Directions for improving the audit of securities transactions in banks in accordance with international standards

Author: Mamedova Nigar Akim

Article in issue: 3, 2022.

Free access

The purpose of the study is to analyze the role of international auditing standards in the regulation of auditing and to identify areas for improving the audit of securities transactions in banks. The article addresses international auditing standards and their objectives, which are of particular importance in the audit of financial instruments. At the same time, the interrelationships of International Financial Reporting Standards and International Standards on Auditing are considered as effective tools for the formation of quality financial information. One of the issues that attracts attention in the article is the identification of important trends in the development of internal audit of banks in the environment of digitalization and change, and tasks that are adequate to modern challenges. The problems raised in the article and the results obtained on the basis of the research can be useful in determining the prospects for the development of the audit, in assessing the feasibility of applying international standards in this area.

Audit, banking, financial instruments, securities transactions, internal audit, international auditing standards, digitization, continuous audit

Short address: https://sciup.org/148325444

IDR: 148325444 | UDC: 657.6 | DOI: 10.18101/2304-4446-2022-3-60-66

Направления совершенствования аудита операций с ценными бумагами в банках в соответствии с международными стандартами

Целью исследования является анализ роли международных стандартов аудита в регулировании аудиторской деятельности, а также определение направлений совершенствования аудита операций с ценными бумагами в банках. В статье рассматриваются международные стандарты аудита и их цель, что имеет особое значение при аудите финансовых инструментов. При этом взаимодействие международных стандартов финансовой отчетности и международных стандартов аудита рассматривается как эффективный инструмент формирования качественной финансовой информации. Одним из вопросов, рассматриваемых в статье, является выявление тенденций развития внутреннего аудита банков в условиях цифровизации и изменений, а также задач, соответствующих современной проблематике. Поднятые в статье вопросы и полученные на основе исследования результаты могут быть полезны для определения перспектив развития аудита и при оценке целесообразности применения международных стандартов в этой области.

Text of the scientific article Directions for improving the audit of securities transactions in banks in accordance with international standards

Rapid changes in the external environment, intensification of integration and globalization processes have stimulated the emergence of new methods, systems and approaches to governance. The complexity of management problems and the need for their comprehensive solution increase the importance of internal audit as an integral part of corporate governance. Internal audit is one of the most realistic ways to increase efficiency and identify opportunities to ensure competitive advantage. Even a well-organized system of internal control needs to be evaluated for its effectiveness in terms of achieving its goals. Internal audit serves this purpose.

The need for internal control and audit of securities transactions in banks

Internal control and audit is an important infrastructure component that ensures the quality and reliability of the market entity's accounting (financial) reports and, as a result, is a means of increasing the level of trust for internal and external users of these reports.

Control over asset protection, identification of internal financial, material, and temporary reserves of the joint-stock company, financial risk management, analysis of op- timality, design of functional and linear structures, examination of contractual relations, security of economic activity, coordination of activities and procedures between structural units, cash flow analysis, and tax planning are some of the competencies (skills) of the internal audit service in practice.

The organization's founders and owners, as well as the relevant issuers and creditors who own the securities, are interested in acquiring credible information on the organization's financial condition and solvency, including outcomes for the present and future periods [2, p. 20]. Users of an entity's financial statements may obtain such information from the results of the audit process. Auditing is an integral part of the market economy mechanism. An integral attribute of a market economy is securities. Therefore, the audit of securities transactions is one of the important and new areas of auditing.

The system of internal control and audit has been operating in the country's banking sector for a long time as a mandatory organizational element. At present, the issues of practical audit in the banking sector of the country are regulated by International Standards on Auditing, and in this regard, a number of standards of auditing have been adopted.

From an accounting point of view, certain types of activities, processes, elements or the management system as a whole may be the objects of audits. Transactions with securities as an object of audit should be considered from the point of view of the type of audit. The fundamental difference between the essence of internal and external audit activity is that internal audit ensures the reliability of the organization of accounting, financial results, calculations, and external (external) audit proves only such reliability. As a result, the scope of an external (external) audit is determined by the substance of the contract between the auditor and the economic entity, whereas an internal audit determines the company's management needs, including those of the bank. As a result, the accounting and reporting of the audited entity's securities transactions are the objects of external (external) securities audit. Internal auditing focuses on specific forms of securities (corporate, debt, financial, and derivative assets) as well as their funding sources (private capital and liabilities of the audited entity) [4].

