Assessing the factors that determine people's financial behavior: an experience of using regression analysis based on panel data

Author: Belekhova Galina V., Rossoshanskii Aleksandr I.

Journal: Economic and Social Changes: Facts, Trends, Forecast @volnc-esc-en

Section: Social development

Article in issue: 5 (59) т.11, 2018.

Free access

Financial behavior determines people’s engagement in economic life and is therefore critical to social, financial, and economic stability. Numerous studies conducted in Russia since the mid-1990s point out the existence of “system problems” in the financial behavior of the country’s population; the problems include moderate savings and investment activity, passive pension strategies, and a low level of financial literacy. The reasons for this situation lie not only in the “Soviet past”, or in the prevalence of paternalistic sentiments, or in the specifics of “national mentality” in relation to money, or in the limited amount of free cash that people have, or in the “blind spots” of financial legislation. It is necessary to understand that financial behavior is a complex socio-economic phenomenon, formed by the impact of many different factors. Therefore, it is important to study factors that influence the content of people’s financial behavior. The goal of the paper is to identify macroeconomic factors in people’s financial behavior; the factors that can be taken into account in the regulation of the financial sector and the social sphere...

Financial behavior, econometric methods, panel data, income, birth rate

Short address: https://sciup.org/147224093

IDR: 147224093 | UDC: 330.567.2:330.43 | DOI: 10.15838/esc.2018.5.59.13

Text of the scientific article Assessing the factors that determine people's financial behavior: an experience of using regression analysis based on panel data

In modern Russia the main criterion for public administration efficiency is the ability of the state to improve the citizens’ quality of life by ensuring sustainable economic growth and increasing real incomes and opportunities for their beneficial use [1; 2]. In this context it is important to address the topic under review as the financial behavior of the population not only forms a certain standard of living and contributes to household welfare, but also provides the economy with necessary funds, thereby supporting investment processes in the country. In the opposite case (systemic long-term problems in citizens’ financial actions) we have to deal with retirement of a significant share of assets, their inaccessibility to enterprises and local authorities either as investment funds or as consumer demand1.

, panel data, income, birth rate.

Issues related to the regulation of financial behavior, study of factors and motives determining its content are reflected in works by domestic and foreign researchers and various research groups. For example, since the early 2000s, VTsIOM together with ZIRCON analytical group monitors the financial behavior of Russians and some of its types (saving, credit and investment). The results of sociological research studies demonstrate that among Russians most widely use the consumer behavior model, “I spend everything I earn”, they only save in case when there are money left after consumption; every fifth considers loans as their most adequate practice2.

Similar findings are demonstrated by regional studies. The results of long-term studies of financial behavior, population’s standard of living and quality of life, conducted at the Vologda Research Center of the Russian

2 Financial behavior of Russians. Available at: rossiyan/

Academy of Sciences suggest that people’s financial behavior is concentrated on using traditional financial products (savings and loans), is associated with a low level of financial literacy, and is characterized by a permanent increase in the volume of deposits and consumer loans (in monetary terms). At the regional level, moderate saving and credit activity is marked among of the population (according to sociological studies in the Vologda Oblast3 in 2016, 23% of the population have savings and 22% – outstanding loans). People are focused on consumption to meet current needs (48% use all funds for consumer spending); a significantly smaller shareof people (39%) prefer “passive savings” where consumer needs are satisfied initially and only then the remaining funds are saved; a small share of people (13%) is focused on “priority saving” where savings are used for meeting consumer needs. For a long time (since 2001 – the first year of observations), commitment to traditional forms of saving – keeping funds in commercial banks (50%) and in cash (46%) – has prevailed; “new market” forms (securities, deposits in mutual funds, non-state pension funds, insurance policies) are less common (up to 10%). There is a focus on the “marketing” component of banks’ activities (awareness – 43% and brand loyalty – 27%) to the detriment of accounting for deposit characteristics and conditions of its provision (interest rate, ease of disposal of funds, favorability of contract terms – about 20–24%), lack of attention to security and reliability a bank in terms of deposit insurance (10%). The prevalence of “moderate” self-assessment of the level of financial literacy is marked (the share of satisfactory assessments – 35%, unsatisfactory – 55%, only 10% of people assess their skills as good and excellent); at the same time, the key issues of financial literacy for many years remain the same: lack of focus on savings, low budget discipline (most people do not keep record of their incomes and expenses), low prevalence of the practice of comparing financial services, unawareness of the deposit insurance system.

