Meta-learning Approach for Time Series Forecasting: First-order MAML and Reptile

Author: Pratik Zinjad, Tushar Ghorpade, Vanita Mane

Journal: International Journal of Intelligent Systems and Applications @ijisa

Article in issue: 2 vol.18, 2026.

Free access

Forecasting time series data especially in volatile sectors like financial markets, shows significant challenges due to non-linearity, non-stationarity and noise in the data. Traditional forecasting models most likely fail to generalize effectively across varying tasks without extensive retraining. This study investigates the application of meta learning techniques, particularly First-Order Model-Agnostic Meta-Learning (FOMAML) and Reptile, to make adaptability and generalization better in time series forecasting tasks. An extensive empirical study was done using three neural networks as base models, namely Long Short Term Memory (LSTM), Gated Recurrent Unit (GRU) and Feed Forward Neural Network (FFNN) applied to four real-world stocks: TCS, TATASTEEL, GRASIM and DJIAHD. The models were evaluated under few-shot learning(defined here as 211-shot learning using sliding window samples) conditions with varying iteration counts(outer loops or epochs) and their effectiveness was checked using some common standard metrics like RMSE(Root Mean Squared Error), MAE(Mean Absolute Error) and R²(Coefficient of Determination). Outcomes have shown that meta-learning approach notably performs much better than traditional models with MAML(First Order) in particular showing quicker task adaptation as well as stable convergence behavior, especially when it used with GRU and LSTM as base models, as validated empirically on the GRASIM dataset where the MAML with LSTM configuration attained around 81.9\% reduction in RMSE (dropping the value from 622.94 to 112.60 over the iterations). In all four stocks, reptile shows relatively steady performance. The study validates the potential of meta-learning as a powerful framework for time series forecasting problem in dynamic settings which offers robust algorithmic foundation for numerous future financial modeling applications.

Few-Shot Learning, GRU, LSTM, MAML, Meta-learning, Reptile, Stock Price Prediction, Time Series Forecasting

Short address: https://sciup.org/15020318

IDR: 15020318 | DOI: 10.5815/ijisa.2026.02.03

Text of the scientific article Meta-learning Approach for Time Series Forecasting: First-order MAML and Reptile

Published Online on April 8, 2026 by MECS Press

Forecasting time series data, especially in financial areas like stock markets, presents a persistent challenge because of the data's noisy, non-linear, and non-stationary characteristics. Conventional forecasting models most likely needs an extensive amount of retraining when faced to new datasets or market conditions, which restricts their scalability and adaptability. This inefficiency emerges as one of the important factors in dynamic environments like equity markets, where swift changes required models that can generalize and adapt more quickly. Recent advancements that are done in meta-learning makes it an effective approach by enabling models to learn how to learn making quick adaptation to new tasks with minimum fine-tuning. Specifically, algorithms like MAML(used here in its First-Order (FOMAML) formulation for better efficiency) and Reptile have ability of efficient knowledge transfer among multiple time series tasks, greatly minimizing the need for large size labeled datasets and extensive amount of training [1,2]. Inspired by the success of meta-learning in a number of other fields, this paper explores its application in time series forecasting to be specific to build adaptive models which not only maintain high accuracy but also minimize training time and computational cost. The Objectives of this research paper are as follows:

-

• Explore and implement MAML(First order) and Reptile algorithms for problem of time series prediction.

-

• Compare the effectiveness of meta-learning approaches with traditional time series forecasting methods like Autoregressive Integrated Moving Average (Arima), Seasonal Autoregressive Integrated Moving Average (Sarima), etc. using visualizations to show the results.

-

• Evaluate and explore the adaptability and generalization capabilities of MAML and Reptile algorithms across different conditions or tasks.

-

• Demonstrate the effectiveness of meta-learned models using low-data and few-shot learning scenarios, using real world historical data.

-

• Analyze the pros and cons of each meta learning approach through empirical results and visualizations while providing insights for future improvement.

-

• We propose a thorough empirical investigation of two meta-learning approaches those are MAML(First Order) and Reptile, in the context of time series prediction.

-

• We merged these meta-learning approaches with various base models like LSTM networks, GRU and FFNN, to show their adaptability in various financial time series prediction tasks.

-

• Our experimental work specifically focuses on stock price prediction problem, where we use few-shot learning (211shot learning) settings while training used models using varying iteration counts (10, 20, ....., till 100),

which makes us easy to systematically investigate the factors like convergence speed, stability, and forecasting performance.

• We studied the behavior of each base model (neural network architecture) using with both MAML(First Order) and Reptile frameworks to identify which combinations give us better performance using low data and task variant settings.

• In contrast to traditional forecasting models our suggested strategy focuses on task adaptation and generalization across various temporal tasks which is especially vital in fast paced financial markets where quick learning from small amount data is very much needed.

2. Related Works

2.1. Survey of Existing System2.2. Limitations of Existing System / Research gap

This paper is structured into five main sections. The Related Work or Literature Survey is presented in Section 2 of the paper which starts with a thorough review of existing systems and methodologies used for the problem of time series forecasting, followed by limitations and research gaps in existing systems. The Proposed System is described in section 3, including an introduction to meta-learning, the architectural framework used, algorithmic implementation using FOMAML and Reptile, and the hardware-software required to carry out this work. It also outlines the evaluation metrics used to explain the performance of the investigation done. The experiment and results are explained in detail in Section 4, where the proposed approach is assessed using real stock market stocks i.e TCS, Tata Steel, Grasim and DJIAHD, along with a comparative analysis against various traditional models like Arima, Sarima, etc. The investigation’s findings are summarized in section 5, which also discusses possible directions for future research.

Time series forecasting plays a crucial role in various real-world applications which includes financial market prediction, energy consumption estimation, weather forecasting, and healthcare analytics. Traditional models like exponential smoothing and ARIMA most probably suffer with the problem of non-linearity and noise when working with modern datasets. On the other hand, while using deep learning-based architectures like LSTM [6], GRU and FFNN after investigating the findings have shown strong capabilities in catching temporal patterns and long-term dependencies. But these models want huge amounts of data as well as training when learning needs to get transfer to new tasks, which will cause an inefficiencies in dynamic or low-resource situations. To fix these cons, recent research has been done towards meta learning, a concept that make models to quickly adapt to new tasks with small amount of data. Meta learning approaches, particularly MAML [3,7] and Reptile [4], have shown promising results in the domains like computer vision and reinforcement learning. These algorithms aim to learn a good initialization of model parameters such that a few gradient steps with a small amount of task-specific data can yield optimal performance. Despite their success to learn general tasks easily, their application to time series forecasting remains an emerging area of research. Some efforts have been made and tried to integrate meta-learning with time series forecasting. Chang et al. [8] used a meta-learning framework for short term stock price-trend prediction, leveraging the rapid adaptation capability of meta-learners successfully. Song et al. [9] given a weighted meta extreme learning model for stock prediction, implementing and showing that meta learning can improve generalization across various financial time series tasks. Similarly, Maya et al. [10] used a meta-transfer learning model to handle missing data values in time series, to show improved adaptability across varying temporal patterns.

