Restaurant management cost price as a key competence of its management

Author: Habibullo Ziyavitdinov

Journal: Экономика и социум @ekonomika-socium

Section: Основной раздел

Article in issue: 9 (88), 2021.

Free access

The purpose of the study is to analyze the business processes carried out in the production of a public catering enterprise associated with the purchase of raw materials, the production of semi-finished products, taking into account the waste ratio, which is reflected in the cost of production, the formation of meals. A method is given for preserving the "taste of a restaurant", which depends on the availability of the most relevant recipes in production, which should be law in production when preparing dishes, since their observance determines the quality of production.

Catering, cost of raw materials, profits, motivation, meal formation, suppliers, procurement activities, cost control

Short address: https://sciup.org/140254926

IDR: 140254926

Стоимость управления рестораном как ключевая компетенция его управления

Анализ бизнес-процессов, осуществляемых на производстве предприятия общественного питания, связанных с закупкой сырья, производством полуфабрикатов, учетом коэффициента отходов, что отражается на себестоимости продукции, формированием блюд. Дана методика по сохранению «вкуса ресторана», что зависит от наличия на производстве максимально актуальных рецептов, которые должны быть законом на производстве при приготовлении блюд, так как их соблюдение определяет качество работы производства.

Text of the scientific article Restaurant management cost price as a key competence of its management

Currently, the automation of all business processes is intensifying and the digitalization of paper workflow is taking place. Economic and managerial decisions cannot be made without involvement in kitchen management, which is centered on improving production costs. One of the leading methods in this aspect is “Care Cost”, which literally means “save the cost”. The main essence of this technique is a systematic approach to managing the cost indicator in a restaurant. This indicator should be effective and controllable, amenable to influence from the management of the enterprise, as well as motivate employees to achieve the desired result when working with raw materials in the process of processing. This is very important for the functioning of almost any enterprise.

Control over the indicator of the cost of production is important, since it makes up 1/3 of all expenses of the enterprise and thus directly affects the profit of the activity.

For the activities of a catering enterprise, three key concepts are relevant -income, expenses and profit, which is the meaning of the activities of any commercial enterprise. Profit is what remains after income received and expenses incurred, which include taxes, rent of premises, salaries of employees, cost of raw materials, business expenses, commercial services and communications, office expenses, transportation costs, advertising and marketing, technical support and repairs, banking services, other (unforeseen) expenses. Among all these items, the prime cost of raw materials stands out, which can vary from 25 to 40% depending on the concept of the restaurant, that is, on the cost of the main raw materials, the specifics of accounting. On average, this is approximately 30-35%. Therefore, it is very important:

-

1. Not to miss a single mechanism of influence on the cost indicator;

-

2. Use a data mining technique, namely:

-

• prescription cost management;

-

• activation of the purchase cost;

-

• management of the cost of demand;

-

• management of the cost of commodity balances;

-

• launching techniques for effective cost regulation; - inclusion of an economic approach to cost management. Such a broad approach leads to optimization of the cost indicator by 2-4%.

-

3. To activate personnel for the result - to reduce the costs of the enterprise, and specifically the cost of working with raw materials. Among the key tasks when working with raw materials supplied to the production of the enterprise can be noted:

-

- safety - maximally closed refrigerators, chambers, containers for bulk products, preventing theft;

-

- maintenance of the required temperature regimes of refrigerators and freezers (chambers, chests): constant monitoring of the health of the equipment to prevent damage and write-off in large volumes;

-

- sanitation - maintaining constant cleanliness in warehouses (fighting flies, cockroaches, rodents), excluding spoilage and write-offs;

-

- Compliance with the rules "first in - first out": timely use of products with limited shelf life;

-

- mandatory correct labeling of semi-finished products: exclusion of damage and write-offs. After the receipt of products for production, production processes begin directly. When fulfilling which, the personnel must comply with the following rules; - understanding of the processes occurring with the product during cutting, storage, primary and thermal processing, because ignorance of these technological fundamentals can have a catastrophic effect on the activities of the enterprise, especially those that affect the safety of products;

-

- control and fixation of volumes / outputs of all ingredients of a dish or semi-finished products.

