of shareholders, and the role of minority shareholders in governance (Hillmann, 2023; Lee, 2022; Berzins et al., 2019).

Figure 2. Distribution of regions by growth rates of PIT revenues from dividends in 2025 compared to 2024

Compiled based on: FTS Russia form No. 1-NM data.

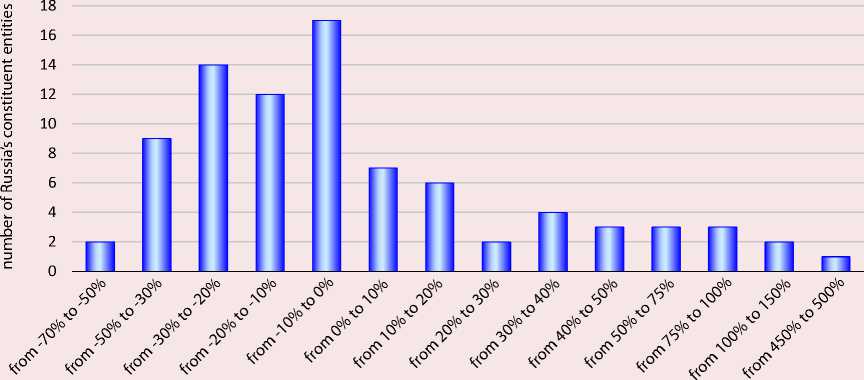

Figure 3. Dynamics of PIT revenues under different scenarios of economic changes

■ ■ PIT revenue from dividends taxed at 15% rate

PIT revenue from dividends taxed at 13% rate

■■■■■■ ^^a Forecast of the total PIT revenue from dividends in a conservative scenario

* Estimated value based on 9 months of 2025 data.

** Forecasted PIT revenue.

Calculated based on: FTS Russia form No. 1-NM data.

A prospective analysis of PIT revenue development from dividends for 2026–2028 was conducted according to baseline and conservative scenarios for projected growth in corporate profits. In the baseline scenario, tax revenues from dividends in 2026 will remain virtually unchanged (about 831 billion rubles, +0.6%; Fig. 3 ). In 2027, they will slightly exceed the PIT level before the tax scale adjustment (about 911 billion rubles, +9.6%), and by 2028 will reach 991 billion rubles (+8.8%).

The conservative scenario predicts a slightly faster recovery in tax revenues (about 866 billion rubles, or +4.8% in 2026) but slower growth rates in subsequent years: 934 billion rubles (+7.9%) in 2027 and 991 billion rubles (+7.4%) in 2028. Nevertheless, both scenarios ultimately yield almost identical forecast values.

The conducted estimates allowed assessing prospective dynamics of PIT revenues from dividends under given tax conditions and a changing economic situation. However, it is also necessary to analyze the fiscal consequences of fundamental changes in approaches to dividend taxation.

Discussion

Evaluation of proposals for further progressive dividend taxation reform in the context of global experience

Russia long used a relatively neutral and simple “classical” tax system, where dividends were taxed at the same personal income tax rates as wages. This system led to double economic taxation of dividends but was intended to encourage companies to retain and reinvest profits. However, practice showed that Russian companies, on the contrary, distributed an increasing share of profits as dividends: dividend payouts fluctuated within 40–60% of net profit, and this share could jump to 80–90% in anticipation of large-scale restructuring. One reason for this was the predominance of intercorporate dividends taxed at 0% (53–62%) and, conversely, the low share of dividends paid to resident individuals – about 8–12% ( Fig. 4 ).

Figure 4. Dynamics of dividend payouts structure of Russian companies

■ ■ Share of dividends paid to Russian tax residents in the structure of dividends paid by Russian organizations

■ ■ Share of intercorporate dividends subject to corporate income tax at a rate of 0% in the structure of dividends paid by Russian organizations онм^^ш Share of Russian organizations' profits distributed as dividends to all shareholder groups (right scale)

Compiled based on: FTS Russia form No. 5-P data.

Although globally the “classical” system is still prevalent (adhered to by about 14% of countries, accounting for ~37% of global GDP)9, it is increasingly complemented by measures for finetuning capital income taxation to ensure fair distribution of the tax burden, overall tax neutrality while preserving targeted tax incentives, and elimination of tax avoidance schemes.