A novel direction was introduced by van Zyl [11], who introduced late fusion using representation based learning and meta-learning for forecasting, suggesting that learning useful data representations before meta-training can make performance better across various tasks. Another magnificent work done by Xiao et al. [12], where a multi stage loss optimization strategy was developed to make gradient-based meta-learning approaches better, thereby enhancing the convergence behavior of models like MAML and Reptile. Furthermore, comprehensive surveys done by Hospedales et al. [13] and Barman et al. [14] have worked on meta-learning architectures, categorizing optimization-based algorithms (like MAML, Reptile), model-based learners, and metric-based approaches. These surveys give foundational understanding and explain emerging challenges in applying meta-learning techniques to sequential data such as time series. Several hybrid models have also emerged that indirectly relate to the concept of meta-learning. Samanta et al. [1] elaborated a Meta-cognitive Recurrent Fuzzy Inference System (McRFIS-MN) with memory neurons, focusing on quick learning with online adaptation in temporal domains. Li et al. [2] proposed a hybrid forecasting model that combines LSTM with LMS filtering and ISSA-based optimization algorithm. Although it is not a classical metalearning technique, these models have similar goals of rapid adaptation and generalization. Parallel advances have been made in representation based meta-learning techniques. For example, Gutowska et al. [15] explored constructing metalearning model for unsupervised anomaly detection while providing insight into learning task specific embeddings. Other works like Noor and Fatima [16] worked specifically on adapting meta-learning strategies specifically for financial time series, practically showing the impact of task design and feature distribution alignment in low-resource settings. Recent studies have also introduced dynamic models tailored for long-term time series forecasting. Ma’sum et al. [17] developed a Meta-Transformer Networks model that uses attention-based dynamic modeling, which fits well with the time-varying nature of real-world data. In the context of few-shot and continual learning, works such as those by Chi et al. [18], Zhuang et al. [19], and Zhao et al. [20] proposed meta-learning strategies that could most likely be adapted to incremental time series forecasting, mostly under changing distributions or task settings. There is limited empirical proofs comparing the convergence speed, stability, and transferability of these meta-learning algorithms in temporal forecasting situations. For instance, although Wen and Li [21] improved LSTM models using attention mechanisms to make forecasting performance better, their work does not show cross-task model adaptation, which we see in most of the meta-learning approaches.

While several studies have explored meta-learning algorithms for time series tasks in various ways, a comprehensive empirical investigation of MAML and Reptile merging with deep sequence models, remains underexplored. This highlights a gap here in understanding how gradient-based meta-learners perform in dynamic time series settings/conditions and whether their theoretical advantages get translate to solve practical forecasting problems.

Despite receiving more attention to meta-learning and its applications in various sectors including time series forecasting, existing research reveals several critical limitations that highlights the need for more systematic empirical investigation, particularly for meta-learning algorithms like MAML and Reptile.

-

• Inadequate Exploration of Base Model Influence:

-

• Limited Comparative Studies on MAML(First Order) and Reptile using Neural prediction Models:

-

• Less Evaluation Across Varying Inner Loop Iterations:

Meta-learning algorithms mostly rely heavily on the number of inner loop updates for proper task adaptation. However, current approaches typically keep fixing the number of iterations, while ignoring the possible difference in learning dynamics and convergence behavior that might come with different iteration counts. As mentioned by Yao et al. and Nichol et al., inner loop design plays a pivotal role in performance, yet few studies showed a systematic variation in inner loop iterations, especially in the context of time series [12].

-

• Training Stability and Convergence in Temporal Contexts:

The training stability and convergence behavior of MAML and Reptile algorithm on time series forecasting in existing literature remains unexplored. Although these aspects are studied in image-based tasks, temporal data introduces unique convergence challenges due to its inherent sequential dependencies and variable input lengths. Yao et al. and Nichol et al. acknowledge optimization issues but do not extend this analysis to recurrent or sequence based models [12].

-

• Less Focus on Model-Agnostic Meta-Learning for Time Series Problems:

While MAML and Reptile are designed to be model-agnostic, their applications for time series forecasting problems remain underdeveloped. Surveys such as those by Hospedales et al. and Son et al. primarily focus on vision and NLP tasks, leaving temporal domains relatively underexplored. The unique characteristics of time series data like seasonality, trends and temporal dependencies adds some additional challenges that are not properly solved in general meta-learning frameworks [13,22].

-

• Few-Shot Prediction Remains Underrepresented:

Despite the theoretical alignment of meta-learning with the concept of few-shot learning, few-shot forecasting has not received proper attention. Most of the research remains focused on classification or regression kind of problems in static domains. Although Pilyugina et al. discuss meta-learning strategies in data-scarce conditions, empirical benchmarks for few-shot time series forecasting, particularly using MAML and Reptile, remain limited [23].

• Absence of Standardized Evaluation Metrics:

3. Proposed Approach3.1. Architecture/Framework

Another limitation in existing literature survey is the lack of consistency in use of evaluation metrics, making cross study comparisons difficult. While metrics such as MAE, RMSE and R 2 are commonly used, they are not uniformly adopted across current meta-learning studies. Furthermore, very few works simultaneously evaluate the combined effects of base model architecture, inner loop iterations, and meta-learning algorithm on forecasting accuracy using a proper unified metric framework [23,24].

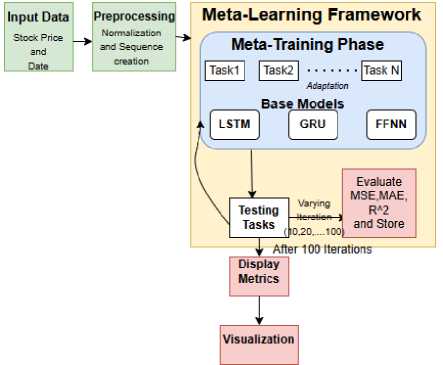

Time series forecasting is used in various sectors includes finance, healthcare, etc. Traditional deep learning algorithms need large amounts of data and more computational resources for training when compared to meta-learning algorithms. Also, meta-learning techniques like MAML(First Order) and Reptile provide an efficient approach for training models that generalize well across multiple tasks. This study explores a meta-learning framework using LSTM, GRU, and FFNN as base models for stock price prediction. The proposed framework consists of a meta-learning pipeline that includes preprocessing, base model training, meta-update, and evaluation phases, as shown in Fig 1.

Fig.1. Meta-learning framework

The following sections describe each component of the architecture in detail.

-

• Input Data and Preprocessing: The dataset comprises of historical stock prices and corresponding timestamps. The preprocessing step involves:

Normalization: Min-Max Scaling is applied to convert the input values which will lie within a specific range after conversion, improving model convergence.

Sequence Creation: The input sequences are created with a look-back period of 60 time steps, enabling the model to capture proper temporal dependencies.

Testing was done on the final, most recent 20 percent of the chronologically ordered dataset.

-

• Meta-Training Phase: In this phase, the base models (LSTM, GRU, FFNN) are trained on multiple tasks extracted from different time segments of the stock price data. The training process is performed under two meta-learning paradigms: Here, task is distinct and contiguous segment of historical data(271 day window). Each dataset consisting of 271 records was partitioned into 10 distinct temporal task and each task provides a 211-shot learning condition after accounting for the 60 days look back window.

MAML(first order): The model learns an initial set of parameters using a first-order approximation (ignoring second derivatives) to minimizing computational overhead which allows fast fine-tuning on unseen tasks.

Reptile: The model updates its parameters by moving towards the average parameter values obtained from multiple tasks.

-

• Meta-Model and Meta-Update: The meta-model aggregates knowledge from multiple training tasks through meta updates. In MAML, meta-updates are computed by averaging gradients across tasks, whereas Reptile uses parameter interpolation to achieve better generalization.

-

• Unseen Task Evaluation: The trained meta-model is tested on an unseen forecasting task. The evaluation is conducted using three key metrics: MSE, MAE and R 2

-

• Visualization and Comparison: Predictions obtained from LSTM, GRU, FFNN models trained with MAML and Reptile and predictions obtained from traditional models are presented strategically in single figure of all the four stocks(4 figures i.e fig 2,3,4,5).