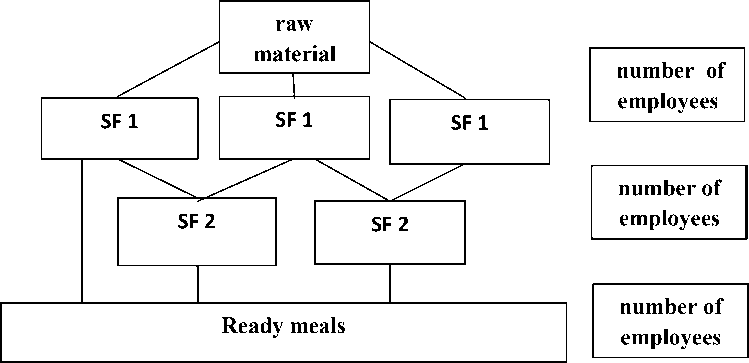

It is impossible to deal with the management and improvement of the cost indicator in a situation of errors in production accounting (PU), especially in terms of controlling the percentage of waste. For this purpose, at least once a quarter or at least six months, conduct an audit of the execution of recipes, that is, prepare according to them within a month and make sure that they correspond to what was agreed on at the tasting. Technologists, chefs, senior bartenders, and a manager should be involved in the audit and updating of recipes. For convenience, you can create a recipe audit schedule (5-6 pcs per day). It is necessary to start the audit with semi-finished products. This work will help preserve the "taste of the restaurant", that is, the consistency of the taste characteristics of the dishes sold on the menu, regardless of the working shift on that day. This can be achieved if the production has the most relevant recipes that do not depend on the care of the chef or key chef. The recipe must be created according to the manufacturing processes, for example, a dish is prepared sequentially from different semi-finished products, this is exactly how you need to collect the recipe into production accounting, as shown in Figure 1. This approach solves several problems at once:

-

1. Recipe is the source for the stationary map;

-

2. Employees are trained using stationary cards;

-

3. Control of the cooking process is carried out using stationary cards.

In order to verify the quality of the restaurant with the cost, you need to start with a billet departments involved in the preparation of semi-finished products for a particular meal.

warehouse

Figure 1 - formation meals

Stationary cards must also be issued for semi-finished products. In order to check the correctness of the technology of their preparation, it is necessary to compare the data - the curtains of the actual semi-finished product with the data in the recipe and the stationary card. It is clear that everything must match. Often there are situations when the real weight is one, in the stationary map there is another, and in the recipe - the third. This indicates that:

-

- stationary cards are fiction, they are not used either as a training document, or as a document for control; - none of the management delves into these cards;

-

- a recipe is not a law, at the enterprise they prepare as they remember and how they want. In such a situation, it is impossible to manage the cost. It needs to be fixed first. Production accounting should reflect the actual picture at the enterprise: - correct and error-free recording of the necessary information in the appropriate forms; - drawing up an act of elaboration of a dish or semi-finished product;

-

- drawing up an application for the creation of a technological map. The restaurant management must constantly and in detail monitor each of these stages. A separate business process in any restaurant is a study, which is associated with:

-

- the planned introduction of new dishes in the menu of the enterprise;

-

- constant study of raw materials, semi-finished products, dishes. The result of each study should confirm the correctness of existing (or newly created) technological maps or lead to their corrections to obtain the most objective data when preparing the corresponding reporting. If recipes with a high cost price are identified, then it is necessary first of all to make decisions on the recipes of this group, namely:

-

1. Refuse these dishes if they sell poorly;

-

2. Discuss the recipe with the chef: is it possible to lighten it, replace raw materials;

-

3. Give a task for the development of a group of recipes with an unsuccessful cost price: if the cost price in the group is currently 35%, then this group should be updated with the help of dishes with a cost price much lower.

The double ABC analysis is very helpful in working on the efficiency of the cost price of formulations. It is necessary to start by working out the "CC" group, which is characterized by poor (high) cost and low sales. The AC group also requires attention, where A is an indicator of excellent sales, C is a high cost price, that is, these dishes are sold well, but their cost price is poor. It is on these dishes that you need to make management decisions. When working with raw materials when preparing dishes, it is necessary to fulfill the following series of requirements, for the fulfillment of which the manager, chef, technologist are responsible:

-

- control over compliance by cooks with the requirements for cooking dishes and semi-finished products according to technological charts;

-

- control over compliance by cooks with the requirements for the return of dishes (exit of a dish on a plate) according to technological charts;

-

- control over compliance by cooks with established requirements / standards for the use and processing of raw materials, especially meat, fish, fruits (freshly squeezed juices in the bar), vegetables;

-

- control of the stability / constancy of the percentage of waste / processing of raw materials supplied to the enterprise established during development and entered into the accounting system (development act);

-

- timely introduction of necessary changes into the accounting system. Cost management is related to procurement activities. The supply department of a catering company that deals with purchases has a significant impact on a restaurant's bottom line. Purchases account for about 30% of the total turnover. They are associated not only with the product itself, but also with consumables. In order for the cost price and cost fund of the enterprise to be under control, it is important to manage the work of the purchasing department.

