Corporate social responsibility: assessment methods and the regional dimension

Author: Kopytova Ekaterina Dmitrievna

Journal: Economic and Social Changes: Facts, Trends, Forecast @volnc-esc-en

Section: Young researchers

Article in issue: 1 (49) т.10, 2017.

Free access

In order to implement all the delegated powers amid lack of economic and financial opportunities, it is necessary for the authorities to search for additional sources of development. One of the key economic actors is represented by business structures which possess a significant amount of financial, investment, labor and other resources. In this regard, it is relevant to develop mutually beneficial cooperation of authorities and business entities. An efficient form of such cooperation, as evidenced by world experience, is social responsibility. However, this practice is not widespread in Russia; Russian research do not pay enough attention to specific tools contributing to enhancing the role of businesses in addressing social and economic issues of territories. The present paper identifies current approaches to the understanding of social responsibility of business and presents the author's interpretation of this economic category. Based on the developed methodological tools, the author makes an appraisal of social responsibility of major chemical enterprises of the Northwestern Federal district...

Corporate social responsibility, interaction, authorities, regional development, appraisal

Short address: https://sciup.org/147223910

IDR: 147223910 | UDC: 330.341 | DOI: 10.15838/esc.2017.1.49.14

Text of the scientific article Corporate social responsibility: assessment methods and the regional dimension

The current stage of socio-economic development of Russia and its regions is characterized by lack of budget resources for financing both strategic and current issues. The situation is exacerbated by the introduction of political and economic sanctions against Russia, considerable fluctuations in oil prices and ruble exchange rate, the increasing business distrust of the authorities accompanied by an increase in capital outflows. These circumstances make it necessary to search for ways of addressing the socio-economic issues.

It is now becoming obvious that high and sustainable rates of territory’s development are impossible without committed partnership of public authorities and business representatives. Studies by leading foreign and domestic scientists (J. Banon, J. Galbraith, K. McConnell, W. Eucken, M. Porter, O. Williamson, F. Hayek, M.A. Gusakov, V.V. Okrepilov, V.S. Selin, A.I. Tatarkin, T.V. Uskova, etc.) proved the importance of private sector resources in ensuring socio-economic development of regions.

The authorities also have resources (economic, administrative, political, informational), the access to which may be useful and beneficial to businesses possessing financial, expert, innovation and management resources [15, 19]. Therefore, in order to attract business entities to the solution of issues of socio-economic development of territories it is necessary to coordinate the interests and find mutually beneficial forms of cooperation.

One of the most promising forms of interaction between authorities and business which would effectively solve socio-economic problems of territory’s development is corporate social responsibility (CSR). However, in the Russian business environment, the understanding of this category is only beginning to emerge; the related research pay insufficient attention to the study of specific forms, methods and tools contributing to enhancing the role of economic entities in regional development.

Despite the increase in the number of CSR studies, the number of definitions of this economic category is quite large. In Russia, the most common definition is given by Managers Association and states that corporate social responsibility is a voluntary contribution of business to the development of economic, social and environmental spheres. A similar definition is given by Bank for Development (Vnesheconombank): corporate social responsibility is a voluntary contribution of enterprises to the development of the society in economic, social and environmental spheres, which is mainly implemented on a supplemental basis with reference to legal requirements. The fund “Institute for Urban Economics” defines it as a comprehensive responsibility of a citizen, employer, business partner, actor of social relations.

Different interpretations of corporate social responsibility in western countries have existed for a long time (Tab. 1). The traditional approach is known as a theory of corporate selfinterest characterized by denial of social responsibility of business structures because the main purpose of their activity is to gain maximum profits. The essence of the theory of corporate altruism, which was formulated by the US Committee for Economic Development, consists of recommendations to business entities to contribute to the solution of socio-economic problems of territories. The following interpretation of the concept encompasses voluntary social businesses program designed both to support certain population groups and gain tax benefits and public recognition. The awareness of economic entities of benefits from charity programs has led to the emergence of an integrated approach to corporate social responsibility, where business structures derive their own benefits.

There is a different point of view regarding the essence of corporate social responsibility ( Tab. 2 ). It is necessary to note the similarity between the integrated and strategic approaches. The strategic approach to the

Table 1. Interpretation of corporate social responsibility

|

Theory |

Interpretation |

|

The theory of corporate selfinterest (traditional approach) |

The distinctive feature of the theory lies in the fact that the only purpose of social responsibility is increase in shareholders’ earnings within the law; the main objective of the government is to address public issues (M. Friedman The Social Responsibility of Business is to Increase its Profits, 1971). |

|

The theory of corporate altruism |

The essence of the theory is that business entities must maximize and gain profit, as well as contribute to addressing the issues of the population, environment, etc. US Committee for Economic Development). |

|

Theory of enlightened selfinterest |

The essence is that costs of social programs, charity, and sponsorship contribute to favorable environment, reduction in enterprise tax base under statutory legislation. |

|

Integrated approach |

The feature of the approach is business participation in socially significant projects in specific spheres, which results in reduced inconsistencies in the interests of businesses and population. |

|

Source: compiled from [2, 17, 21, 22]. |

|

Table 2. Approaches to the content of corporate social responsibility [2, 20, 23]

In the author’s view, it is the strategic approach which is associated with successful international experience, as it is aimed at the development of both the enterprise itself, and its area of presence. Accordance to this approach, the author identifies two interpretations of CSR. In a narrow sense it is understood as regulation of social and labor relations in a company, in a broad sense – implementation of enterprise programs within their area of presence.