-

3.2. Algorithm

Algorithm 1 First-Order MAML(FOMAML) for Stock Price Prediction (Base Model: LSTM/GRU/FFNN)

-

1: Initialize: Base model parameters θ , learning rates α , β

-

2: while not converged do

-

3: Sample batch of tasks T i ~ p (T)

-

4: for each task T i do

-

5: Sample dataset D i '•■, D i test

-

6: Compute training loss: £i ( 9 ) on D i“■

-

7: Compute adapted parameters: 9 i‘ = 9 - a V в £ i ( 9 )

-

8: end for

-

9: Compute meta-loss: £ i £ i ( 9 i ') on £ i test

-

10: Update meta-parameter: 9 ^ 9 - P V в £ i £ i ( 9 i '))

-

11: end while

9 i‘ = 9 - aV 9 £ i ( 9 ) (1)

Here, a represents the learning rate used for the task-specific adaptation.

The outer loop emphasis on the meta-learning aspect. The performance of the adapted or modified parameters θ i ′ is assessed on a different query dataset, £ i test, for the same task. The meta-objective is then computed by adding up the losses for every task that was taken into consideration. To guarantee computational efficiency, we used here the First-Order MAML (FOMAML) approximation. In contrast to standard MAML which need to calculate second-order derivatives (Hessian matrices). FOMAML ignores second-order terms in order to approximate the meta-gradient. This preserves strong performance while drastically lowering memory use as well as computational expense. The original model parameters i.e θ , are subsequently updated based on this aggregated meta-loss gradient:

9 ^ 9 - PV 9 £ i £ i ( 9 i '))

In this update rule, β signifies the meta-learning rate. This iterative process encourages the meta-model to learn a parameter initialization that exhibits strong generalization capabilities across diverse forecasting or regression tasks, allowing for efficient fine-tuning on new or unseen tasks with very few gradient steps.

Algorithm 2 Reptile for Stock Price Prediction (Base Model: LSTM/GRU/FFNN)

-

1: Initialize: Base model parameters θ , learning rates α , β

-

2: while not converged do

-

3: Sample batch of tasks T i ~ p (T)

-

4: for each task T i do

-

5: Sample dataset £ i

-

6: Perform k SGD updates: 9 i' = 9 - a V 9 £ i ( 9 )

-

7: end for

-

8: Update meta-parameter: 9 ^ 9 + P(9i' — 9)

-

9: end while

Reptile is a meta-learning algorithm that uses a first-order approximation to estimate the meta-gradient, which avoids the computational cost associated with second-order derivatives. In contrast to MAML, Reptile updates the global meta-parameters by shifting them in the direction of the task-specific parameters that are obtained after performing several steps of standard gradient descent on individual tasks. For each task T i sampled from the task distribution, the base model is trained on the task-specific dataset £ i for k iterative gradient descent steps. This process leads to the task-adapted parameters θ i ′ . Each step in this inner loop update can be represented as:

9 ^ 9 - a V 9 £ i ( 9 )

This update is repeated k times to obtain the final task-adapted parameters θ i ′ . Following this task-specific training, the meta-update is performed according to the following rule:

9 ^ 9 + в ( 9 i ‘ - 9 )

-

3.3. Details of Hardware & Software

-

3.4. Evaluation Parameters

The experimental setup for this investigation was implemented using Google Colaboratory (Colab), a cloud-based interactive development environment or notebook that supports GPU and TPU acceleration for executing intense codes in various programming languages. Using Colab notebooks cloud infrastructure it gives the seamless execution of computationally intensive meta-learning algorithms, particularly MAML and Reptile, applied to time-series forecasting tasks. The virtual machine environment was equipped with an Intel Xeon processor and where applicable, computation was accelerated using an NVIDIA Tesla T4 GPU. The notebook provided 12 GB of dynamic RAM and integration with Google Drive was utilized for efficient data management, reading dataset and model checkpointing.

From a software perspective, the experiment was carried out in a Python 3.9+ environment along with PyTorch (version 1.13 or higher) as the primary deep learning framework. several other libraries were utilized to support different phases of the modeling pipeline: NumPy used for performing various numerical operations, Pandas used for performing data preparation and manipulation, and Scikit-learn used here for performing normalization procedures and evaluation metrics computation. Matplotlib was used to generate performance visualizations, while PrettyTable given organized display of quantitative results in tables. The Google Drive API was used here to safely access and save data while making sure that there is reliable and consistent file management during sessions.

The integration of these tools made experimentation easy as well as efficient with the utilization of neural architectures as base models under the meta-learning paradigm, supporting both scalability and reproducibility. This environment proved particularly effective for training and evaluating complicated models across various stock datasets, guaranteeing that the computational requirements of the investigation were satisfied without sacrificing performance as well as flexibility.

To evaluate the effectiveness of the proposed meta-learning models, namely MAML(First Order) and Reptile, when integrated with various base learner models like LSTM, GRU, and FFNN for the tasks of stock price prediction, here we have employed the following standard performance metrics:

Root Mean Square Error (RMSE)

RMSE is a commonly used metric in regression based analysis to quantify the average magnitude of the errors between predicted and actual values. RMSE gives higher weight to larger prediction errors due to the squaring of difference. It is mathematically defined as:

RMSE = ^Т^^У2 (5)

In Eq.5, У( represents the actual or label value y j denotes the predicted value, and n is the total number of input data points.

Mean Absolute Error (MAE)

MAE gives a measure of the average absolute difference between the predicted and observed values. Unlike RMSE, MAE treats all prediction errors uniformly, without differential weighting based on their magnitude. The formula for MAE is:

MAE^Z ’LJ y i -yJ (6)

In Eq. 6, yj is the actual or label value yj is the predicted value, and n is the number of input data points.

Coefficient of Determination (R² Score)

R² score is a statistical measure that represents the proportion of the variance in the dependent variable that is predictable from the independent variables. It essentially indicates the goodness of fit of the model to the data. The R² score is calculated as follows:

R2 = 1 -

Г^СугЛ)2

Z "=1 (y i -y) 2

In Eq. 7, y j represents the actual or label value, y j is the predicted value, and у is the mean of the actual values. An R² score to 1 shows a better fit of the model to the data.