The ratio of PIT rates on dividend income, capital gains on shares, and wages established since 2025 corresponds to the practice of most economically developed countries. It reflects the most common form of partial relief from double economic taxation of dividends (Shareholder Relief

Systems) – setting lower rates for them compared to standard income tax rates (Hourani et al., 2023). At the same time, both dividends and capital gains from share sales are taxed at a single reduced rate relative to earned income to ensure neutrality in their taxation. Besides Russia, this approach is followed by about 18.5% of countries, representing roughly 36% of global GDP, including Germany, Italy, Spain, Austria, Denmark, Poland, France, and China. For example, in Germany, most capital income (dividends, interest, capital gains) is taxed at a flat rate of 25%, not the progressive scale up to 45%10; in Italy, capital income is taxed at 26%, not the progressive scale up to 43%11.

The level of the maximum PIT rate on dividends for residents (15%) was linked to the tax rate on dividends paid to non-residents as an element of preventive action against tax avoidance using foreign jurisdictions12. This is a simple but rather controversial criterion, found mainly in developing countries (Barbados, Hungary, Guinea, Zimbabwe, Costa Rica, Lithuania, Malta, Nicaragua, Pakistan, Papua New Guinea, Republic of Congo, Rwanda, Sao Tome and Principe, Serbia, Montenegro, Czech Republic, Uganda, Jamaica).

Taxing dividends at a lower rate than capital gains from share sales is found in about 20% of developing countries, accounting for less than 6% of global GDP (Indonesia, Philippines, Czech Republic, and a number of others). This may create an incentive to hold shares for dividends rather than selling them for capital gains. In Russia, implementing such a proposal would lead to a reduction in federal budget revenues of about 98 billion rubles annually and in regional and municipal budget revenues of 2.5 billion rubles annually. The largest decline in revenues would be experienced by the regional and municipal budgets of Moscow (-1 billion rubles), Saint Petersburg (-260 million rubles), and the Moscow Region (-208 million rubles).

This effect would only be noticeable with a sufficiently large difference in rates. For instance, in Indonesia, dividends are taxed at 10%, while capital gains are taxed at 35%. Domestically, dividends may be fully exempt from taxation if reinvested or if below certain thresholds13. In the Czech Republic, dividends are taxed at 15%, while capital gains (from shares held for a certain period or from a significant block of shares) are taxed at the main income tax rate14. In Ireland, dividends are taxed at 25%, while capital gains are taxed at 40%.

Analysis of global practice shows that about 11% of countries, accounting for about 1.4% of global GDP, tax dividends at higher personal income tax rates than capital gains. This approach is not used in developed economies because a mature financial market typically features a large number of income-oriented investors, whereas emerging markets are more focused on capital growth itself. To encourage this, profit reinvestment is promoted through the “lock-in effect”: it becomes more beneficial for shareholders when companies retain profits (leading to share price growth) rather than distribute dividends.

However, such an effect can, conversely, reduce share liquidity and lead to potential overcapitalization of companies, which is why this approach is relatively rare and found only in growing economies. For example, in Colombia, dividends are taxed at progressive rates from 0 to 39%, while capital gains are taxed at 15%15. Other countries with this approach include Vietnam, Zimbabwe, Laos, Rwanda, Chad, and South Africa. However, in practice, a significant effect from stimulating profit reinvestment is not noticeable in these countries. Often, companies simply hoard cash or buy back their own shares because paying dividends is disadvantageous from a tax perspective.

In Russia, the lock-in effect may also be insignificant due to the predominant share of intercorporate dividends (53–62%) and the low share of dividends paid to individuals (8–12%) in the structure of dividends distributed by Russian firms16. On the contrary, it may only stimulate tax avoidance.

Immigration Guide.

Immigration Guide.

Prospects for partial exemption of dividends from taxation

Partial relief from double taxation of dividends can also be implemented by taxing only a portion of dividends (with the remaining portion taxed at the standard income tax rate). The exempt amount can be expressed in absolute terms (a minimum non-taxable amount, which can be indexed annually) or relative terms (a specific proportion of dividends received).

Relative exemption of dividends is used in Luxembourg and Portugal (50% of dividends received by residents)17. In Switzerland, 30% of dividends are exempt from taxation at the federal level if the shareholder holds at least 10% of the company’s shares18. In Finland, 15% of dividends from public companies are exempt from taxation (actually, only the remaining 85% of dividends are subject to income tax)19. By reducing the tax base, the effective tax rate on dividends is lowered.

