An Analysis of the Potential for Rebalancing Strategy to Generate Premium Returns in Long-Only Portfolios

Автор: Mingxi H.

Статья в выпуске: 2, 2026 года.

Бесплатный доступ

The primary purpose of rebalancing strategies in long-term investing is risk aversion, but investors also expect to generate excess returns or premium returns through rebalancing strategies. The article analyzes the probability of premium returns from rebalancing strategies using pure long-only portfolios. Rebalancing Alpha can be used to assess the likelihood of obtaining premium returns. A positive rebalancing Alpha indicates that the rebalancing strategy can generate premium returns. Therefore, the higher the probability of a positive rebalancing Alpha, the greater the likelihood of premium returns from the rebalancing strategy. We have analyzed both the simple two-asset model and the general model. It shows that for a long-only portfolio of two assets the probability of a positive rebalancing Alpha is approximated as a t-distribution with M-1 degree of freedom where M is the investment period. While for a multi-asset long-only portfolio the rebalancing Alpha of a portfolio is the sum of the rebalancing Alphas of all different asset pairs. The probability of the positive portfolio rebalancing Alpha is equal to the product of probabilities that the rebalancing Alphas of all asset pairs are positive. Therefore, the conditions for a positive rebalancing Alpha are very stringent. Even if a positive rebalancing Alpha exists, its value is usually very small and its duration is very short. This explains why, in practice, investors find it difficult to obtain premium returns from rebalancing strategies.

Rebalanced portfolios, long-only portfolios, rebalancing Alpha, rebalancing strategies, premium returns

Короткий адрес: https://sciup.org/148333558

IDR: 148333558 | УДК: 336.76 | DOI: 10.18101/2304-4446-2026-2-160-166

Анализ потенциала стратегии ребалансировки для получения премиальной доходности в портфелях с длинными позициями

Основной целью стратегий ребалансировки в долгосрочном инвестировании является снижение риска, однако инвесторы также рассчитывают на получение избыточной, или премиальной, доходности за счет применения стратегий ребалансировки. В статье анализируется вероятность получения премиальной доходности от стратегий ребалансировки с использованием исключительно «длинных» портфелей (long-only). Для оценки вероятности получения премиальной доходности используется показатель альфы ребалансировки (rebalancing Alpha). Положительное значение альфы ребалансировки указывает на способность стратегии ребалансировки генерировать премиальную доходность. Следовательно, чем выше вероятность положительной альфы ребалансировки, тем выше вероятность получения премиальной доходности в результате применения стратегии ребалансировки. В статье рассматриваются как простая двухактивная модель, так и обобщенная модель. Показано, что для longonly портфеля, состоящего из двух активов, вероятность положительной альфы ребалансировки аппроксимируется 𝑡-распределением с числом степеней свободы М-1, где М — инвестиционный период. В случае многоактивного long-only портфеля альфа ребалансировки портфеля представляет собой сумму альф ребалансировки всех возможных пар активов. Вероятность того, что портфельная альфа ребалансировки является положительной, равна произведению вероятностей того, что альфы ребалансировки всех пар активов положительны. Таким образом, условия получения положительной альфы ребалансировки являются весьма жесткими. Даже при наличии положительной альфы ребалансировки ее величина, как правило, очень мала, а период ее существования — крайне непродолжителен. Это объясняет, почему на практике инвесторам сложно получить премиальную доходность с помощью стратегий ребалансировки.

Текст научной статьи An Analysis of the Potential for Rebalancing Strategy to Generate Premium Returns in Long-Only Portfolios

A long-only portfolio is the most fundamental and common investment approach in the investment world. In the context of retail investing, this approach relies on the basic infrastructure of the stock market, which involves “mobilizing household funds” and encouraging “active investment of savings in securities” [1, p. 58]. It embodies the classic "buy and hold" philosophy, whose success relies on careful asset selection, diversification, and confidence in the long-term upward trend of the market. While it lacks the ability to hedge against market downturns, its simplicity, low cost, and longterm effectiveness make it a core strategy for most individual and many institutional investors. Rebalancing is also a common strategy used in long-term investing, aiming to mitigate the additional risk associated with weight drift. The practical adoption of rebalancing is further supported by digital investment services; such tools “lower the entry threshold for clients in the investment market” [2, p. 132] and make it possible to “balance the client’s accounts by automating the calculation of security purchases and sales” [2, p. 135]. In practice, investors often experience temporary premium returns on long-only portfolios over the long term, often referred to as rebalancing Alpha [7]. For example, during the 2008 financial crisis, investors who rebalanced during 2008 experienced a premium return due to a strong rebound in 2009 after a period of sustained stock market decline [4; 8]. However, such premium returns are not frequent, and whether rebalancing strategies can generate premium returns has been a major research question for many scholars. Therefore, this paper analyzes whether rebalancing strategies can generate premium returns for long-only portfolios based on a mathematical approximation of rebalancing Alpha. The result can explain some of the practical phenomena that investors encounter when applying rebalancing strategies to long-only portfolios.