4. Experiments

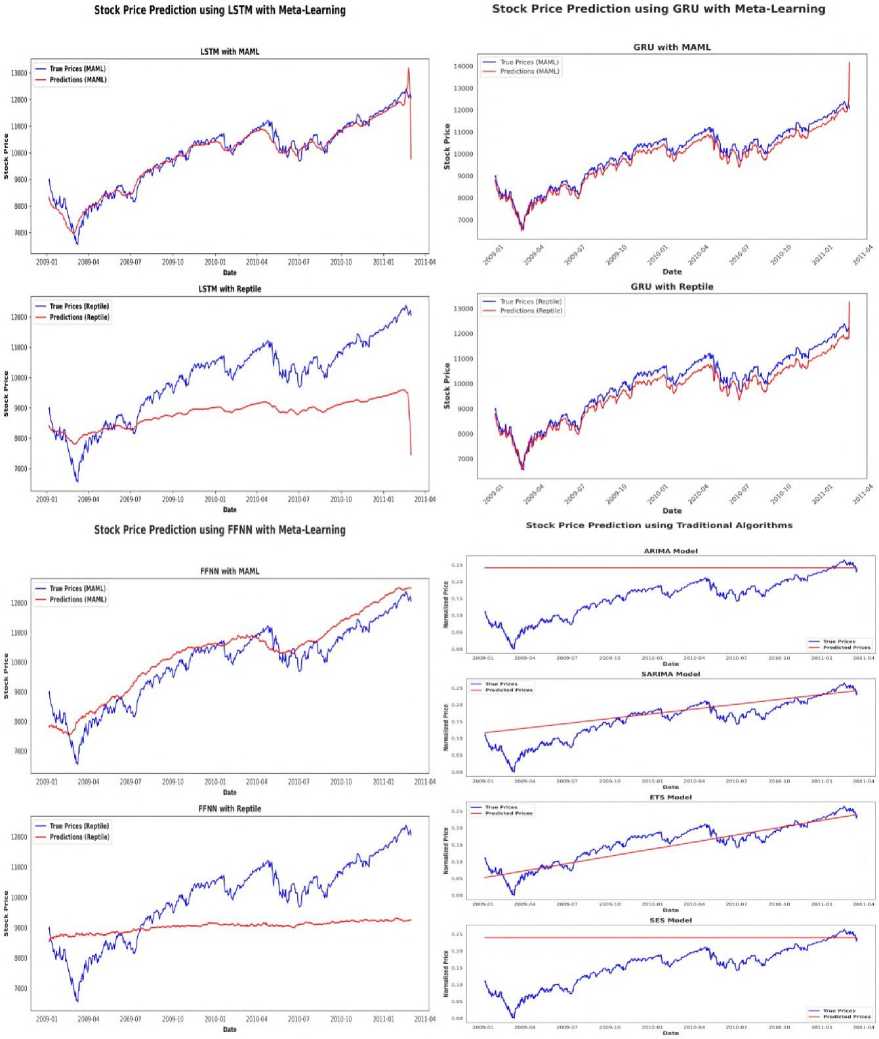

This section explains a comprehensive evaluation of stock price prediction models using two well known meta- learning approaches like MAML(First Order) and Reptile integrated with three neural network architectures: LSTM, GRU, and FFNN. The evaluation or investigation was done on four different stocks dataset those are TCS, TATASTEEL, GRASIM, and DJIA index—to check robustness and generalizability of the models across varying market behaviors. The Nifty Fifty dataset (2010–2021) was used as the source for TCS, TATASTEEL, and GRASIM, while the DJIAHD dataset (2009–2019) was used for U.S.-based stocks(Dow Jones Industrial Average Index). Each model was trained and tested using both meta-learning frameworks with a varying number of iterations, ranging from 10 to 100. Performance was rigorously evaluated using three standard statistical metrics: RMSE, MAE, and R².

Note: To validate the statistical significance of our observations, we did the Diebold-Mariano (DM) test. Comparing the proposed best performing MAML(First Order) with GRU model against the ARIMA baseline we got a p-value of p < 0.001. Furthermore, a comparison against the alternative meta-learning approach (Reptile) also resulted in a significant p-value (p < 0.001). These results confirm that the performance improvements of the MAML-GRU framework are statistically significant and not due to random chance or luck.

Table 1. Performance comparison of MAML(First Order) and reptile with different base models and iterations on tcs stock data

|

TCS Stock |

Metric |

Number of Iterations |

||||||||||

|

10 |

20 |

30 |

40 |

50 |

60 |

70 |

80 |

90 |

100 |

|||

|

LSTM |

MAML |

RMSE |

447 . 51 |

456 . 11 |

332 . 76 |

370 . 97 |

428 . 42 |

480 . 09 |

302 . 94 |

194 . 95 |

308 . 37 |

204 . 55 |

|

MAE |

390 . 89 |

351 . 26 |

269 . 47 |

317 . 03 |

369 . 77 |

445 . 66 |

245 . 01 |

134 . 87 |

264 . 83 |

148 . 49 |

||

|

Rˆ2 |

0 . 41 |

0 . 39 |

0 . 68 |

0 . 60 |

0 . 46 |

0 . 32 |

0 . 73 |

0 . 89 |

0 . 72 |

0 . 88 |

||

|

Reptile |

RMSE |

233 . 80 |

238 . 95 |

226 . 21 |

223 . 95 |

199 . 96 |

489 . 65 |

305 . 79 |

359 . 89 |

371 . 40 |

281 . 54 |

|

|

MAE |

185 . 69 |

191 . 11 |

177 . 71 |

175 . 88 |

146 . 64 |

451 . 77 |

265 . 46 |

318 . 47 |

332 . 34 |

240 . 94 |

||

|

Rˆ2 |

0 . 83 |

0 . 83 |

0 . 85 |

0 . 85 |

0 . 88 |

0 . 29 |

0 . 72 |

0 . 62 |

0 . 59 |

0 . 76 |

||

|

GRU |

MAML |

RMSE |

445 . 69 |

326 . 15 |

202 . 41 |

283 . 11 |

203 . 96 |

359 . 64 |

187 . 42 |

151.13 |

180 . 62 |

217 . 27 |

|

MAE |

366 . 86 |

286 . 19 |

141 . 98 |

242 . 65 |

149 . 44 |

317 . 74 |

129 . 67 |

158 . 89 |

120.05 |

166 . 73 |

||

|

Rˆ2 |

0 . 41 |

0 . 68 |

0 . 87 |

0 . 76 |

0 . 87 |

0 . 62 |

0 . 89 |

0 . 86 |

0.90 |

0 . 86 |

||

|

Reptile |

RMSE |

220 . 04 |

222 . 88 |

225 . 68 |

231 . 44 |

240 . 02 |

242 . 52 |

243 . 17 |

244 . 36 |

245 . 32 |

246 . 09 |

|

|

MAE |

170 . 25 |

173 . 61 |

176 . 85 |

183 . 29 |

192 . 42 |

195 . 00 |

195 . 71 |

196 . 96 |

197 . 93 |

198 . 69 |

||

|

Rˆ2 |

0 . 85 |

0 . 85 |

0 . 85 |

0 . 84 |

0 . 83 |

0 . 82 |

0 . 82 |

0 . 82 |

0 . 82 |

0 . 82 |

||

|

FFNN |

MAML |

RMSE |

248 . 55 |

248 . 97 |

249 . 24 |

249 . 71 |

250 . 37 |

251 . 31 |

251 . 92 |

251 . 00 |

252 . 31 |

252 . 56 |

|

MAE |

185 . 62 |

188 . 37 |

189 . 41 |

190 . 74 |

192 . 25 |

193 . 35 |

193 . 91 |

195 . 09 |

195 . 93 |

196 . 37 |

||

|

Rˆ2 |

0 . 81 |

0 . 81 |

0 . 81 |

0 . 81 |

0 . 81 |

0 . 81 |

0 . 81 |

0 . 81 |

0 . 81 |

0 . 81 |

||

|

Reptile |

RMSE |

256 . 85 |

256 . 86 |

256 . 87 |

256 . 92 |

256 . 92 |

256 . 93 |

256 . 94 |

256 . 95 |

256 . 96 |

256 . 97 |

|

|

MAE |

202 . 78 |

202 . 82 |

202 . 87 |

202 . 96 |

202 . 97 |

202 . 98 |

202 . 99 |

203 . 01 |

203 . 03 |

203 . 84 |

||

|

Rˆ2 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 88 |

||

Table 2. Performance comparison of MAML(First Order) and reptile with different base models and iterations on tatasteel stock data