Taking into account the identified peculiarities, the author defines corporate social responsibility as business participation in solving socio-economic problems of its area of presence beyond legislative regulations in order to improve the quality of life of both their employees and the population of the region.

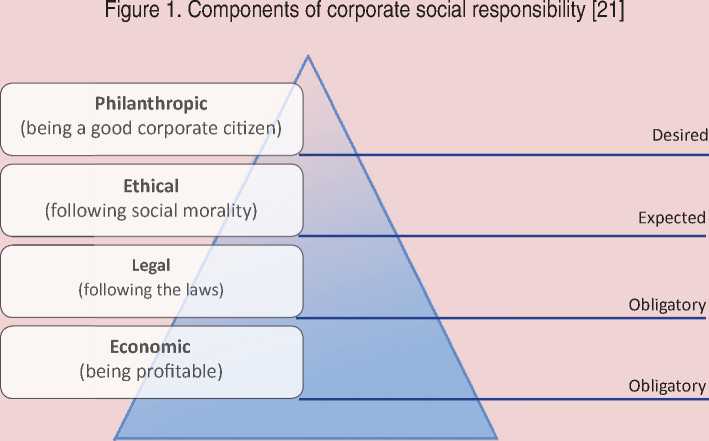

Levels of CSR were presented in the form of a pyramid by a foreign scientist A. Karroll [21] back in the 1970–s ( Fig. 1 ). The base of the pyramid is economic responsibility because this is the basic function of a business entity in the market as a producer of goods and services allowing gaining profit. Legal responsibility means the necessity to observe legislative regulations in market economy. Ethical responsibility means meeting the expectations of the society from business entities, which are not fixed in legal documents but are based on existing norms of morality and ethics. Philanthropic responsibility, in turn, involves actions of

business entities aimed at maintaining and developing the welfare of the society through voluntary participation in the implementation of social programs.

The issue of social responsibility is becoming more relevant for Russian businesses because enterprises as the most important actors of economic relations influence the socio-economic processes in modern society. In addition, there is a general deterioration of the socio-economic situation in the country. Thus, the average annual GDP growth in 2009–2014 compared to 2004– 2008 was markedly reduced (1.1% against 7.1 % respectively). Industrial production growth during 2009–2014 amounted to 1.4% against 5.4% in 2004–2008. A significant decline in indicators such as investment in fixed assets (1.2% and 15.6%), retail turnover

(3.5% and 14.0%), profit (7.0% and 28.0%), consolidated budget revenues (3.3 % against 23.0 %) was recorded [13]. The study of annual trends of main macro-economic indicators reveals a slowdown in economic development, which has a negative impact on the social sector: growth rate of the population’s real cash incomes in 2009–2014 amounted to only 2.7% (for comparison: in 2004–2008- 10.2%).

Judging by analysis results, over the past years average annual growth rates of main socio-economic indicators of the regions of the Northwestern Federal district (NWFD) have been declining ( Tab. 3 ).

A significant decline in the GRP growth in 2008–2015 compared to 2000–2007 is observed in the Republic of Karelia (5.0% against -1.1%), the Murmansk (1.7% against

Table 3. Annual average growth rates of main socio-economic indicators of NWFD regions in 2000–2015, % (in comparable prices of 2015)