According to NAFI Research Center4, in 2017 only a bit more than one third of Russians (36%) had savings in the form of bank deposits in banks, stocks, bonds, and other securities or cash. The most common way to invest money is opening and making a deposit in SBERBANK (48% of those who have savings); the second most popular way is saving money in rubles and storing it in cash (34%). 21% of respondents have deposits in other commercial banks. Less traditional investment options are used much less often: deposits in pension funds (9%), purchase of foreign currency (8%), purchase of securities (3%), and deposits in mutual funds (3%). A new mass product proposed by the Ministry of Finance – federal loan bonds (“people’s bonds”) – is considered attractive by 17% of Russians, the rest (83%) prefer bank deposits5. The market of non-cash payments is also slowly developing – as of the beginning of 2017, the share of non-cash payments in the total volume of payments amounts only to 30%6. According to the results of other nationwide surveys, 61% of Russians make rash purchases even in situations of personal budget deficit7, % are informed about tax credits but only 10% of respondents executed them8, only 50% of respondents keep record of a family budget and 46% have long-term financial goals which they try to achieve9.

According to official statistics, when administering funds people primarily seek to meet consumer demand and various monetary liabilities to the state and creditors. Thus, for the last 10 years the main share of cash income allocated to purchasing goods and paying for services (74% in 2008, 74% – in 2012, 75% – in 2017), as well as to paying mandatory payments and contributions (12% in 2008, 11% – in 2012, 12% – in 2017)10. The share of funds saved ranges between a rather narrow interval (6–14%), while during 2015–2017 there was a significant reduction in savings – from 14 to 8%11. Such patterns in income management are manifested in a rather moderate growth in the volume of individual deposits in commercial banks compared to loans granted to the population: for example, in 2011, compared to 2010, the increase in deposits amounted to 14%, in loans – 28%, in 2017 compared to 2011 it is 5 and 10%, respectively. In other words, the predominance of consumer behavior practices including those financed by borrowed funds is obvious.

On the one hand, the current situation corresponds to the objectives of executive authorities aimed inter alia at supporting consumer demand (for example, through actions such as increasing minimum wage, wage indexation in public sector, support for the social security system, development of mechanisms for demand side financing, etc.). On the other hand, the government is also interested in “educating the domestic mass investor: since 2015, Russians can open individual investment accounts; since 2017 the Ministry of Finance issues special federal loan bonds for the population (OFZ-n), the concept of individual pension capital is being developed”12. Above all, scientific interest in the problems of financial behavior does not subside, researchers seek to find opportunities for greater involvement of the population in operations on the financial market. The research presents the results of the study of factors in population’s financial behavior conducted to identify the most significant of them. It is assumed that accounting the identified factors in public administration will increase people’s involvement in the financial sector and improve its financial situation. The research studies the existing classification of factors and justifies the author’s view on the set of factors in population’s financial behavior; regression analysis of the influence of factors is conducted with the use of panel data, which made it possible to take into account the time and spatial effects.

The research depth of the problem

In foreign science, the theoretical and methodological framework of studying people’s financial behavior was formed by the 1970s on an extensive basis of empirical research; in domestic science, the transformation processes of the early 1990s became an incentive for studying financial behavior. Two approaches to the interpretation of the considered economic category are mainly used:

-

1) financial behavior as various types of citizens’ financial activity (savings, investment activity, insurance, debt and credit behavior, money games, etc.) [3];

-

2) financial behavior as people’s activity in receiving, spending, and other use of money pursuing a variety of goals13.