The role of International Auditing Standards in auditing activities

Audit work is carried out in accordance with the relevant auditing standards, which define the basic rules for conducting audits, uniform requirements for its quality and reliability. The use of audit standards provides a certain level of assurance of the reliability of the results of audits. The auditing standards system includes several levels of standards (international standard, national standard, etc.).

International Standards on Auditing (ISA) are a set of international auditing professional standards.

International Standards on Auditing consist of 5 interrelated parts, namely the main provisions, general standards, working standards, the standard of auditor opinions and reports, and special standards.

International Standards on Auditing consist of basic principles, necessary procedures and recommendations for the application of principles and procedures, and include an introduction outlining the objectives and objectives of the standard, sections and appendices explaining the nature of the standard. At present, the International Standards on Auditing include 44 standards [3, p. 12]. Based on some of the existing international standards, similar standards have been developed in Azerbaijan and are close in nature. However, Azerbaijan differs from international standards in the form of standards, which is primarily due to the specifics of the country's audit practice. In general, one of the main problems is the application of International Standards on Auditing. The application of International Standards on Auditing increases the value of the auditor's services, the auditors' insufficient understanding of the principles of international standards, the complexity of the structure and content of the standards, the scope of some changes to the standards, frequency and complexity, lack of a perfect mechanism to control the application of international standards, etc. With the adoption of the Law on Auditor Services on September 16, 1994, auditing activities in the country began to be carried out in accordance with international auditing standards [1]. Establishment of the «Audit-Azerbaijan” branch of the International Institute of Internal Auditors (IIA) in Azerbaijan in 1999, May 5, 2003 The Chamber of Auditors of the Republic of Azerbaijan became a full member of the European Federation of Accountants and Auditors (EFAA). On 14 November, the admission of an associate member to the International Federation of Accountants (IFAC) was one of the factors accelerating the application of international standards in auditing1. At the present stage, expanding the scope of application of international auditing standards in Azerbaijan is important in improving the quality of audit services and training of professional auditors.

International Financial Reporting Standards and International Standards on Auditing are effective tools for generating quality financial information. They are based on generalized world experience in accounting, reporting and auditing. The relationship between International Reporting and Auditing Standards is based on the unity of concepts applied in both standards and the use of International Financial Reporting Standards as a criterion for the overall compliance of audited reports with defined requirements [7].

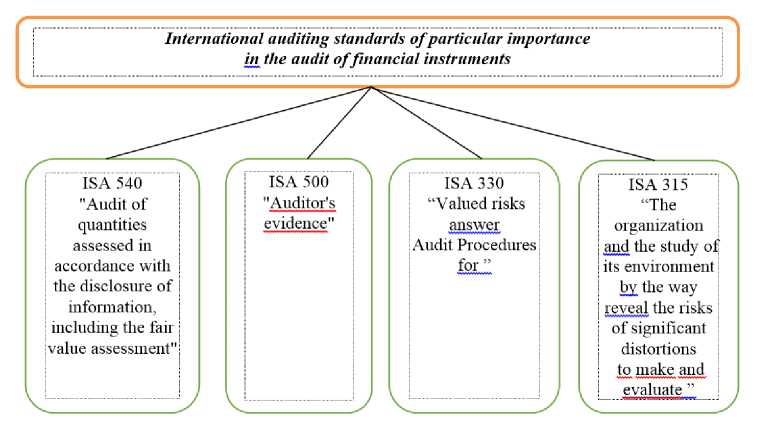

International auditing standards are widely used in the audit of financial instruments (Scheme 1).