|

NWFD regions |

GRP* |

Industrial output |

Agricultural output |

Investment in fixed assets |

Volume of construction works |

Per capita income |

||||||

|

2 |

3 |

2 |

3 |

2 |

3 |

2 |

3 |

2 |

3 |

2 |

3 |

|

|

NWFD |

107.5 |

101.6 |

108.8 |

104.4 |

98.7 |

103.9 |

118.0 |

97.9 |

116.5 |

106.8 |

112.9 |

102.7 |

|

Republic of Karelia |

105.0 |

98.9 |

142.5 |

115.4 |

98.1 |

99.4 |

107.4 |

98.3 |

113.2 |

103.7 |

108.1 |

101.7 |

|

Komi Republic |

103.6 |

100.5 |

104.1 |

102.6 |

97.4 |

101.6 |

107.5 |

105.0 |

115.9 |

108.4 |

109.5 |

99.4 |

|

Arkhangelsk Oblast |

109.2 |

101.1 |

112.9 |

103.7 |

93.1 |

98.0 |

126.5 |

93.1 |

114.9 |

103.9 |

110.9 |

104.0 |

|

Vologda Oblast |

104.7 |

99.3 |

104.4 |

102.9 |

97.6 |

98.8 |

125.5 |

92.7 |

118.1 |

105.9 |

111.4 |

102.2 |

|

Kaliningrad Oblast |

110.3 |

102.0 |

120.0 |

108.9 |

99.5 |

107.2 |

119.9 |

94.9 |

117.3 |

105.9 |

114.4 |

102.2 |

|

Leningrad Oblast |

110.6 |

102.9 |

113.7 |

105.5 |

101.5 |

104.2 |

114.4 |

97.1 |

117.5 |

107.9 |

116.7 |

101.2 |

|

Murmansk Oblast |

101.7 |

99.0 |

100.9 |

104.7 |

98.4 |

92.4 |

108.8 |

104.3 |

116.8 |

107.5 |

105.6 |

100.6 |

|

Novgorod Oblast |

104.7 |

103.6 |

106.1 |

105.6 |

99.5 |

110.7 |

113.6 |

106.6 |

115.0 |

110.9 |

108.6 |

105.3 |

|

Pskov Oblast |

103.6 |

100.7 |

104.7 |

105.2 |

95.2 |

107.7 |

114.0 |

97.6 |

117.2 |

108.3 |

111.6 |

103.1 |

|

Saint-Petersburg |

109.6 |

103.1 |

110.4 |

104.9 |

0.0 |

0.0 |

121.7 |

97.8 |

116.1 |

106.6 |

114.5 |

103.1 |

* For 2015, estimated data were used. Source: compiled by the author.

-1.0%) and Vologda (4.7% against -0.7%) oblasts. Industrial production during this period was been stable but the pre-crisis level is still impossible to reach. In addition, low investment in all regions of the Northwestern Federal district, excluding the Komi Republic and the Murmansk and Novgorod oblasts. It is becoming a threat to stable development of the social sphere: the growth rate of the population’s per capita cash income in 2008– 2015 is much lower than in 2000–2007.

The situation is exacerbated by lack of budget funds of local authorities. Analysis has showed that the budgetary system of NWFD regions is characterized by the increasing budget deficit and budget expenditures, a multiple increase in government debt (Tab. 4). Its volume in a number of regions exceeds 80–100% of tax and non-tax revenues [12].

It is beyond argument socially responsible business behavior is based on dynamic, successful production and economic activity of a specific economic actor the positive effect of which is an increase in the number of new jobs, as well as in the mass of commodities, tax revenues to budgets of all levels and therefore, a possibility of implementing additional social programs. All this ultimately provides a high and sustainable rate of regional economic growth.

Table 4. Main indicators of consolidated budgets of NWFD regions, billion rubles

|

NWFD regions |

Tax and non-tax revenues |

Budget deficit |

Budget expenses |

Government debt |

||||

|

2008 |

2015 |

2008 |

2015 |

2008 |

2015 |

2008 |

2015 |

|

|

NWFD |

571.6 |

894.6 |

21.0 |

16.0 |

766.9 |

1035.6 |

31.5 |

222.0 |

|

Republic of Karelia |

17.8 |

24.3 |

0.4 |

3.8 |

29.4 |

38.6 |

4.1 |

21.3 |

|

Komi Republic |

38.4 |

60.8 |

0.4 |

8.7 |

46.8 |

76.1 |

3.2 |

33.8 |

|

Arkhangelsk Oblast |

35.6 |

59.3 |

4.3 |

2.8 |

58.9 |

81.2 |

5.4 |

37.5 |

|

Vologda Oblast |

45.8 |

47.3 |

-0.3 |

2.0 |

52.8 |

60.0 |

1.8 |

34.3 |

|

Kaliningrad Oblast |

24.3 |

39.5 |

-0.8 |

11.1 |

38.1 |

70.2 |

7.5 |

20.4 |

|

Leningrad Oblast |

51.6 |

120.9 |

-1.1 |

-11.7 |

65.6 |

120.8 |

5.4 |

9.6 |

|

Murmansk Oblast |

33.7 |

59.5 |

0.3 |

1.5 |

49.8 |

68.0 |

0.8 |

20.7 |

|

Novgorod Oblast |

16.1 |

24.7 |

1.1 |

1.3 |

24.1 |

31.3 |

2.8 |

15.4 |

|

Pskov Oblast |

11.5 |

17.4 |

-0.5 |

2.1 |

18.7 |

29.0 |

0.2 |

13.3 |

|

Saint-Petersburg |

290.6 |

423.3 |

16.7 |

-7.7 |

372.5 |

439.7 |

0.3 |

14.7 |

Compiled from: [3, 12].

In this context, evaluation of the role of enterprises in the socio-economic development of territories is becoming more relevant. Russian scientists are currently working on the development of methodological tools for such evaluation. However, a unified approach to the solution of this problem has not yet been developed. This is explained by significant difficulties in obtaining reliable information about real volumes and sources of resource consumption in the business sector for financing of various activities.