The researchers agree that people’s financial behavior is determined by many factors of both objective (monetary income, trends in the development of financial institutions, money supply, inflation, exchange rate, interest rates, etc.) and subjective nature (estimates and expectations regarding the country’s economic prospects, credibility of banking institutions, desire to save/not save, learned behavior patterns, etc.) ( Tab. 1 ).

All these factors are interrelated, i.e. the influence of objective economic conditions on human behavior is inevitably mediated by their subjective views on economic processes [4]. This statement demonstrates the classification of factors in financial behavior proposed by S.J. Heckman and S.D. Hanna [5, p. 189]. The researchers rely upon the conceptual model developed by S. Beverly [6] taking into account individual and institutional factors. According to S.J. Heckman and S.D. Hanna, individual factors include: economic resources and needs, social networks, financial literacy, and psychological variables. Economic resources and needs are determined by classic economic variables – income and expenditure. Social networks refer to the extent to which financial practices are encouraged or discriminated in the society (or in the social environment where a person operates). Financial literacy reflects a person’s level of understanding financial concepts and products. Psychological variables include monetary attitudes (attitudes to money) and personality traits that can influence financial management such as person’s motivation to save up. Among institutional factors highlighted by S.J. Heckman and S.D. Hanna are: features of access, incentives, and assistance. Features of access characterize the degree to which it is convenient and easy to access financial institutions and receive necessary services or advice. Incentives are institutional factors, both financial and nonfinancial, that make financial actions more attractive. Assistance involves simplification of formalities, i.e., specially designed plans (for example, pension or mortgage) that can be used by people to significantly simplify complex financial decisions.

Some foreign studies have shown14 that the use of income as a determinant of financial decision-making is a rough approximation and the impact of income expectations needs to be further considered. In particular, it was found that household savings are influenced by the expected future income. It is also indicated that the emergence of short-term and longterm “uncertainties” associated with income,

Table 1. Classification of factors determining people’s financial behavior

The hypothesis of the life cycle of consumption and savings, which presents an original view on the combination of objective and subjective factors influencing financial (consumer and saving) behavior, has become widely spread. Its main idea is that people’s needs and incomes are not equal at different stages of a life cycle; people make choices about how much they want to spend at each stage of their life, taking the resources available as a limitation [14, p.138]. Accordingly, the hypothesis states that financial actions are influenced by the size and composition of a household; age and number of children in a family, as well as the number of working members; changes in the marital status of household members such as death of one spouse, divorce, temporary separation, and other demographic factors [14, p. 139].

At the same time, it is noted that macroeconomic demographic factors (population growth and ageing) produce long-term changes, which necessarily lead to serious transformations both in financial systems and individual attitude to personal finance [13, p. 423].

Cultural characteristics are important in shaping people’s financial behavior. The study by W. Breuer and A.J. Salzmann [15] argues that national culture is a strong indicator of the structure of household assets and thus very effectively predicts the use of certain classes of assets, but at the same time, it is less informative in case of general characteristics of people’s financial decisions.

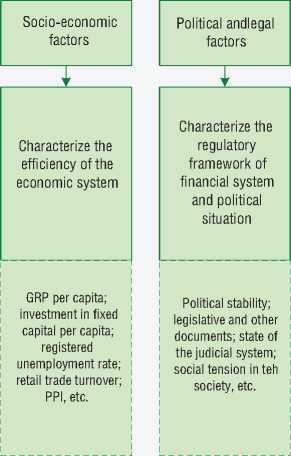

Macroeconomic factors of people’s financial behavior

|

Factors of strandard of living |

Demographic factors |

|

|

; |

||

|

Characterize people's financial status and opportunities |

Characterize the impact of biological processes and demographic behavior of the population (i.e. reflect the demographic status and its change) |

|

|

Average per capita cash income; average monthly wage; consumer expernditure per capita; living space per inhabitant, etc. |

Life expectancy at birth; total fertility rate; age structure; marriage and divirce rates; vital statistics, etc. |

|

Financial factors |

Socio-cultural factors |

|

|

; |

ф |

|

|

Characterize the development of the country's financial sector |

Characterize the impacts of historical, cultural, and national characteristics of the country, as well as social relations |

|

|

Object security (number of credit institutions per capita); interest rates; financial stability; financial depth (share of loans or deposits in GDP), etc. |

Ethnic composition; religion; mentality, etc. |

Source: compiled by the authors.