|

TATASTEEL Stock |

Metric |

No of Iterations |

||||||||||

|

10 |

20 |

30 |

40 |

50 |

60 |

70 |

80 |

90 |

100 |

|||

|

LSTM |

MAML |

RMSE |

302 . 86 |

167 . 51 |

156 . 03 |

151 . 88 |

142 . 06 |

135 . 45 |

120 . 36 |

174 . 57 |

123 . 57 |

146 . 43 |

|

MAE |

210 . 51 |

100 . 59 |

100 . 88 |

106 . 19 |

99 . 06 |

90 . 66 |

73 . 64 |

116 . 52 |

79 . 38 |

106 . 14 |

||

|

Rˆ2 |

0 . 28 |

0 . 78 |

0 . 81 |

0 . 82 |

0 . 84 |

0 . 85 |

0 . 88 |

0 . 76 |

0 . 88 |

0 . 83 |

||

|

Reptile |

RMSE |

144 . 96 |

143 . 66 |

138 . 39 |

116 . 98 |

119 . 72 |

139 . 76 |

273 . 67 |

279 . 38 |

382 . 77 |

381 . 58 |

|

|

MAE |

108 . 28 |

110 . 61 |

105 . 84 |

86 . 51 |

89 . 11 |

105 . 47 |

209 . 73 |

198 . 88 |

212 . 72 |

205 . 12 |

||

|

Rˆ2 |

0 . 83 |

0 . 83 |

0 . 85 |

0 . 89 |

0 . 88 |

0 . 84 |

0 . 41 |

0 . 39 |

0 . 28 |

0 . 29 |

||

|

GRU |

MAML |

RMSE |

303 . 41 |

136 . 31 |

130 . 99 |

129 . 53 |

134 . 31 |

109.88 |

118 . 43 |

125 . 52 |

134 . 02 |

124 . 59 |

|

MAE |

216 . 18 |

83 . 49 |

83 . 02 |

78 . 47 |

79 . 46 |

71.22 |

77 . 06 |

80 . 02 |

99 . 76 |

84 . 18 |

||

|

Rˆ2 |

0 . 28 |

0 . 85 |

0 . 86 |

0 . 86 |

0 . 85 |

0.90 |

0 . 89 |

0 . 87 |

0 . 85 |

0 . 87 |

||

|

Reptile |

RMSE |

147 . 79 |

125 . 41 |

118 . 04 |

120 . 22 |

120 . 89 |

119 . 04 |

119 . 52 |

117 . 01 |

119 . 79 |

122 . 47 |

|

|

MAE |

119 . 64 |

91 . 58 |

79 . 68 |

83 . 79 |

85 . 23 |

82 . 42 |

83 . 81 |

80 . 64 |

85 . 48 |

89 . 50 |

||

|

Rˆ2 |

0 . 83 |

0 . 87 |

0 . 89 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 88 |

0 . 89 |

0 . 88 |

0 . 88 |

||

|

FFNN |

MAML |

RMSE |

277 . 71 |

272 . 52 |

273 . 95 |

274 . 25 |

288 . 45 |

298 . 56 |

298 . 28 |

297 . 98 |

298 . 38 |

298 . 76 |

|

MAE |

185 . 23 |

182 . 08 |

182 . 88 |

182 . 92 |

190 . 62 |

196 . 21 |

195 . 89 |

195 . 53 |

195 . 48 |

195 . 66 |

||

|

Rˆ2 |

0 . 39 |

0 . 42 |

0 . 41 |

0 . 41 |

0 . 35 |

0 . 30 |

0 . 30 |

0 . 30 |

0 . 30 |

0 . 30 |

||

|

Reptile |

RMSE |

216 . 98 |

233 . 09 |

233 . 17 |

233 . 25 |

233 . 53 |

233 . 54 |

233 . 55 |

233 . 56 |

233 . 57 |

233 . 59 |

|

|

MAE |

182 . 81 |

205 . 28 |

205 . 42 |

205 . 56 |

205 . 93 |

205 . 95 |

205 . 97 |

206 . 00 |

206 . 03 |

206 . 07 |

||

|

Rˆ2 |

0 . 63 |

0 . 57 |

0 . 57 |

0 . 57 |

0 . 57 |

0 . 57 |

0 . 57 |

0 . 57 |

0 . 57 |

0 . 57 |

||

Fig.2. Performance comparison of MAML(First Order) and reptile with different base models on tcs stock data

FFNN with MAML

FFNN with Reptile

JOZIMV JOJO 10 Date

SARIMA Model _ж ^^4^^tM

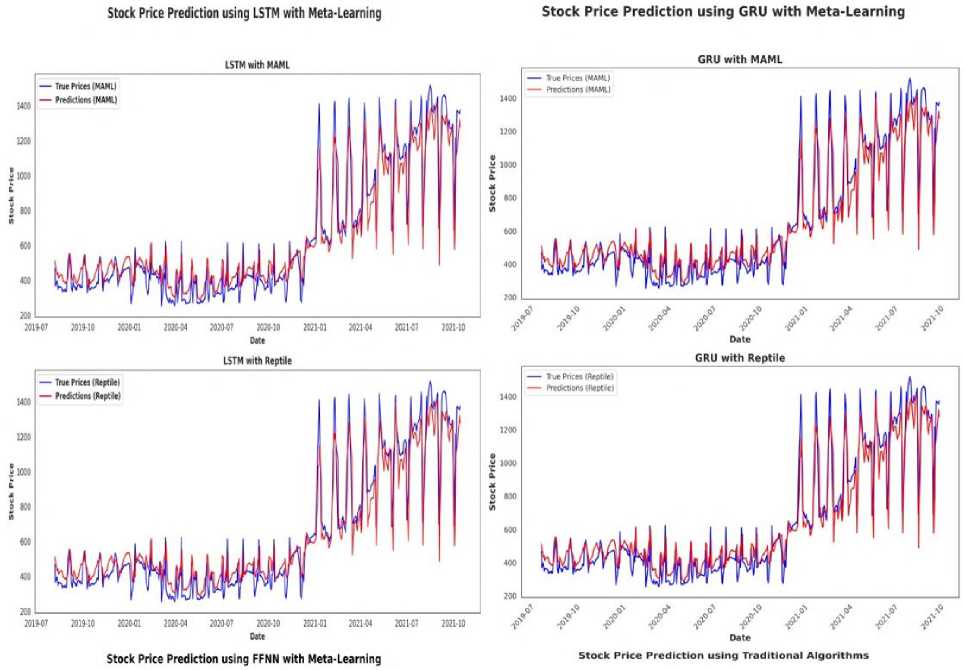

Fig.3. Performance comparison of MAML(First Order) and reptile with different base models on TATASTEEL stock data

Table 3. Performance comparison of MAML(First Order) and reptile with different base models and iterations on GRASIM stock data