In developed countries, absolute dividend exemptions are more targeted at small, retail investors. For example, in the UK, the tax-free dividend allowance was reduced from £2000 to £1000 in 2023, and then to £500 in 2024 (~63 000 rubles)20. In Belgium, conversely, the tax-free allowance is indexed slightly – from 833 euros in 2024 to 859 in 2025 (~79 000 rubles)21.

Developing countries often set high tax-free thresholds, aiming to practically exempt typical investors from taxation entirely. For instance,

Immigration Guide.

Immigration Guide.

Immigration Guide.

Kazakhstan indexes its tax-free threshold annually; in 2025 it amounted to 117 960 000 tenge (~23 million rubles)22. Such an extremely high ceiling means that most individual investors pay no tax on dividends unless they are very large shareholders. In Colombia, dividends equivalent to 1090 units of tax value (Unidad de Valor Tributario) were exempt from taxation in 2025, equivalent to over 54 million Colombian pesos (~1.3 million rubles)23. In Malaysia, dividends up to 100 000 ringgits (~2.2 million rubles) are exempt from tax since 202424, in Tunisia – 10 000 Tunisian dinars (~310 000 rubles)25.

The vast difference in the size of dividend taxfree thresholds reflects differences in tax policy: European countries are more focused on supporting small investors and the middle class overall, while developing countries aim to create a favorable investment environment even for fairly large investors to attract or retain capital in their markets.

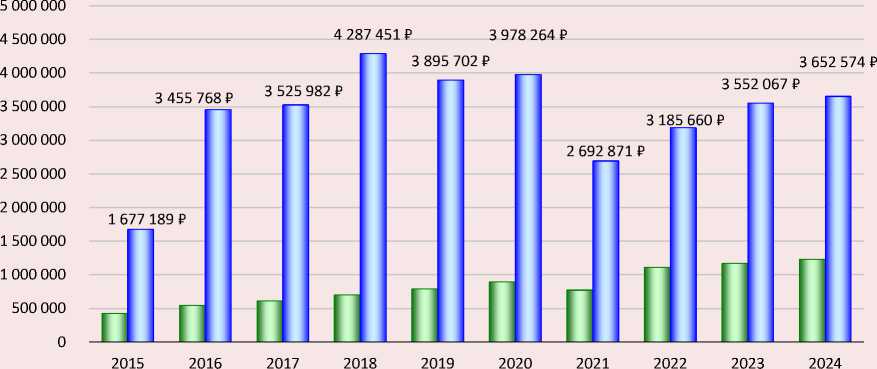

For Russia, introducing a tax-free threshold for dividends (possibly tied to an investor’s average dividend income) could also be a tool to encourage public investment in shares while limiting such benefits for very large investors. The average size of dividends paid to individuals has been steadily growing and exceeded 1.2 million rubles per taxpayer ( Fig. 5 ).

However, setting a tax-free threshold of, for example, 100 thousand rubles would lead to forgone revenues for regional and municipal budgets of up to 537 billion rubles26. It should be considered that a significant tax reduction typically results in income shifting between wages and dividends (Koivisto, 2025). For this reason, a tax-free threshold would not so much stimulate the development of individual investments in the stock market as increase the efficiency of tax avoidance schemes, particularly among individual entrepreneurs, whose national average dividend size has already exceeded 3.6 million rubles per taxpayer, and is even higher regionally: 57.7 million rubles per individual entrepreneur in Kaliningrad Region; 54 million rubles – in Magadan Region; 33 million rubles – in Sakhalin Region27.

Given that the average level of dividend income per taxpayer exceeds the average wage per taxpayer, regressive taxation would exacerbate income inequality between the majority of the population earning only wages and wealthy individuals with high passive incomes. Regressive dividend taxation would discourage earned income and increase opportunities for tax arbitrage, encouraging to distribute dividends instead of paying wages to minimize taxation. This could have long-term negative consequences: undermine progressive income tax policy and reduce tax revenues.