It is quite natural that the economic environment and the direct development of the financial system, along with the above factors, are also powerful sources of influence on people’s financial decisions. The variety and availability of financial products outline the possibilities of the population’s financial selfexpression. It is important at what stage of the economic cycle the country currently is. Even if other elements related to financial decisions remain constant, financial behavior would be significantly different in periods of economic growth compared to the periods of crisis or shocks [13, p. 423].

In our view, macro- and microeconomic factors of financial behavior should be distinguished. Macroeconomic factors ( Figure ) affect the entire population of the country and are affected by direct and centralized management. Microeconomic factors are manifested and influence differentially depending on the groups under consideration (population of a region/ city, household, etc.), cover objective and subjective aspects of life, are more socialized and psychologized, and, therefore, measures of indirect impact at the local level are more applicable for them.

It should be emphasized that the presented classification is not the only correct one and does not deny other approaches to identifying factors in financial behavior. Moreover, it is not excluded that the two selected groups of factors (for example, personal household income and per capita income) may overlap. In other words, the presented authors’ classification covers the most important factors identified in previous studies and corresponds to the research objectives. In particular, the selected factors will be used in regression analysis taking into account panel data, the results of which are presented in the following sections of the article.

Materials and methods

The use of panel data when constructing regression models of financial behavior in this article is explained by the specific structure of the information framework of the study which includes both time series (“time-series data”) and spatial data (“cross-section data”). The use of this type of information framework makes it possible to specify and evaluate more complex and more realistic models, as opposed to models based on only one time series or one spatial set. This is achieved through the ability, firstly, to track individual characteristics of objects over time; secondly, to use a larger number of observations, which increases the number of degrees of freedom and reduces factor multicollinearity; thirdly, to prevent aggregate shift, which inevitably occurs when analyzing only time series or only spatial samplings [16; 17].

M. Verbeek notes that an important advantage of panel data compared to univariate time series or spatial sampling is the fact that the former identify certain parameters or questions without having to make constraint assumptions [18, p. 496]. Thus, the structure of panel data helps model or explain the situation not only when the sample units behave differently, but also when the sampled situation behaves differently in different periods of time.

Regarding the individual effects of economic units, two main types of panel regression models are used: the fixed effects model and the random effects model. At the content level the difference between them can be interpreted as follows. Fixed effect models imply that each economic unit is unique and cannot be considered as a result of a random selection from a certain general population. This is true when it comes to multiple samples consisting of countries, regions, large enterprises or industries, that is, individual differences are permanent, rather than random [19]. The regression equation of the fixed effects model is as follows:

V it = P l ^ it + a i + e it , (1)

where Xit – regressor which does not contain constant term ;

ai – time-independent term expressing individual effect of i unit;

eit – standard error.

In a random effects model, on the other hand, units fall into the panel as a result of selection from a large sampling and differ in the size of random effect. A distinctive feature of the random effects panel data model compared to the fixed effects model is that the differences revealed during the construction of the model are random due to the fact that units randomly fall into the sample from the general population. For example, this is true for surveys of households, small companies, etc. [19]. The random effects model has the following form:

V it = p o + P l ^ it + u i + e it , (2)

where β 0 – constant term;

ui – random error time-invariant for each unit.

In addition to content selection of the most appropriate type of models, there is a number of standard tests to solve the problem of selection. For this purpose, a pairwise comparison of the estimated models is carried out15:

-

1. Wald test (testing the hypothesis that all individual effects equal zero) – used to compare a fixed effects model with a combined regression model that does not take into account individual characteristics of a unit.

-

2. Breusch–Pagan test (BP test) (based on the maximum likelihood method) – compares a combined regression model and a random effects models.