International auditing standards of particular importance in the audit of financial instruments

ISA 540 "Audit of quantities assessed in accordance with the disclosure of information, including the fair value assessment"

answer

ISA 330 'Valued risks

Audit Procedures for "

ISA 315 “The organization and the study of its environment by the way reveal the risks of significant distortions to make and evaluate ”

ISA 500 " Auditor’s evidence "

Scheme 1. International auditing standards of special importance in the audit of financial instruments

ISA 540 «Audit of disclosed quantities, including fair value estimates” should be considered in conjunction with ISA 200 «Auditing in accordance with International Standards on Auditing and the Main Objectives of an Independent Auditor” 1 . This standard defines the auditor's responsibilities for auditing quantities measured in accordance with the disclosure of information in the financial statements, including fair value. The auditor's goal is to obtain sufficient audit evidence. The first of these arguments is the reasonableness of the valuation of the amounts recognized or disclosed in the financial statements, including fair value, and the second is that the appropriate disclosure of the information in the financial statements is sufficient in the context of the concept used in preparing the financial statements.

Explanation of the concepts used in the Standard, procedures for assessing related activities and risks and identifying and assessing significant distortion risks, response measures for assessed material misstatement risks, additional inspection procedures to mitigate significant risks, recognition and assessment criteria, disclosure of information on estimated values, etc. is given.

ISA 500 «Auditor's Evidence (Evidence)» defines what is included in the auditor's evidence when auditing financial statements and what the auditor's responsibilities are to develop and implement audit procedures to obtain sufficient and necessary audit evidence. invigorates 2 . The audit evidence obtained allows the auditor to make substantiated judgments that are relevant to the auditor's opinion.

This standard relates to specific aspects of the audit, ie ISA 315 «Detection and assessment of significant distortion risks by studying the organization and its environment”, ISA 570 «Continuity of operations”, ISA 520 «Analytical procedures”, ISA 330 «Assessed audit procedures for risk response ”and ISA 200» Conducting audits in accordance with International Standards on Auditing and the main objectives of an independent auditor ”. An explanation of the concepts used in the standard, sufficient and necessary audit evidence, information used as audit evidence, selection of items tested to obtain audit evidence, discrepancies in audit evidence or doubts about its validity, etc. is given.

ISA 330 «Audit Procedures for Responding to Assessed Risks” defines the responsibilities of the auditor for procedures to be developed and implemented in terms of detecting and assessing significant distortion risks 3 . This standard should be considered in conjunction with ISA 315 «Identifying and assessing the risks of material misstatement through a study of the entity and its environment” and ISA 200 «Conducting audits in accordance with international auditing standards and the main objectives of an independent auditor”.

Through the formulation and implementation of proper audit processes, the auditor's goal is to acquire sufficient and appropriate audit evidence about material misstatement risks. The standard uses the notion of an authentication procedure, which includes detailed tests of the types of transactions, account balances, disclosure of information, analytical procedures for authentication checks, as well as testing of controls.

This document describes general audit procedures, audit procedures to respond to significant distortion risks assessed at the initial level, testing of controls, nature and scope of controls testing, timing of controls testing, and interim audit evidence. use of control devices, assessment of operational efficiency of control means, etc. issues are reflected.

ISA 315, Identifying and Assessing Significant Distortion Risks by Studying the Organization and Its Environment, covers the identification and assessment of material misstatement risks in the financial statements, as well as the application of appropriate measures to address those risks 1 . In other words, this standard defines the auditor's responsibilities to identify and assess the risks of material misstatement of the financial statements through a study of the entity and its environment, including the internal control system.

Directions for improving the accounting and reporting system in Azerbaijan The auditor's goal is to identify and assess significant risks of misstatement due to either inaccuracies or negligence at the level of the initial and financial statements through a study of the entity and its environment. The standard defines business risk, internal control system, significant risk, risk assessment procedures, etc. concepts such as.

Thus, the improvement of Azerbaijan's accounting and reporting system and its harmonization with international standards has made it necessary to apply international auditing standards in auditing, allowing the gradual elimination of existing shortcomings and inconsistencies in this area adequately to the requirements of a market economy. The following results can be formed based on the research:

-

- International auditing standards are a set of documents that ensure the appropriate level of quality of audit and related services and formulate uniform requirements. In other words, it is the common international principles and standards that all auditors are obliged to follow in the course of their audit activities.

-

- International Standards on Auditing are well-thought-out and highly sound methodology and process control. Therefore, there is no need to complicate the widespread application of international auditing standards. The main requirement of the audit is to ensure the required quality of performance in order to form an accurate opinion on the financial statements. Quality of work — the audit process ensures the implementation of all technological processes that can describe, without neglecting any operation. This means that the audit process must be regulated in detail. Standards are process regulations.