Long-only portfolios of two assets

A long-only portfolio generally involves buying a collection of stocks, bonds, or other assets that investors believe will appreciate in value, then holding on to them and waiting for them to rise. The long-only portfolio usually means that all assets have the positive weights in the portfolio. First consider a long-only portfolio with two assets. A common example is that investors will invest in stocks and bonds, such as the classic 60/40, which means that 60% of the assets will be held in stocks and the remaining 40% will be held in bonds [9]. Some investors allocate 60% of their funds to two stock strategies, such as a multi-factor equity index ETF and a wide-moat quality equity ETF. Others allocate 60% to two alternative strategies, such as a trend-following managed futures ETF and a market-neutral long/short beta strategy ETF [3]. When the portfolio has only two assets, the rebalancing Alpha can be simplified. Assume that there are two assets in the portfolio with weights w1 and w2 respectively, and w1 + w2 = 1. The volatility effect is shown as follows.

ev=^ (W 1 ^ 1 + ^2^2 - a2w)

= ^ [w-^ l + w2a2 — (w2a 1 + w^ H + 2w1w2p12a1a2)] 1

= 2W 1 W 2 (al+al — 2P 12 O 1 O 2 )

p12 is the correlation coefficient between two assets. The correlation coefficient is between —1 and 1. When the correlation coefficient is —1, the volatility effect is the maximum; When the correlation coefficient is 1, the volatility effect is the minimum.

Similarly, we can also calculate the value of return effect.

( M —1) (M— 1~)[W 1 (g 1 —g)2+W 2 (g 2 -g)2]

^ 2(1-g'^'-g' = ---------W+g)---------

= (M — 1)W 1 W 2 (g 1 — g 2 )2

= 2(1 + g)

Rebalancing Alpha = 2W1w2[(al+al — 2p12o1a2) — (M — 1')(g1 — g2)2]

-

1 [ ко? 1иф g иГ|

= -W1W 2 ff12 _2 1-------

-

2 o2 -2( 1 + g)

We define a variable in the above formula as statistic 1 1— 2.

~ JtM-tyCg i -9 2}

£1-2 * ~

^ 1-2

Therefore, it can be clearly seen that the positive or negative rebalancing Alpha is related to the size of t1-2. When the absolute value of the statistic t1-2 is less than 1, the rebalancing Alpha is positive; When the absolute value of the statistic t1-2 is greater than 1, the rebalancing Alpha is negative; When the absolute value of the statistic is equal to 1, the rebalancing Alpha is zero, which means that the geometric mean returns on the two assets are the same, and the incremental value of portfolio rebalancing reaches its maximum.

Rebalancing Alpha can also be approximated by the following formula.

Rebalancing Alpha = 2w1w2[(o'12+o'22 — 2p12a1a2) — (M — 1)(g1 — g2)2] 1

* ^vvgKa f+O — 29 12 0 1 0 2 ) — ( M — 1)0 1 — 9 2) 2 ]

= 2W 1 W 2 [O 1 2 -2 — (M — 1)9 1-2 ]

91-2 is the premium of asset A1 relative to asset A2. Assume that the difference in the returns of the two assets follows a normal distribution and is independently distributed in different periods. The expectation of the sample mean is the population mean, and the variance of the sample mean is ^ of the population variance. Then we can get that the sample mean also follows a normal distribution.

9 1-2 ~ ^ ^9 1-2 ,

° Г-2 M

■)

The sample variance follows a chi-square distribution.

Si2_?

(M — 1)-^~I2 -1 ° 1-2

Rebalancing Alpha can therefore be rewritten as follows.

1 Rebalancing Alpha * 2w1w2s £ -2

1 2

= 2W 1 W 2 S f-2

M —

M

M —

M

- и — ^СЭД

'(-M9g)

^ 1-2 (О) is a non- ce nt ra l t-distribution with M — 1 degrees of freedom, and its noncentrality parameter is s ho w n as follows.

VM^ i-2

О = ------

O1-2

Therefore, the p r ob a bi l it y of rebalancing Alpha being positive can be obtained from the probability of—1 < TM-1(6) < 1.

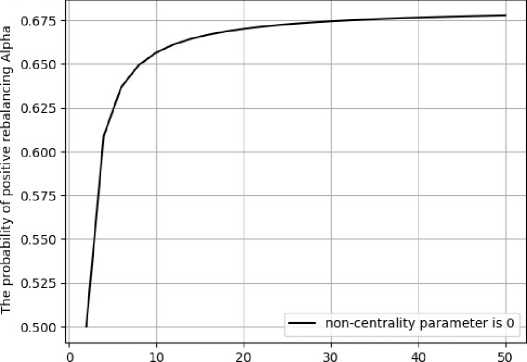

The probability of positive rebalancing Alpha when the expected returns of two assets are the same.