-

3. The Hausman test – compares random effects regression and fixed effects regression. The random effects model assumes that individual effects are not correlated with regressors. It is important to check that we fulfilled an assumption of such a correlation which invalidate most estimates of the random effects model.

Econometric models of saving and credit behavior

Regression analysis of the impact of factors in financial behavior will be performed based on the models of saving and credit behavior. The choice of these types of financial behavior is due to several circumstances. First, our studies have made it possible to establish that the higher the population’s saving and credit activity is, the better are the characteristics of the quality of life, and the higher is its integral assessment16

[20, p. 51]. Second, these types of financial behavior finance consumer demand, which helps judge the population’s standard of living and at the same time is the basis of the country’s economy17.

We chose the deposits of physical persons and loan debt provided to physical persons as dependent variables characterizing saving and credit behavior. Information on these indicators is accumulated by the Central Bank of the Russian Federation and the Federal State Statistics Service (Rosstat) for a fairly long period of time and is publicly available. The choice of the indicator “loan debt provided to physical persons” is due to the fact that it is calculated on a cumulative basis and includes both newly granted loans and payments on previously granted loans, i.e. it more accurately reflects the population’s loan liabilities compared to the indicator “loans granted”.

In this study, econometric models are constructed taking into account the structure of panel data separately for saving and credit behavior. Thus, we evaluated regression equations where the dependent variable in the first case is saving behavior, and in the second – credit behavior; we take socio-economic, demographic, political, legal, financial and socio-cultural factors and the factors in the standard of living as explanatory variables (see Figure). The information framework consists data from the Federal State Statistics Service and the Bank of Russia for 2010–2016 for 80 constituent entities of Russia. The exceptions were: the Republic of Crimea, the city of Sevastopol, Khanty-Mansiysk, Yamal-Nenets, and Nenets Autonomous okrugs due to lack of information on a number of indicators. StataMP statistics package was applied for calculations.

The list of variables analyzed in the paper for the two models is as follows. The model of saving behavior includes statistical indicators such as average per capita income (RUB); total fertility rate, number of children per 1 woman; number of credit institutions and branches (units per 100 thousand people); unemployment rate (according to the ILO methodology); consumer price index (CPI). The model of credit behavior includes: average monthly wages; life expectancy (years); demographic load factor; consumer expenditure per capita (RUB); total living space per capita (m2). It is noteworthy that other indicators previously identified as macroeconomic factors of financial behavior, no matter how they were included in the model of both saving and credit behavior, did not have a statistically significant impact on the dependent variable. Thus, these variables were not included in further analysis. At the same time, the list of indicators used as explanatory variables represents in detail the groups of factors of people’s financial behavior.

Specification of models of saving and credit behavior was carried out using three standard tests described above (Wald, Breusch–Pagan, and Hausman). To confirm the need to use the structure of panel data, we built multiple regression models that do not take into account individual characteristics – the so-called “pooled regression” models. Based on the calculations, it is the fixed effects regression model taking into account the structure of panel data that helped obtain a significant and reasonable version of simulation related