|

GRASIM Stock |

Metric |

No of Iterations |

||||||||||

|

10 |

20 |

30 |

40 |

50 |

60 |

70 |

80 |

90 |

100 |

|||

|

LSTM |

MAML |

RMSE |

622 . 94 |

295 . 44 |

316 . 18 |

323 . 42 |

229 . 94 |

178 . 42 |

253 . 17 |

113 . 21 |

169 . 53 |

112.60 |

|

MAE |

543 . 98 |

239 . 36 |

273 . 09 |

283 . 92 |

195 . 44 |

152 . 12 |

223 . 28 |

81 . 55 |

134 . 22 |

80.67 |

||

|

Rˆ2 |

-20 . 32 |

0 . 22 |

0 . 18 |

0 . 59 |

0 . 75 |

0 . 50 |

0 . 90 |

0 . 77 |

0 . 98 |

0.98 |

||

|

Reptile |

RMSE |

111 . 96 |

109 . 29 |

108 . 20 |

106 . 93 |

105 . 38 |

119 . 56 |

104 . 22 |

105 . 00 |

105 . 55 |

112 . 06 |

|

|

MAE |

80 . 47 |

76 . 82 |

76 . 11 |

75 . 55 |

75 . 11 |

93 . 71 |

74 . 68 |

76 . 47 |

77 . 78 |

84 . 93 |

||

|

Rˆ2 |

0 . 90 |

0 . 90 |

0 . 90 |

0 . 91 |

0 . 91 |

0 . 88 |

0 . 91 |

0 . 91 |

0 . 91 |

0 . 90 |

||

|

GRU |

MAML |

RMSE |

355 . 11 |

296 . 57 |

162 . 47 |

142 . 84 |

519 . 06 |

218 . 08 |

117 . 13 |

100.22 |

110 . 97 |

106 . 38 |

|

MAE |

310 . 79 |

262 . 42 |

135 . 44 |

112 . 71 |

466 . 24 |

195 . 22 |

76 . 76 |

64.22 |

75 . 49 |

75 . 14 |

||

|

Rˆ2 |

0 . 02 |

0 . 31 |

0 . 79 |

0 . 84 |

-1 . 08 |

0 . 63 |

0 . 89 |

0.92 |

0 . 98 |

0 . 91 |

||

|

Reptile |

RMSE |

105 . 25 |

109 . 25 |

113 . 00 |

124 . 21 |

129 . 12 |

131 . 60 |

132 . 56 |

129 . 95 |

134 . 24 |

135 . 24 |

|

|

MAE |

75 . 48 |

71 . 95 |

85 . 93 |

97 . 86 |

102 . 75 |

105 . 57 |

106 . 93 |

104 . 98 |

109 . 66 |

109 . 74 |

||

|

Rˆ2 |

0 . 91 |

0 . 90 |

0 . 90 |

0 . 88 |

0 . 87 |

0 . 86 |

0 . 86 |

0 . 86 |

0 . 86 |

0 . 85 |

||

|

FFNN |

MAML |

RMSE |

161 . 31 |

190 . 73 |

179 . 60 |

181 . 08 |

181 . 43 |

181 . 57 |

182 . 33 |

198 . 89 |

246 . 42 |

245 . 19 |

|

MAE |

116 . 91 |

143 . 68 |

140 . 62 |

145 . 84 |

146 . 56 |

146 . 77 |

147 . 91 |

163 . 99 |

192 . 53 |

191 . 71 |

||

|

Rˆ2 |

0 . 79 |

0 . 71 |

0 . 75 |

0 . 74 |

0 . 74 |

0 . 74 |

0 . 74 |

0 . 60 |

0 . 52 |

0 . 53 |

||

|

Reptile |

RMSE |

268 . 98 |

287 . 97 |

293 . 19 |

300 . 21 |

309 . 13 |

319 . 88 |

332 . 65 |

335 . 96 |

335 . 97 |

336 . 01 |

|

|

MAE |

229 . 52 |

247 . 01 |

251 . 78 |

258 . 13 |

266 . 19 |

275 . 95 |

287 . 69 |

298 . 74 |

290 . 75 |

290 . 78 |

||

|

Rˆ2 |

0 . 43 |

0 . 35 |

0 . 33 |

0 . 30 |

0 . 25 |

0 . 20 |

0 . 14 |

0 . 12 |

0 . 12 |

0 . 12 |

||

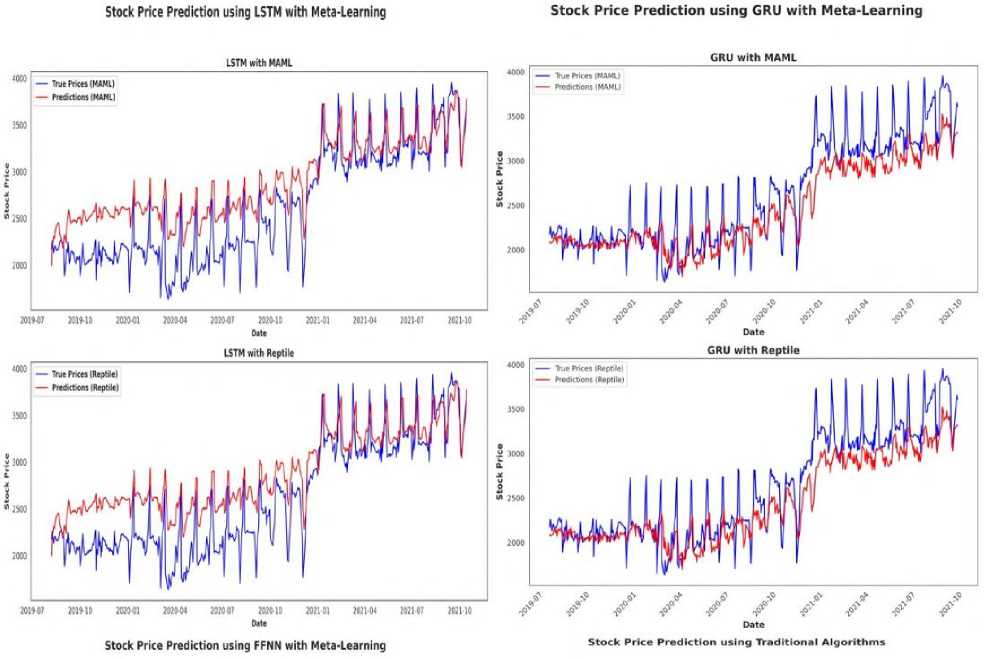

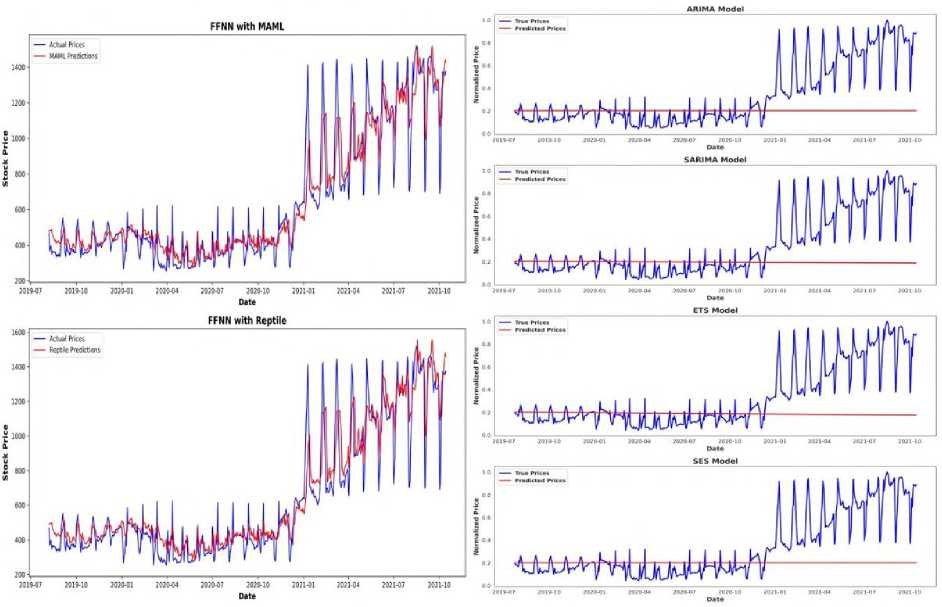

Fig. 4 and Table 3 present the comparative results of MAML(First Order) and Reptile meta-learning algorithms with LSTM, GRU, and FFNN as base learner models for predicting GRASIM stock prices. The visual plots and metrics collectively show the superior learning capabilities of MAML, particularly when used with recurrent models like GRU and LSTM, in capturing the temporal dependencies within financial time series data. LSTM with MAML demonstrating a good improvement in performance with increased iteration counts, achieving the best results at 100 iterations with an RMSE of 112.60, MAE of 80.67, and R² of 0.98. On the other hand, Reptile maintains continuously stable performance across various iterations, but does not able to reach the peak accuracy of MAML. Similarly, GRU with MAML gives excellent predictive performance, reaching at 80 iterations with an RMSE of 100.22, MAE of 64.22, and R² of 0.92, strengthening its ability to model sequential data effectively. Conversely, the model using FFNN as base neural architecture performs poorly with both MAML and Reptile, showing higher error and worse R² values over all the iterations, showing its flaws in handling time-dependent patterns. Traditional methods such as ARIMA, SARIMA, ETS, and SES are also shown in Fig. 4 for baseline comparison but fall short of matching the accuracy and responsiveness of meta learning enhanced deep learning models. These findings suggest that MAML-based meta-learning significantly boosts the adaptability and accuracy of deep models, particularly LSTM and GRU, for dynamic stock forecasting tasks.