Thus, some researchers [2] suggest measuring the level of social responsibility through corporate social reporting. However, they are not obliged by the law to do so,, which makes it impossible to use such techniques in the regions. Other scientists [11] determine the level of CSR on the basis of questionnaire surveys of heads of enterprises; however, it only helps estimate the level of social investment. It works of some researchers [1], this indicator is revealed only at the level of an individual enterprise through socio-labor relations, which implies access to consolidated statements, which is difficult amid current market conditions.

In the author’s view, the most appropriate method for improving the reliability of estimates of the contribution of economic entities in the regional socio-economic development is the method developed by researchers of Kemerovo State University [11]. It has been improved in terms of calculation of indicators of influence of business entities on economic growth, improvement of environmental situation, population’s quality of life and standard of living. Since these indicators characterize the enterprise activity in certain spheres, the author has calculated the integral index

– Index of influence of company’s activities on the region‘s development (IIcD) using the geometric mean value:

I IcD = VI IcG X I lli X l ie

The Index of influence of enterprise activity on the region’s economic growth (IIcG) is determined by multiplying the Index of growth of gross value added and Index of increase tax payments to regional and local budgets during the period under review compared to the reference period. The index of influence of enterprise activity on the level and quality of life and standard of living in the region (IIll) is determined by multiplying the Index of increase in average wages of company’s employees and the Index of increase in the number of company’s employees. The Index the influence of enterprise activity on the environment in the region (IIe) is determined by multiplying the Index of reduction in hazardous substances emissions into water bodies and the Index of reduction in hazardous substances atmospheric emissions [14, 17].

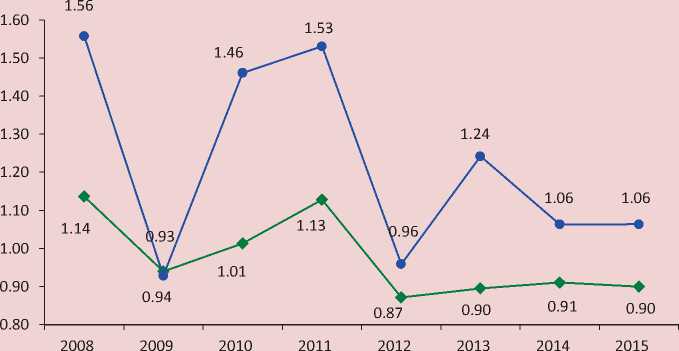

The author evaluates the impact of enterprise activities on the regional development on the example of major chemical enterprises of the Northwestern Federal district – Akron and FosAgro JSCs, which are world leaders in the market of mineral fertilizers. Their main activity is production and sales of phosphorous, nitrogen and potassium fertilizers, fluorides and other chemical products. According to estimations, the contribution of these enterprises to the development of the region has decreased ( Fig. 2 ).

Figure 2. Index of influence of company’s activities on regional development

— ♦ — Akron —•— FosAgro

Source: calculated by the author on the basis of annual reports of FosAgro and Akron JSCs.

The reduction in Index of influence of FosAgro JSC activity on regional development in 2015, compared to 2008 is explained by the reduction in gross value added, average wages and the average number of employees ( Tab. 5 ).

As for Akron JSC, a similar situation is observed: in 2008, the integral index amounted to 1.14 against 0.9 in 2015. This is caused by instable world market of chemical products and increase in their cost, which led to a decline in the enterprise’s net profit, and as a result, reducing its impact on the economic growth of the region ( Tab. 6 ).

The presented data indicate that local authorities fail to efficiently organize their interaction with business units on meeting the challenges of the socio-economic development of territories. This is confirmed by the results of the annual questionnaire survey conducted by ISEDT RAS among enterprise managers with the author’s direct participation [4]. In 2014–2015, none of the respondents gave 10 points for the level of cooperation with the government in solving regional problems ( Fig. 3 ). However, 2% of respondents awarded this interaction 9 points; 37% noted that the level of relations deserves

Table 5. Calculation of Index of influence of FosAgro JSC activity on regional development

|

Criterion |

2008 |

2009 |

2011 |

2013 |

2014 |

2015 |

Change in 2008– 2015, +/- |

|

1. Index of influence of enterprise activity on the region’s economic growth (IIcG) |

3.10 |

0.60 |

2.98 |

1.18 |

1.20 |

1.31 |

-1.79 |

|

Index of growth of gross value added |

3.74 |

0.74 |

2.37 |

0.98 |

1.30 |

1.30 |

-2.44 |

|

Index of increase tax payments to regional and local budgets |

0.83 |

0.81 |

1.25 |

1.20 |

0.92 |

1.01 |

0.18 |

|

2. Index of influence of enterprise activity on the level and quality of life and standard of living in the region (IIll) |