Table 2. Fixed effects regression for saving behavior and socio-economic factors

|

Logarithm of deposits of physical persons per capita (RUB) |

Estimated coefficient |

Standard deviation of estimated coefficient |

Student’s t-test |

Significance level P>|t| |

95% confidence interval |

|

|

Logarithm of population's revenues per capita, RUB |

1.18978 |

0.0426885 |

27.87 |

0.000 |

1.105899 |

1.273662 |

|

Total fertility rate, children per 1 woman |

0.2046596 |

0.0464145 |

4.41 |

0.000 |

0.1134564 |

0.2958627 |

|

Number of credit institutions and branches, units per 100 hundred people |

-0.0430529 |

0.0065526 |

-6.57 |

0.000 |

-0.0559285 |

-0.0301773 |

|

Unemployment rate (ILO methodology), % |

-0.0082325 |

0.0025476 |

-3.23 |

0.001 |

-0.0132384 |

-0.0032265 |

|

Total living space per capita, m2 |

0.0362576 |

0.0059912 |

6.05 |

0.000 |

0.024485 |

0.0480303 |

|

Constant term |

-1.902618 |

0.3343472 |

-5.69 |

0.000 |

-2.5596 |

-1.245635 |

|

sigma_u |

0.4310251 |

|||||

|

sigma_e |

0.08354147 |

|||||

|

rho |

0.096379378 |

|||||

|

F test that all u_i=0: F(79. 475) = 85.94Prob> F = 0.0000 |

||||||

|

(F(5.475) = 1440.22; Prob> F = 0.0000; R-sq: within = 0.9381; between = 0.6307; overall = 0.6671 Corr(u_i, Xb) = 0.2856) Source: authors calculations. |

||||||

Table 3. Fixed effects regression for credit behavior and socio-economic factors

-

1. Wald test . Since p-level < 0.01, the main hypothesis is rejected. This means that a fixed effects regression model better suits to describe data than a simple regression model.

-

2. Breusch–Pagan test . In this case, the value of criterion x2 = 853.04, the significance level p = 0.0000. Since p-level < 0.01, the main hypothesis is rejected. This means that a random effects model better describes data than a combined regression model.

-

3. Hausman test . Since p-level < 0.01, the main hypothesis is rejected. Thus, a fixed effects model describes data better than a random effects model.

In general, such a result is expected since the study selected Russian constituent entities whose composition has not changed during the research period.

Results and discussion

Below are the results of constructing econometric models taking into account the structure of panel data separately for saving ( Tab. 2 ) and credit behavior ( Tab. 3 ).

Factors in standard of living. A quite natural result is the identification of a significant positive correlation between financial behavior and factors in standard of living, namely between the population’s deposits and per capita cash income, between loan debt and wages, and consumer expenditure. Population’s income is treated as a budget constraint within which consumption, savings and investment is carried out. The higher the income level is, the more, with all other things being equal, opportunities there are for making savings (e.g. bank deposits). The observed correlation between loan debt and per capita consumer expenditure illustrates the important role of borrowed funds (consumer and mortgage loans, car loans) in expanding income-constrained consumption frameworks18.

Presence of credit institutions . Numerous empirical studies demonstrate that effective functioning of the financial sector has a positive impact on economic growth [21; 22; 23; 24]. At the same time, “the contribution of the financial sector to the country’s GDP primarily depends on the actions of its key actors – commercial banks”19. Initially, it is banks that produce the supply of standard financial products (deposits, loans), through which loan requests of various enterprises are financed. Banking institutions contribute to economic development as they often redirect funds from low- to high-income investments [25; 26], and the prevalence of banking institutions strengthens monetary control thus providing greater economic stability [26].

The established inverse correlation between the number of credit institutions and deposits of individuals is largely due to the growth of the latter while the financial system is being “cleaned up” by the Bank of Russia.

Inflation (consumer price index). The impact of this factor often has conflicting explanations. Some experts argue that expectations of high inflation stimulate consumption, which consequently reduces savings20. Other researchers draw attention to the fact that the level of inflation is largely determined by financial and economic decisions of the federal government, and, consequently, high inflation may indicate macroeconomic uncertainty of the country’s development21, thereby encouraging the population to be guided by caution and save money. The calculations reveal a weak feedback between inflation and loan debt. This suggests a fairly “balanced” behavior of Russians who try not to undermine their financial situation amid rising consumer prices and therefore – not to increase the debt.

The correlation between financial behavior and demographic factors is interesting. An inverse correlation between life expectancy at birth and loan debt can be interpreted in two ways. On the one hand, in regions with low life expectancy the population is more likely to live “here and now, without postponing” willingly spending money, including those borrowed. On the other hand, in regions with high loan debt, the population is forced to work more, overloading themselves physically and psychologically, which can affect the state of health and life expectancy.

The regression model reveals a positive correlation between deposits of individuals and total fertility rate. This situation can partly be explained by the fact that child births in 2010–2016 encouraged by the demographic policy (maternity fund) has led to the growth in consumption, which was provided both at the expense of previously accumulated savings and through loans. Thus, analysis demonstrates the need to identify factors affecting people’s financial behavior in order to regulate it, focusing on improving both people’s financial literacy and the standard of living.