Risks of full exemption of dividends from taxation

One radical deviation from the classical model is the Dividend Exemption System, where dividends to shareholders are fully exempt from personal income taxation. Within this system, corporate profit tax is considered the final tax on distributed income, and if profit is paid as dividends, it is not taxed again for any shareholder (whether individual or corporate). From an economic viewpoint, this completely eliminates double economic taxation of dividends – income is taxed only once at the

Figure 5. Dynamics of the average size of dividends paid to individuals, rubles

□ Average size of dividend payouts per individual tax resident of the Russian Federation

□ Average size of dividend payouts per individual entrepreneur

Calculated based on: FTS Russia form No. 5-NDFL data.

corporate level. Under this approach, dividends are viewed as a recovery of money invested or as a non-taxable transfer of already-taxed profit. The presumed goal is typically to stimulate equity investment by increasing the after-tax return on shares and neutralizing the advantages of debt financing over equity financing (since capital income is taxed no higher than interest on loans).

In practice, only about 13% of countries (comprising roughly 3.5% of global GDP) use this system. Most are small, open economies or financial centers seeking to attract international investment through tax incentives. For example, in Hong Kong, Cyprus, and Singapore, it is part of a broader low-tax strategy for investment income28.

Brazil was the only large economy where dividends were not subject to personal income tax from the mid-1990s, with Brazilian companies instead paying a higher corporate tax29. But in May 2025, it announced a reform under which dividends would be taxed at a 10% rate. Slovakia (2004–2017), India (1997–2020), and Uzbekistan (2022–2024) also experimented with exempting dividends from taxation but ultimately restored the dividend tax.

The main advantage of this system is ensuring neutrality in dividend taxation:

– elimination of an extra layer of equity income taxation ensures neutrality in the choice between debt and equity financing;

– companies can make decisions on dividend payments or reinvestment based on business needs, not tax considerations;

– slight simplification of the mechanism for taxing and administering personal income.

However, these benefits come with significant costs and risks, which is why this system has not gained wide acceptance.

First, there is a high forgone tax revenue, especially in countries with significant dividend payouts. Only jurisdictions confident in their ability to otherwise compensate for lost revenues or willing to sacrifice them to enhance the country’s tax competitiveness can absorb this strike. For example, in Malaysia, dividends were exempt from taxation from 2008, but due to a budget deficit, it was decided to abandon this in 2024. Instead, a modest 2% tax on dividends exceeding 100 000 ringgit per year (~2.3 million rubles) was introduced30. Given that dividends below this limit remained exempt, the change is clearly aimed at the wealthiest residents.

Second, there is high potential for abuse and tax arbitrage. To take advantage of the exemption, certain groups of high-income taxpayers may attempt to reclassify other types of income as dividends. In Brazil, the phenomenon of pejotiza^ao (a term derived from “Pessoa Juridica” — “legal entity”) emerged, when individuals (e.g., lawyers, doctors, engineers) began creating shell companies to channel their, in fact, earned income into corporate profit, which was then distributed as taxexempt dividends31. Employers began terminating employment contracts with their employees and then hiring them as representatives of small companies, converting salaries (taxed at progressive rates up to 27.5%) into tax-exempt dividends.

Such a tax avoidance strategy became so widespread that it not only undermined the personal income tax base but also led to horizontal inequality, because other workers performing similar jobs (e.g., in the public sector or companies not using such schemes) continued to pay full personal income tax. As a result, for the wealthiest Brazilian citizens, the effective personal income tax rate became extremely regressive: while for 99% of the population the effective rate steadily increased up to 12.3%, for the top 0.05% of the ultra-wealthy who could utilize the dividend exemption, it, conversely, sharply dropped to about 7%32.

This distortion not only sparked debates about the fairness of such tax policy but also required labor law reform and anti-tax avoidance measures. Ultimately, in 2025, a tax reform was proposed, including not only the introduction of a 10% tax on dividends but also the establishment of a minimum effective tax rate for high-income individuals. As a result, individuals with large previously tax-exempt dividends would have to pay at least a base tax33.

Third, dividend exemption disproportionately benefits wealthy investors and exacerbates income inequality. Capital ownership (and receipt of dividends) is typically concentrated in high-income households, and exempting dividend tax allows the wealthiest individuals to pay less tax relative to their total income. Since capital income is distributed more unevenly than labor income, not taxing it undermines the progressivity of the tax system and can worsen inequality (Hourani, Perret, 2025). This was evident in Brazil and is a primary reason why other countries also combine dividend tax reform with other, broader measures regarding wealthy citizens’ income.