1.22 |

1.12 |

1.09 |

1.83 |

0.91 |

0.96 |

-0.26 |

|

Index of increase in average wages of company’s employees |

1.19 |

1.15 |

1.08 |

1.11 |

1.05 |

1.05 |

-0.14 |

|

Index of increase in the number of company’s employees |

1.03 |

0.97 |

1.01 |

1.64 |

0.87 |

0.91 |

-0.12 |

|

3. Index the influence of enterprise activity on the environment in the region (IIe) |

0.99 |

1.18 |

1.10 |

0.89 |

1.10 |

0.96 |

-0.03 |

|

Index of reduction in hazardous substances atmospheric emissions |

0.90 |

1.07 |

0.99 |

0.89 |

1.09 |

0.95 |

0.05 |

|

Index of reduction in hazardous substances emissions into water bodies |

1.10 |

1.11 |

1.11 |

1.01 |

1.01 |

1.01 |

-0.09 |

|

Index of influence of socially responsible activity of a separate corporation on regional; development (IIcd.) |

1.56 |

0.93 |

1.53 |

1.24 |

1.06 |

1.06 |

-0.5 |

|

Sources: calculated by the author on the basis of FosAgro JSC annual reports. |

|||||||

Table 6. Calculation of the Index of influence of Akron JSC activity on regional development

|

Criterion |

2008 |

2009 |

2011 |

2013 |

2014 |

2015 |

Change in 2008– 2015, +/- |

|

1. Index of influence of enterprise activity on the region’s economic growth (IIcG) |

1.51 |

1.12 |

1.41 |

0.70 |

1.08 |

1.15 |

-0.36 |

|

Index of growth of gross value added |

1.22 |

0.98 |

1.01 |

0.93 |

1.18 |

1.28 |

0.06 |

|

Index of increase tax payments to regional and local budgets |

1.24 |

1.15 |

1.39 |

0.76 |

0.91 |

0.91 |

-0.33 |

|

2. Index of influence of enterprise activity on the level and quality of life and standard of living in the region (IIll) |

0.99 |

1.03 |

1.14 |

1.09 |

0.62 |

0.81 |

-0.18 |

|

Index of increase in average wages of company’s employees |

0.96 |

1.01 |

1.11 |

1.01 |

0.84 |

0.80 |

-0.16 |

|

Index of increase in the number of company’s employees |

1.02 |

1.02 |

1.02 |

1.05 |

0.73 |

1.01 |

-0.01 |

|

3. Index the influence of enterprise activity on the environment in the region (IIe) |

0.99 |

0.72 |

0.89 |

0.94 |

1.11 |

0.79 |

-0.2 |

|

Index of reduction in hazardous substances atmospheric emissions |

1.05 |

0.90 |

0.95 |

0.99 |

1.02 |

0.85 |

-0.2 |

|

Index of reduction in hazardous substances emissions into water bodies |

0.95 |

0.80 |

0.95 |

0.95 |

1.10 |

0.93 |

-0.02 |

|

Index of influence of socially responsible activity of a separate corporation on regional; development (IIcd.) |

1.14 |

0.94 |

1.13 |

0.90 |

0.91 |

0.90 |

-0.24 |

|

Sources: calculated by the author on the basis of Akron JSC annual reports.. |

|||||||

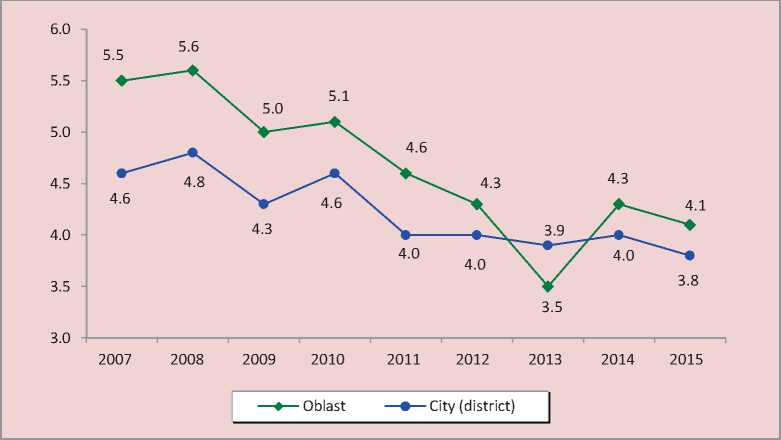

Figure 3. Level of government and business interaction in addressing socioeconomic issues in the Vologda Oblast, points (top – 10)

5–8 points, and 25% – 4 points. 37% of respondents gave not more than 3 points. The average score is 4.1 points. The interaction between executive authorities of cities and districts of the Vologda Oblast and business is assessed somewhat lower – 4 points on average. The share managers who believe that this interaction deserves the highest ranking of 8 points and above is 7%, from 6 to 7 points – 10%, no more than 5 points – 84%.