The constructed models of saving and credit behavior in the country’s regions suggest that the citizens’ financial actions are not absolutely unpredictable, but depend on rather objective factors. By influencing all of these factors, executive bodies can promote the development sound financial behavior.

Conclusion

The study identifies macroeconomic factors that have a significant impact on people’s financial behavior. For this purpose, the authors developed and justified a system of indicators and a classification of macroeconomic factors in financial behavior. In contrast to the analyzed works of related topics, which characterize financial behavior through savings, the presented study takes into account saving and credit practices of the population, which is especially important amid current economic conditions since, along with the traditionally widespread savings, the Russians have been actively using borrowed funds to finance their consumer demand for several years. Moreover, saving and credit behavior was modeled using regression analysis through panel data, which took into account temporal and spatial data and helped construct more realistic models as opposed to models based solely on time series or spatial population.

The results show that the impact on financial behavior should be “close” to its carrier, i.e. a person, since the determining factors are demographic processes and financial status. We can identify the following targets for regulating people’s financial behavior:

– improving the legal and regulatory framework of the financial system taking into account international standards; strengthening the legal framework for the functioning of the financial sector;

– creating mechanisms to increase people’s saving motivation, which would increase the volume of organized savings and diversify financial products and services;

– implementing measures to improve financial literacy and overcome people’s distrust of financial institutions;

– implementing the demographic policy measures to support young families, multi-child families, as well as further developing the system of material incentives and support fertility.

Regulation of financial behavior should be ensured by a set of dynamic complementary interacting mechanisms, including social policy (income policy, pension reform), educational policy (financial education), demographic policy, and youth policy. The functioning of all mechanisms involved should be ensured by management entities through coordinated execution of planning, forecasting, regulatory support, monitoring and control functions.

The research results can be used by state authorities at the federal and regional level in order to elaborate regional development programs, develop measures within the framework of the social policy aimed at addressing social and economic problems of households, and determine measures to stimulate financial behavior aimed at increasing people’s involvement in saving and investment. The applied tools can be used as a methodological framework both by authorities for developing the described programs and activities and by private financial institutions in their own market research.

In conclusion it should be emphasized that the current political course aimed at addressing demographic problems, improving and developing financial system, and educating the Russian population financially, in light of the identified correlations is timely and correct. However, the concern for the most acute problems, i.e. providing sustainable growth of people’s incomes, overcoming excessive income inequality, and creating conditions for improving the financial status of the country’s population, remains the most relevant aspect.

References Assessing the factors that determine people's financial behavior: an experience of using regression analysis based on panel data

- Ilyin V.A., Povarova A.I. Problems of regional development as the reflection of the effectiveness of public administration. Ekonomika regiona=Economy of Region, 2014, no. 3 (39), pp. 48-63..

- Ilyin V.A. Shabunova A.A. Sociological assessment of public administration efficiency. Ekonomicheskie i sotsial’nye peremeny: fakty, tendentsii, prognoz=Economic and Social Changes: Facts, Trends, Forecast, 2014, no. 2(32), pp. 18-35..

- Kuzina O.E., Ibragimova D.Kh. Confidence in Financial Institutions: Experience of Empirical Study. Monitoring obshchestvennogo mneniya: ekonomicheskie i sotsial’nye peremeny=The Monitoring of Public Opinion: Economic and Social Changes Journal, 2010, no. 4(98), pp. 26-39..

- Katona G. Psychological Analysis of Economic Behaviour. New York, McGrow-Hill, 1963. 347 p.

- Heckman S.J., Hanna S.D. Individual and Institutional Factors Related to Low-Income Household Saving Behavior. Journal of Financial Counseling and Planning, 2015, vol. 26, is. 2, pp.187-199.

- Beverly S., Sherraden M., Cramer R., Shanks T., Nam Y., Zhan M. Determinants of asset holdings. In: Asset building and low-income families. Eds. S.-M. McKernan & M. Sherraden. Washington, D.C., The Urban Institute Press, 2008. Rp. 89-151.