Investment period M

Figure 1. The re l ati on s hip between the probability of positive rebalancing Alpha and the investment pe rio d M when the expected returns of two assets are the same

It can be observed in Figure 1 that the probability of a positive rebalancing alpha is related to the investment horizon. When the non-centrality parameter is 0, the expected returns of the two assets are the same. The longer the investment horizon, the greater the probability of a positi v e rebalancing Alpha. However, the probability of a positive rebalancing Alpha re a ches a maximum of 0.68 at an investment horizon of approximately 50 and the n reaches equilibrium.

Long-only portfolios in general form. The problem can be extended to the long-only portfolios of m ult i pl e assets greater than two. The rebalancing Alpha of a long-only portfolios in g ene r a l form can be written as follows.

N = 2 ( z w i ° i 2

Rebalancin9 Alpha = ev — er

—

„ 2

° FW I

—

(M — 1)(1 + g- pr2

2(1 + g)M-1 Var(9)

1^ 21

= 2 f wiw7 [° i-j — (M — 1)(9i — 9') ] i<7

Similarly, we also h a ve the following statistics t 2._j .

ti-i

^(M — !)(g j - g j ) ^ i-i

1 N

R ebala n cin g Alpha = ^ ^ W i W j o' f -l(1 — Ь — ) i

Intuitively, the r e ba l a n c i n g Alpha of a portfolio is the sum of the rebalancing

Alphas of all different asset pairs. The probability that the portfolio rebalancing Alpha is positive is the product of the probabilities that the rebalancing Alphas of all asset pairs are positive. For a long-only portfolio, if the rebalancing Alphas of all asset pairs are non-negative, then the rebalancing Alpha will be non-negative. Furthermore, if at least one asset pair has a positive rebalancing Alpha, then the portfolio rebalancing Alpha will be positive. If there are asset pairs with negative rebalancing Alpha, investors can make the rebalancing Alpha in the portfolio positive by excluding these asset pairs.

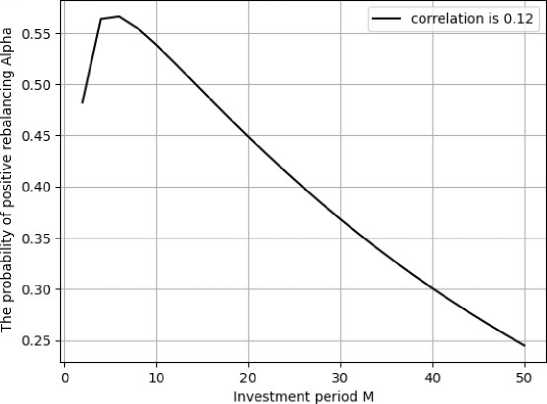

Based on the above t he or y , it can be concluded that the probability of a positive rebalancing Alpha for a l o ng -only portfolio is independent of the asset weights. For a long-only portfolio, sin ce all assets have positive weights, it is only needed to consider the non-centrality p a r ame t e r. We further constructed portfolios of equity and bills based on historical re se ar ch data. Global investors can expect an equity premium (relative to bond) of a r ou nd 5% on an arithmetic mean basis, which is similar to Siegel‘s data [5; 10]. F o ll ow i ng standard practice in finance literature, we obtain volatility and c or r e l at io n estimates from the Ibbotson SBBI database (Ibbotson & Sinquefield, 1976). For the 1926-2022 period, US equity volatility was 19.8%, longterm government bond volat i l i t y was 9.9%, and their correlation was 0.12 [6]. Based on different i nv es tm e nt periods M, we calculated the probability of a positive rebalancing Alpha. The r e s ul ts are shown in Figure 2.

The probability that the rebalancing Alpha of an Equity-Bond portfolio is positive.

Figure 2. The re l ati on s hip between the probability that the rebalancing Alpha of an Equity-Bond portfolio is positive and the investment period M

The result of Figure 2 is completely different from Figure 1. The probability of a positive rebalancing Alpha rises first, and reaches the maximum around the year of five. However, it will reduce with the growing M. When M reaches 50, the probability of a positive Alpha will be extremely less.

Conclusion

The probability of a positive rebalancing Alpha refers to the probability that a portfolio will achieve premium returns through a rebalancing strategy. A positive rebalancing Alpha is exactly what is expected, but in reality, it is a rare phenomenon. Even if it exists, its existence is short-lived. Only under strict conditions will the probability of a positive rebalancing Alpha in long-term investments not decrease. In general, a long-only portfolio achieves premium returns. It is also difficult for a long-only portfolio to achieve premium returns through rebalancing strategies. This requires investors to construct an ideal portfolio to avoid asset pairs that cannot obtain premium returns.