The revealed low performance of business and government interaction in resolving socio-economic problems of the territory indicated the importance of this issue for the regional economic policy.

However, according to the survey, heads of economic entities expect from the authorities more proactive measures in improving relations with them. In particular, the majority of respondents (58.8%) are in favor of strengthening economic policy by mainly using indirect measures of economic regulation. Moreover, the proportion of those who believe the state must not interfere with the country’s economic sphere decreased by 11.2 percentage points (p.p.) (Tab. 7).

At the same time, according to the respondents, the leading role in solving social problems of territories must belong to local authorities (80%), federal and regional authorities (73%; Tab. 8 ). Only 12% of managers believe that the solution to social problems must be dealt with by small and medium businesses.

Table 7. Distribution of answers to the question: “What role should the government play in the Russian economy in the next few years?”, % of the total number of respondents

|

Assessment |

2007 |

2008 |

2009 |

2010 |

2012 |

2014 |

2015 |

Change 2015 to 2007, p. p. |

|

The government should activate economic policy, expanding the scope of tools it uses, including in terms of engagement of business entities in addressing territory’s problems |

43.6 |

44.6 |

50 |

41.2 |

65.9 |

45.5 |

58.8 |

+15.2 |

|

The government must maintain certain influence on the country’s economic sphere, however, it’s role should be decreased. |

16.4 |

17.9 |

17.2 |

20 |

18.7 |

34.8 |

23.5 |

+16.4 |

|

The government must increase the degree of direct participation in the economic activity by interfering with the economic policy, хозяйственную and developing corporate social responsibility. |

16.4 |

26.8 |

15.6 |

17.6 |

7.7 |

6.1 |

8.8 |

-7.6 |

|

The current degree of government participation in the country’s economic activities is optimal. |

3.6 |

8.9 |

6.3 |

5.9 |

3.3 |

0.0 |

7.4 |

-3.8 |

|

The government must not directly interfere with the economic sphere and only monitor the implementation of laws by all business entities |

12.7 |

1.8 |

7.8 |

9.4 |

4.4 |

13.6 |

1.5 |

-11.2 |

|

Compiled from: [4]. |

||||||||

Table 8. Distribution of answers to the question: “Who should address the social problems territories?”, % of the total number of enterprise managers

|

Actors |

% |

|

Bodies of local self-governance |

80 |

|

Federal and regional authorities |

73 |

|

Citizens |

30 |

|

Large business |

29 |

|

Small and medium business |

12 |

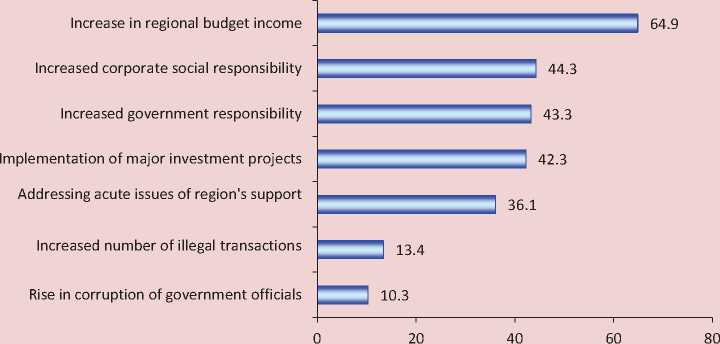

Fig. 4. Distribution of answers to the question: “What effect, in your opinion, can be expected from the interaction of government and business i n the form of social responsibility?”, % of the total number of enterprise managers

The result of productive policies of regulatory and administrative authorities in attracting businesses to the solution of regional problems is a positive effect on the socio-economic development of the region in the form of increased revenues, implementation of investment projects, etc. ( Fig. 4 ).

Taking part in the solution of territory’s problems, businesses gain additional advantages: in particular, goodwill (64.3% of enterprise managers of the Vologda Oblast); increase in public confidence in the company’s activities and expanded clientele (47,6%); retention of human capacity (47.6%) and partnership relations with authorities

Table 9. Basic areas of social responsibility of Vologda enterprises in 2015, % of respondents

|

Area |

Sjare |

|

Staff development and support |

85 |

|

Health protection and occupational safety |

62 |

|

Development of fair business practice between company’s suppliers, business partners, and customers |

41 |

|

Resource saving |

29 |

|

Participation in municipal projects implemented by the Vologda city Administration based on principles of social partnership |

26 |

|

Environmentalism |

12 |

|

Development of local community |

11 |

Table 10. Sufficiency of information about enterprise social behavior in Vologda in the media, % of respondents

However, the majority of representatives of business entities currently understand social responsibility in a narrow sense, directing a significant share of resources to staff development and support. This is evidenced by the results of a questionnaire survey of business leaders in Vologda conducted by ISEDT RAS in 2015 ( Tab. 9 ).