- Kostomarova A.V. Makroekonomicheskaya rol’ sberezhenii domashnikh khozyaistv: avtoref. dis. … kand. ekon. nauk: 08.00.01 . Moscow, 2013. 28 p.

- Abbas N.Yu. Statisticheskoe issledovanie investitsionnogo potentsiala naseleniya RF: avtoref. dis. … kand. ekon. nauk: 08.00.12 . Moscow, 2011. 27 p.

- Agrba D. V. Lichnye sberezheniya kak istochnik razvitiya finansovogo rynka: avtoref. dis. … kand. ekon. nauk: 08.00.10 . Moscow, 2013. 26 p.

- Merzlyakova S.V. Regional’nye osobennosti finansovoi aktivnosti naseleniya Rossii: avtoref. dis. … kand. ekon. nauk: 08.00.05 . Moscow, 2012. 24 p.

- Strebkov D.O. Faktory i tipy sberegatel’nykh strategii naseleniya Rossii vo vtoroi polovine 1990-kh godov: avtoref. dis. … kand. ekon. nauk: 22.00.03 . Moscow, 2002. 27 p.

- Loayza N., Schmidt-Hebbel K., Serven L. What Drives Private Saving around the World? World Bank. Policy Research Working Paper No. 2309. Washington, D.C. 2000. Available at: https://openknowledge.worldbank. org/handle/10986/18854.

- Ciumara T. Factors Influencing Individual Financial Decisions: a Literature Review. Conference: Globalization, Intercultural Dialogue and National Identity -GIDNI, At Targu Mures, 2014, vol. 1, pp. 421-428.

- Belekhova G.V., Gordievskaya A.N. Population’s financial behavior: demographic features. Problemy razvitiya territorii=Problems of Territory’s Development, 2018, no. 1, pp. 133-150..

- Breuer W., Salzmann A. National Culture and Household Finance. Global Economy and Finance Journal, 2012, vol. 5, no. 1, pp. 37-52.

- Ratnikova T.A. Introduction to econometric analysis of panel data. Ekonomicheskii zhurnal VShE=The Higher School of Economics Economic Journal, 2006, no. 2, pp. 267-316..

- Wooldridge J.M. Econometric analysis of cross section and panel data. Cambrige. MIT Press. 2007, 776 p.

- Verbeek M. Putevoditel’ po sovremennoi ekonometrike . Translated from English. Moscow: Nauchnaya kniga, 2008. 616 p.

- Molchanova E.V. Zdorov’e naseleniya kak bazovoe uslovie sotsial’no-ekonomicheskogo razvitiya obshchestva: dis. … dokt. ekon. nauk: 08.00.05 . Moscow, 2014. 338 p.

- Belekhova G.V. Population’s financial behavior and its role in shaping the quality of life. Material from the 8th Urals Demographic Forum "Demographic potential of EAEC countries". Vol. 2. Ekaterinburg: Institut ekonomiki UrO RAN, 2017. Pp. 48-53..

- King R.G., Levine R. Finance and growth: Schumpeter might be right. The Quarterly Journal of Economics, 1993, no. 108(3), pp. 717-737.

- McKinnon R. Money and Capital in Economic Development. Washington, D.C.: Brookings Institution Press, 2010. 184 p.

- Beck T., Levine R., Loayza N. Finance and the sources of growth. Journal of Financial Economics, 2000, no. 58, pp. 261-300.

- Bangake C., Eggoh J. Further Evidence on Finance-Growth Causality: A Panel Data Analysis. Economic Systems, 2011, no. 35(2), pp. 176-188.

- Galbis V. Financial Intermediation and Economic Growth in Less-Developed Countries: A Theoretical Approach. Journal of Development Studies, 1977, vol. 13, pp. 58-72.

- Porter R.C. The Promotion of the «Banking Habit» and Economic Development. Journal of Development Studies, 1966, vol. 2, pp. 346-366.