Fourth, dividend exemption encourages profit distribution rather than reinvestment. It is usually considered beneficial for investors if profits are reinvested to ensure company growth. However, in the case of tax-exempt dividends, shareholders, on the contrary, pressure the company to distribute profits, allowing them to receive income tax-free. This contradicts the idea of using the tax system to stimulate investment and can lead to corporate decapitalization. Essentially, dividend payments would be used as a way to extract corporate capital. Such concerns were one of the reasons for abolishing the dividend tax exemption in Malaysia.

A unique solution to this problem exists in Estonia, where profit is subject to a 20% corporate tax only upon distribution34. Effectively, profit taxation is deferred until dividends are paid, with the shareholders themselves exempt from tax. Such a model of corporate tax with separate rates for distributed and retained profit (Split Corporate Tax Rate System) ensures tax neutrality and genuinely stimulates profit reinvestment. Exempting company profits from taxation until distribution resembles a cash flow tax. However, this model has its own drawbacks. Estonia is forced to use strict anti-tax avoidance rules to prevent masking non-commercial expenses or owner payments as deductible expenses.

Given all these disadvantages, most countries eventually abandon full dividend tax exemption. Therefore, proposals heard in Russia to exempt dividends paid to individuals from taxation should be considered cautiously. Their implementation would result in forgone revenues of 905 billion rubles annually, including 98 billion rubles from the Russian federal budget35. Moreover, it would not lead to an “influx of domestic and foreign capital due to increased interest in creating organizations” (Nasyrov, Shtyrlyaeva, 2015) but would stimulate the development of tax avoidance strategies. One should agree with researchers who note that “full exemption of dividends without harmonization with the capital gains taxation mechanism will lead to new types of distortions, as it will become more beneficial for companies to distribute all profits to shareholders, which may reduce the volume of reinvested profit” (Milogolov, Berberov, 2022).

Conclusion

The conducted analysis allows making a number of conclusions which contribute to further study of dividend income taxation.

The proposed model for assessing the fiscal consequences of transitioning to progressive dividend taxation showed that tax revenues of the consolidated budget increased by 186.1 billion rubles over three years. At the same time, the tax base is distributed extremely unevenly: nearly 60% of the increase comes from three regions – Moscow, Saint Petersburg, and the Moscow Region. Those regions where holding companies actively reregister in special economic zones also benefited (Kaliningrad and Sverdlovsk regions, Republic of Tatarstan). Conversely, a decline in the tax base was experienced by regions where a small portion of dividend income fell into the top bracket of the progressive scale (republics of Ingushetia, Tyva, North Ossetia-Alania).

In the case of a return to a flat scale for taxing dividends, shareholders would not receive a significant incentive for long-term shareholding due to the relatively small difference in rates. Meanwhile, federal budget revenues would decrease by about 98 billion rubles, and regional and local budget revenues by 2.5 billion rubles.

If dividends are viewed as “super-incomes” and their tax rate is raised to 35%, there would be a “lock-in effect” because shareholders would benefit from companies retaining profits and from rising share prices. However, at a macroeconomic level, this effect would not be significant due to the predominance of tax-exempt intercorporate dividends (53–62%) in the structure of dividends of Russian organizations, while the share of dividends paid to individuals is only 8–12%.

In developed countries, tax-free thresholds are used to stimulate investment activity among small retail investors. However, in Russia, establishing a tax-free threshold of, for example, 100 thousand rubles would lead to forgone revenues for regional and municipal budgets of up to 537 billion rubles.

When determining directions for further reform of dividend income taxation, one should remember the high potential for income transfer between wages and dividends. For instance, the average dividend size among individual entrepreneurs (3.6 million rubles per taxpayer) already far exceeds the national level (1.2 million rubles). Regionally, this difference is even higher: 57.7 million rubles per individual entrepreneur in the Kaliningrad Region; 54 million rubles in the Magadan Region; 33 million rubles in the Sakhalin Region. With the transition to progressive taxation, more attention should be paid to schemes for reclassifying business owners’ earned income as dividends.

Proposals to exempt dividends from taxation would not only result in forgone revenues of 905 billion rubles annually, including 98 billion rubles from the federal budget, but would additionally stimulate tax avoidance schemes. For example, encouraging individuals to create shell companies to channel their, in fact, earned income into corporate profit and then distribute it as taxexempt dividends.