More than 70% of Vologda enterprise leaders believe that business needs to comply with basic social regulations, i.e., guarantee fair declared wages (76%) and provide safe working conditions and social protection of employees (70%). According to almost half of the leaders, they are required to comply with liabilities to business partners (42%) and customers, ensure production of quality products (54%). As suggested by a quarter of respondents, participation in the development of area of presence may be limited only to tax payment.

According to the respondents, among factors constraining the development of social responsibility are lack of finance for the implementation of social programs (62%), weak government stimulation of these processes (51%) and underdevelopment of the legislative framework (37%). Part of respondents (23%) indicate low information awareness about possible participation in social projects, 14% note lack of knowledge and experience in such participation.

One of the main problems of development of interaction with the authorities is lack of media coverage of enterprises’ social behavior ( Tab. 10 ).

The results of the survey of enterprise managers demonstrate that their participation in the socio-economic development of the territory depends on the government initiative to a certain extent. Therefore, in the author’s view, regional authorities need to create favorable conditions to attract businesses to the solution of territorial problems.

In the author’s opinion, this will contribute to the creation of a special coordinating body for the development of social responsibility of economic entities and their interaction with the authorities. Successful experience of creating such an organization exists in the Belgorod Oblast. In particular, the author refers to activities of Agency for Project Management (project office), under Department for Internal and Personnel Policy. The Agency carries out development and implementation of projects aimed at achieving the goals set by the Strategy of socio-economic development of the Belgorod Oblast. All projects are recorded in the shared electronic document system database “E-government of the Belgorod Oblast” which employs all executive authorities at both regional and municipal levels. As of 2015, the database has 2.300 projects, 850 of which are currently being implemented, 950 – complete [7].

According to data presented at the official website of the Department for Internal and Personnel Policy of the Belgorod Oblast, the implementation of these measures has helped ensure the effect for the socio-economic development of the territory, which consists, in particular, in the reduced period of project development and coordination (the average time savings is not less than 2 months), increased pace of investment assimilation in the region (on average by 23%), increased GRP growth (in 2011–2015, GRP growth amounted to 0.1%, or more than 3 billion rubles) [13].

Vologda also has experience in implementing joint business and government projects. The system of development, implementation and promotion of projects developed in the city Administration operates under the brand “Vologda – city of good causes”. During 2010–2015, the number of projects increased from 5 to 70, i.e., 14 times; the number of organizations participating in the projects increased 30 times. At the same time, it is clear that creation of legal and institutional conditions will lead to more active participation of business entities in solving problems of territorial development.

In addition, it is advisable for the government to stimulate these processes by providing incentives . In this context, experience of Vologda in leasing of land plots owned by municipalities on preferential terms will be useful (Resolution of the Vologda city Administration no. 6506 “List of assets owned by the city of Vologda”, dated November 30th, 2010 for leasing to small and medium business”), as well as in using tax exemptions (according to “Regulations on land tax” no. 309, dated October 6th, 2005, basic organizations of state professional educational organizations receive a 30% discount).

In the author’s view, the practice of incentives should be extended to business entities which are involved in the region’s development and engaged in partnership with the authorities.

Intangible incentives will also promoting socially responsible behavior of business entities. The author proposes activities such as organizing and conducting educational activities, informational support in the local media, social projects exhibition-fairs.

Lack of relevant knowledge and experience in compliance with principles of social responsibility may be resolved organizing and implementing training programs and developing scientific guidance manuals in social report preparation. It is worth noting that a unified form of social responsibility reporting has not yet been developed. That is why reporting of economic entities does not contain quantitative information about the ongoing projects and funds invested in the development of staff and area of presence. However, social reports contribute to creation of favorable social environment in the regions of enterprise’s activity insuring its positive image and public confidence, as well as loyalty to the enterprise. Along with this, there are social issues and risks of enterprise investments in the development of the region.

In global practice there are standards of Global Reporting Initiative (GRI) revealing the basic principles and rules of implementing such documents. In Russia there are also recommendations of this kind. In particular, the Chamber of Commerce and Industry of the Russian Federation developed a document “Social reporting of enterprises and organizations registered in the Russian Federation. Methodological recommendations”, the Russian Union of Industrialists and Entrepreneurs developed “Basic performance indicators”.

Based on analysis of recommendations on non-financial reporting, the author believes that the system of indicators adapted to the Russian accounting system and legislation should reflect the economic, social and environmental aspects of enterprise activities and the structure of corporate social responsibility report must include the following sections: organizational-economic, social, technological, environmental, nonproduction.

The introduction of the report should describe the priorities and principles of the company’s social policy; each section is required to outline the achieved results, the development areas of particular processes, future social projects and the expected results of their implementation.

To sum up, amid current conditions of lack of budget resources, the authorities need to attract additional sources of funding. In this situation, these are resources of businesses, which provide the possibility of investing extra-budgetary funds in the development of public infrastructure, addressing specific socio-economic objectives, expanding the range and improving the quality of services, developing new growth areas, and raising the level of the region’s socio-economic development [16]. However, in order to attract such resources, regulatory and administrative authorities need to strengthen their positions regarding the use of techniques aimed at increasing participation of business entities in the socioeconomic development of territories.