Fig.4. Performance comparison of MAML(First Order) and reptile with different base models on GRASIM stock data

Fig.5. Performance comparison of MAML(First Order) and reptile with different base models on DJIAHD stock data

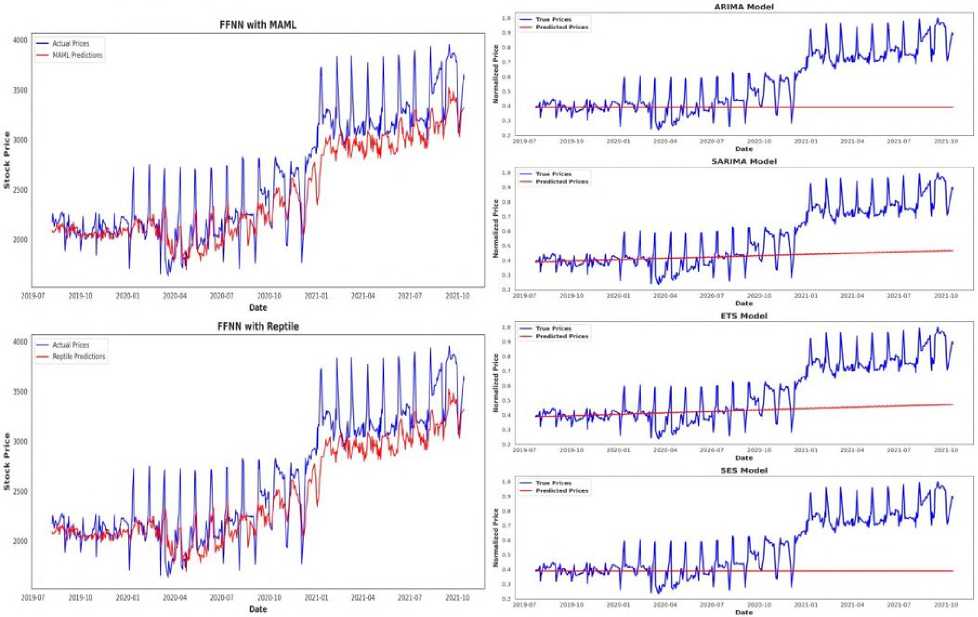

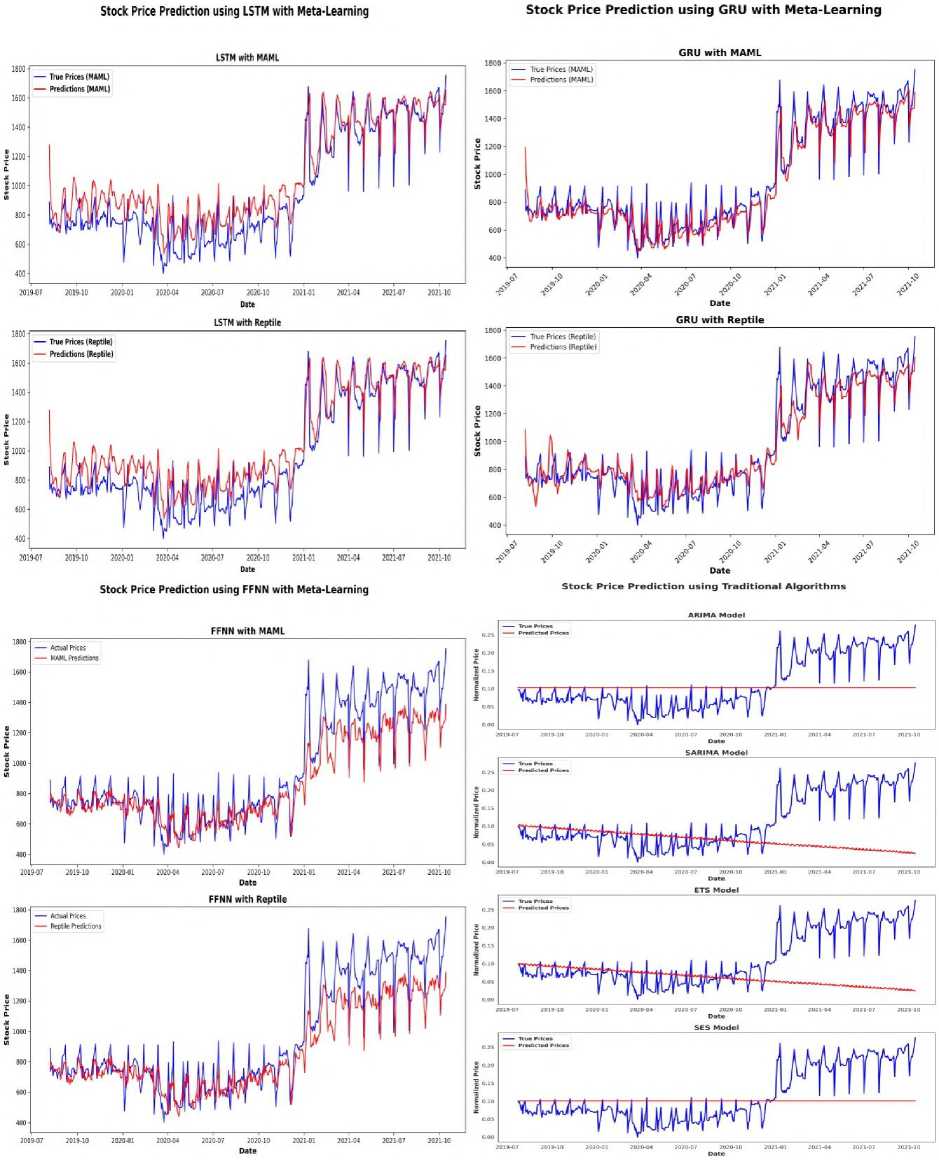

Fig. 5 and Table 4 explain the comparative analysis of MAML and Reptile meta-learning framework used with LSTM, GRU, and FFNN as base models for the prediction of DJIAHD stock dataset. The performance patterns show the notable adaptability of MAML, particularly when combined with LSTM, where the model exhibit very good improvements over successive iterations while reaching peak performance at 100 iterations with RMSE of 278.06, MAE of 184.07, and a high R² of 0.95. Similarly, GRU with MAML algorithm gives strong predictive accuracy at 30 iterations, boasting RMSE of 281.17, MAE of 206.03, and R² of 0.95, though its performance is less stable as compared to LSTM. On the other hand, Reptile shows relatively consistent performance across iteration counts but does not able to reach the best results achieved by MAML. For instance, here reptile with LSTM hovers around RMSE values of 309–394 with R² 0.91, showing reliability but limited amount of improvement. Notably, FFNN performs bad with both meta-learning approaches, particularly with Reptile, where the R² remains around 0.01, indicating poor generalization. Various traditional models like ARIMA, SARIMA, ETS, and SES, plotted in Fig. 5, not adequately capture the market dynamics effectively which shows the superior temporal learning capability of deep learning models, especially when used with meta-learning. Overall, these findings shows that MAML provides significant improvements in learning efficiency and accuracy for stock price forecasting, especially when combined with recurrent architectures base models like LSTM and GRU.