-

- International auditing standards are universal, with a logical systematization and a clearer explanation mechanism. Its application is to achieve high quality of audit, to define uniform requirements for the audit procedure, to understand the process of audit of internal and external (external) users, to increase professional knowledge in the field of auditing, the relationship between the various elements of the audit process, information to ensure reliability and completeness, etc.

-

- Today, in an unstable business environment, banks face a wide range of complex business issues. Effective internal audit is an important factor in effective risk management and management as a whole. Internal audit in banks is an integral component

of the control system. The environment of digitalization and change has formed important trends in this area and has set tasks that are adequate to modern challenges. Important trends in the development of internal audit of banks are its transformation from security to driving force, change of risks (the leading position in the group of ricks will be not financial risks, but risks related to information systems and information technologies), high dynamic planning. application (transition from periodic audit to risk-oriented planning, real-time planning), use of modern technologies (software for management purposes by internal audit — internal audit management software, large amounts of data analysis- data mining, continuous audit — continuous auditing) and work with the necessary skills, especially communication, modern information technology, work with information skills, knowledge of business areas, etc. (changes in the technology used in internal audit increase the demand for auditors with the necessary knowledge and skills in this area).

Conclusion

Internal audit is an effective tool for internal control and risk management in banks. One of the current problems of modern audit in the banking sector is the application of international auditing standards. International auditing standards are international principles and standards that are important to apply in the audit process. The application of international auditing standards is aimed at improving the quality of audit services, defining uniform requirements for the rules of auditing, understanding the process of audit by internal and external users, etc. plays an important role.

The founders and shareholders, as well as the relevant issuers and creditors who own the securities, are interested in obtaining reliable information about the financial condition and solvency of the organization, the results based on the current and future period. Users of an entity's financial statements may obtain such information from the results of the audit process. One of the important and new directions of the auditor's activity is the organization of the audit of securities transactions of banks in accordance with international standards, which is an integral attribute of a market economy.

References Directions for improving the audit of securities transactions in banks in accordance with international standards

- On Audit Service: Law of the Republic of Azerbaijan of September 16, 1994. Available at: https://audit.gov.az/uploads/Auditor_xidmeti_haqqinda_qanun_eng.pdf (accessed: 08.02.2021).

- Bashkatov V. V., Minakov E. R., Sarkisova N. A. Basic Aspects of Accounting and Reporting of Financial. VestnikAltaiskoi akademii ekonomiki iprava. 2020; 8: 19-24. (In Russ.).

- Vorona M. R., Oleinik M. A. Perekhod na mezhdunarodnye standarty audita v Rossii [Transition to International Auditing Standards in Russia]. Problemy i perspektivy razvitiya ekonomicheskogo kontrolya i audita v Rossii. Proc. VIII All-Russ. scientific and practical conference of young scientists. 2019. Pp. 10-15. (In Russ.).

- Likhtarova O. V. Problem Recognition and Presentation of Financial Instruments in the Russian Corporate Reporting Companies // Economics and Innovations Management. 2020: 8. P. 5-9. (In Russ.).

- Loschenko E. V., Dashkevich P. M., Kazantsev L. V. Automated Control Systems: Opportunities, Comparison, Development Prospects // System Analysis & Mathematical Modeling. 2020. V. 2. No. 1. Pp. 54-62. (In Russ.).

- Morozova A. A., Kirilina E. V. Problemy i neobkhodimost primeneniya mezhdunarod- nykh standartov v Rossii [Problems and the Necessity of Application of International Standards in Russia]. Vmire nauchnykh otkrytii. 2019. V. IV, part 2. Pp. 226-228. (In Russ.).

- Rozhnova O.V. Harmonization of Accounting, Auditing and Analysis in a Digital Economy. Accounting. Analysis. Auditing. 2018; 5(3): 16-23. (In Russ.).

- Hayali A., Dinc Y., Sarili S., Dizman A.C., Gundogdu A. Importance of the Internet Control System in Banking Sector: Evidence from Turkey. Available at: https://www.lcbrarchives.com/media/files/13fec27.pdf (accessed 12.05.2021).