References Corporate social responsibility: assessment methods and the regional dimension

- Andreeva E.L. Mekhanizmy otsenki vliyaniya sotsial'noi otvetstvennosti biznesa na ustoichivoe razvitie regionov . Ekaterinburg: Institut ekonomiki UrO RAN, 2010, 43 p..

- Belyaeva Zh.S. Modeli sotsial'no otvetstvennogo biznesa v mirovoi ekonomike: monografiya . Ekaterinburg: In-t ekonomiki UrO RAN, 2010..

- Ilyin V.A., Povarova A.I. Problemy effektivnosti gosudarstvennogo upravleniya. Tendentsii rynochnykh transformatsii. Krizis byudzhetnoi sistemy. Rol' chastnogo kapitala. Strategiya-2020: problemy realizatsii: monografiya . Vologda: ISERT RAN, 2014, 188 p..

- Lukin E.V., Mel'nikov A.E. Monitoring funktsionirovaniya i razvitiya promyshlennosti regiona: zaklyuchitel'nyi otchet o NIR . Vologda, 2015, 82 p..

- Ofitsial'nyi sait AO «Akron» . Available at: http://www.acron.ru/..

- Ofitsial'nyi sait AO «FosAgro» . Available at: http://www.phosagro.ru/..

- Ofitsial'nyi sait Departamenta vnutrennei i kadrovoi politiki Belgorodskoi oblasti . Available at: http://www.dkp31.ru/project..

- Ofitsial'nyi sait Federal'noi nalogovoi sluzhby . Available at: http://www.nalog.ru/rn35/..

- Ofitsial'nyi sait Federal'noi sluzhby gosudarstvennoi statistiki . Available at: http://www.gks.ru/..

- Peregudov S.P. Biznes i byurokratiya v Rossii: dinamika vzaimodeistviya . Politologiya , 2007, no. 1, pp. 47-63..

- Perekrestov D.G., Povarich I.P., Shabaev V.A. Korporativnaya sotsial'naya otvetstvennost': voprosy teorii i praktiki: monografiya . Moscow: Akademiya Estestvoznaniya, 2011, 216 p..

- Pechenskaya M.A., Povarova A.I., under scientific supervision of Doctor of Economics, Professor V.A. Ilyin Regional'nye byudzhety: tendentsii, sostoyanie, perspektivy: monografiya . Vologda: ISERT RAN, 2016, 110 p..

- Praktika organizatsii proektnoi deyatel'nosti v organakh ispolnitel'noi vlasti Belgorodskoi oblasti (opyt pilotnogo regiona) . Available at: http://www.pm-conf.ru/files/04122014/presentations/Pavlova.pdf..

- Razgulina E.D. Otsenka vliyaniya krupneishikh predpriyatii na sotsial'no-ekonomicheskoe razvitie territorii . Ekonomicheskie i sotsial'nye peremeny: fakty, tendentsii, prognoz , 2014, no. 3 (33), pp. 223-234..

- Tatarkin A.I., Tatarkin D.A., Levanova K.A. Partnerstvo vlasti i biznesa v realizatsii strategii razvitiya territorii . Ekonomika regiona , 2008, no. 4, pp. 18-30..

- Uskova T.V., Razgulina E.D. O roli investitsii v sotsial'no-ekonomicheskom razvitii territorii . Ekonomicheskie i sotsial'nye peremeny: fakty, tendentsii, prognoz , 2015, no. 2 (38), pp. 72-89..

- Uskova T.V., Razgulina E.D. Sotsial'naya otvetstvennost' biznesa: problemy i tendentsii: preprint . Vologda: ISERT RAN, 2015, 56 p..

- Uskova T.V. Sotsial'no-ekonomicheskoe razvitie territorii: problemy effektivnosti regional'noi politiki . Problemy razvitiya territorii , 2016, no. 2, pp. 7-18..

- Uskova T.V. Chastno-gosudarstvennoe partnerstvo kak mekhanizm modernizatsii ekonomiki territorii: teoretiko-metodologicheskie osnovy . Problemy razvitiya territorii , 2013, no. 3, pp. 7-16..

- Banon J.-Cl. Partenariat public-privé et croissance en Europe. Confrontations Europe, 2011, July-September, no. 95, pp. 28-29.

- Carroll A.B. A three-dimentional conceptual model of corporate performance. Academy of Management Review, 1979, no. 4 (4), p. 500.

- Williams C.A., Crane A. et al. Corporate Social Responsibility in a Comparative Perspective. The Oxford Handbook of Corporate Social Responsibility. Oxford: Oxford University Press, 2008.

- Uskova T.V., Razgulina E.D. Social responsibility of Russian business: theoretical vision and practical implementation. Transfer inovácií, 2013, no. 26, pp. 9-12.