Table 4. Performance comparison of MAML(First Order) and reptile with different base models and iterations on DJIAHD stock data

|

DJIAHD Dataset |

Metric |

No of Iterations |

||||||||||

|

10 |

20 |

30 |

40 |

50 |

60 |

70 |

80 |

90 |

100 |

|||

|

LSTM |

MAML |

RMSE |

2197 . 38 |

1173 . 06 |

1122 . 69 |

609 . 41 |

757 . 18 |

495 . 14 |

1052 . 55 |

458 . 86 |

838 . 02 |

278.06 |

|

MAE |

1888 . 63 |

1038 . 35 |

982 . 19 |

522 . 98 |

653 . 68 |

406 . 62 |

995 . 52 |

387 . 45 |

783 . 38 |

184.07 |

||

|

Rˆ2 |

-1 . 94 |

0 . 16 |

0 . 23 |

0 . 77 |

0 . 65 |

0 . 85 |

0 . 32 |

0 . 87 |

0 . 57 |

0.95 |

||

|

Reptile |

RMSE |

309 . 51 |

394 . 38 |

380 . 66 |

392 . 62 |

380 . 77 |

405 . 84 |

408 . 57 |

396 . 99 |

387 . 63 |

380 . 31 |

|

|

MAE |

238 . 83 |

331 . 33 |

321 . 82 |

335 . 19 |

325 . 47 |

349 . 37 |

351 . 73 |

341 . 08 |

331 . 64 |

324 . 62 |

||

|

Rˆ2 |

0 . 94 |

0 . 90 |

0 . 91 |

0 . 90 |

0 . 91 |

0 . 89 |

0 . 89 |

0 . 90 |

0 . 90 |

0 . 91 |

||

|

GRU |

MAML |

RMSE |

1357 . 56 |

612 . 77 |

281.17 |

1165 . 88 |

286 . 24 |

1028 . 87 |

1007 . 02 |

1051 . 64 |

898 . 07 |

720 . 30 |

|

MAE |

1032 . 72 |

541 . 53 |

206.03 |

1130 . 88 |

225 . 37 |

1005 . 82 |

995 . 85 |

1040 . 99 |

886 . 68 |

699 . 25 |

||

|

Rˆ2 |

-0 . 12 |

0 . 77 |

0.95 |

0 . 17 |

0 . 95 |

0 . 35 |

0 . 38 |

0 . 32 |

0 . 50 |

0 . 68 |

||

|

Reptile |

RMSE |

720 . 33 |

720 . 33 |

720 . 22 |

719 . 91 |

718 . 96 |

717 . 36 |

715 . 25 |

712 . 98 |

736 . 48 |

766 . 76 |

|

|

MAE |

699 . 73 |

700 . 51 |

701 . 77 |

703 . 04 |

703 . 57 |

702 . 99 |

701 . 62 |

699 . 73 |

725 . 42 |

756 . 16 |

||

|

Rˆ2 |

0 . 68 |

0 . 68 |

0 . 68 |

0 . 68 |

0 . 68 |

0 . 68 |

0 . 68 |

0 . 69 |

0 . 66 |

0 . 64 |

||

|

FFNN |

MAML |

RMSE |

864 . 16 |

792 . 92 |

775 . 17 |

774 . 46 |

773 . 86 |

773 . 45 |

774 . 31 |

773 . 71 |

773 . 58 |

772 . 91 |

|

MAE |

657 . 36 |

615 . 16 |

602 . 86 |

602 . 21 |

601 . 66 |

601 . 17 |

600 . 13 |

599 . 61 |

599 . 27 |

598 . 74 |

||

|

Rˆ2 |

0 . 54 |

0 . 61 |

0 . 63 |

0 . 63 |

0 . 63 |

0 . 63 |

0 . 63 |

0 . 63 |

0 . 63 |

0 . 63 |

||

|

Reptile |

RMSE |

1269 . 77 |

1270 . 22 |

1270 . 89 |

1271 . 78 |

1272 . 89 |

1274 . 26 |

1275 . 85 |

1277 . 69 |

1279 . 81 |

1282 . 13 |

|

|

MAE |

1116 . 65 |

1117 . 05 |

1117 . 64 |

1118 . 43 |

1119 . 42 |

1120 . 64 |

1122 . 04 |

1123 . 67 |

1125 . 54 |

1127 . 60 |

||

|

Rˆ2 |

0 . 01 |

0 . 01 |

0 . 01 |

0 . 01 |

0 . 01 |

0 . 01 |

0 . 00 |

0 . 00 |

0 . 00 |

0 . 00 |

||

5. Conclusions

In this paper we investigated the potential of meta-learning algorithms, to be specific MAML(First Order) and Reptile algorithms, for time series forecasting problem in financial domain. Through a comprehensive evaluation using various real-world company stocks like TCS, Tata Steel, Grasim, and DJIAHD, we demonstrated(from visualization) that meta-learning approaches consistently perform better than traditional forecasting models used, especially in dynamic and volatile environments. Here MAML was proven to be effective in catching stable trends and adapting quickly to minor variation. On the other hand, reptile showed enhanced generalization as well as robustness across various stocks. While helpful in some situations, various traditional models such as ARIMA, SARIMA, etc. showed limits with regard to performance and flexibility across a variety of financial time series stock datasets. The comparative analysis through visual graphs further explains the pros of meta-learning methods in forecasting accuracy and learning efficiency. Overall, this strategic investigation validates the use of MAML and Reptile as effective alternative when compared against conventional time series prediction methods. Additionally, it creates new pathways for robust, adaptive, and task-efficient time series modeling in financial markets.

Although the efficiency of meta-learning methods like MAML and Reptile for financial time series forecasting is the primary focus of the current work done, there are still a numerous other areas that might be investigated and studied in the future. One of the potential directions is the study of various other meta-learning algorithms and optimization approaches to try and further increase adaptability as well as convergence speed. Using specific domain expertise or external factors like macroeconomic indicators, sentiment analysis or news-based signals may increase forecasting accuracy, especially during high-volatility conditions. Furthermore, broadening the current framework to multi-step forecasting and testing across a wider range of asset classes, including cryptocurrencies, commodities and data-scarce emerging markets could validate the applicability of these methods and their potential to support robust portfolio diversification. Finally, real-time implementation of meta-learned models in a live trading environment could give us valuable insights into their practical feasibility and impact on making correct decisions in financial markets.

Author Contributions Statement

Pratik Zinjad– Conceptualization, Methodology, Implementation, Data Curation, and Writing – Drafted the initial manuscript.

Tushar Ghorpade– Supervision, Formal Analysis, Validation, and Writing – Review and Editing.

Vanita Mane– Supervision, Performance Evaluation, and Writing – Review and Editing.

All authors have read and agreed to the published version of the manuscript.

Conflict of Interest Statement

The authors declare no conflicts of interest.

Funding Declaration

This research received no external funding.

Data Availability Statement

This study analyzed publicly available datasets (Nifty Fifty and DJIAHD). The datasets can be found here: “”, ", accessed on “20-05-2024”.

Ethical Declarations

The authors declare that no human subjects or animals were involved in this study.

Acknowledgments

We sincerely thank the experts for their professional evaluation and valuable recommendations, which have contributed to improving the quality of the experiment and the reliability of its results.

Declaration of Generative AI in Scholarly Writing

During the preparation of this work, the authors used ChatGPT in order to improve readability and grammar. After using this tool, the authors reviewed and edited the content as needed and take full responsibility for the content of the publication.

Abbreviations

The following abbreviations are used in this manuscript:

MAML - Model-Agnostic Meta-Learning

FOMAML - First-Order Model-Agnostic Meta-Learning

LSTM - Long Short-Term Memory

GRU - Gated Recurrent Unit

FFNN - Feed Forward Neural Network

RMSE - Root Mean Square Error

MAE - Mean Absolute Error

ARIMA - Autoregressive Integrated Moving Average

SARIMA - Seasonal Autoregressive Integrated Moving Average

AI - Artificial Intelligence

DL - Deep Learning