There are a lot of offers on the market now. Therefore, in order to choose the right suppliers of products for the enterprise, it is necessary to take into account the specifics of the business, namely:

-

- the concept: the specifics of the kitchen, bar;

-

- logistics: location, distance between specific enterprises (the specifics of the entrance, transport);

-

- accounting: taxation, possible and desired deferred payment;

-

- the presence or absence of warehouse, production facilities and their area;

-

- the possibility of designing additional shops in production (vegetable shop, confectionery, etc.);

-

- the volume of purchases per month (currently, in six months, in a year).

After collecting information regarding the main factors, it is necessary to conduct a market analysis in accordance with the requirements of the catering company and create a list of potential suppliers. Raw materials from suppliers must meet the requirements and requests of the enterprise. To do this, it is necessary to draw up a list of approved products (LAP) with all the necessary data. For restaurants, quality is not only organoleptic and shelf life, but also the waste rate. For the items of raw materials for which this indicator is important, the waste rate should be recorded as a task for the purchase.

When purchasing, it is necessary to take into account that the price changes depending on the change in the coefficient of waste for raw materials. The supplier should be informed about this in advance - either the price changes or the raw materials are returned to the supplier. This is especially true for expensive products, raw materials with a floating waste rate or unclear inventory results.

Another step in protecting quality is the procedure for processing raw materials, taking into account the norms for the coefficient of waste, quality requirements. It is necessary to draw up acts of development and appoint a responsible person who will analyze the data and make decisions. The supplier must understand that it is important to comply with the sanitary rules of delivery, storage conditions for raw materials, and ensure food safety during transportation. It is important that from the side of the supplier there is an employee authorized to solve both price issues and related to the possibility of providing additional preferences (discounts, deferred payment, price fixing, marketing support). In case of violation of the rules of timeliness of deliveries, order volumes and contractual purchase prices, penalties are imposed on the supplier. Since there is a so-called title raw material, without which it is impossible to reproduce the company's key meal.

Conclusion. In the production of a catering enterprise, there are no trifles, as they say, everything big is made up of trifles. Each number is important for running a business and maintaining production and labor discipline in the team. Ensuring the receipt of correct data for accounting in the production of the enterprise simultaneously solves the problems of optimizing costs and reducing costs, especially under the item "Cost of raw materials". This work leads to an increase in the professional level of personnel, decency and honesty in the performance of their duties.

References Restaurant management cost price as a key competence of its management

- Product quality management based on HACCP principles in trade and public catering enterprises.G.A. Khamatgaleeva - Moscow: RUSAYNS, 2019 .-- 174 p.

- Хабибулло, З. (2021). OPTIMIZATION OF RESTAURANT SERVICE STAFF BY THE FULL TIME EQUIVALENT METHOD . ЦЕНТР НАУЧНЫХ ПУБЛИКАЦИЙ (buxdu.Uz), 6(6). извлечено от http://journal.buxdu.uz/index.php/journals_buxdu/article/view/3261

- Ziyavitdinov H.H. Инновационный проект “Smart restaurant” в ресторанном сервисе // Вестник науки и образования. № 6(109), 2021. P. 25.

- Khamidovich, Z. K. (2021). Pandemic and Trends in the Restaurant Business in 2021. CENTRAL ASIAN JOURNAL OF INNOVATIONS ON TOURISM MANAGEMENT AND FINANCE, 2(6), 54-61. https://doi.org/10.47494/cajitmf.v2i6.129

- Зиявитдинов Х.Х. ОСОБЕННОСТИ ИННОВАЦИОННОГО ПРОЕКТА “SMART RESTAURANT” В РЕСТОРАННОМ СЕРВИСЕ // Academy. № 6(69), 2021 - С