The accounting archive of Fiorentine bank of uzzano (1363–1386) in saint-Petersburg

in saint-Petersburg")

Author: Малькова Татьяна Николаевна

Journal: Общество. Среда. Развитие (Terra Humana) @terra-humana

Section: История и современность

Article in issue: 2 (27), 2013.

Free access

Архив банка Уццано (Uzzano) представляет колоссальную ценность, он востребован для научных исследований по истории бухгалтерского учета и финансового анализа, в связи с чем актуальны его современное издание и бухгалтерский анализ. Статья была опубликована в журнале «Rivista di contabilitб e Cultura Aziendale» (2011, № 2) и посвящалась году Италии в России (2011). Статья публикуется вновь (c некоторыми сокращениями и поправками) для популяризации уникального итальянского бухгалтерского архива (1363–1386) – единственного в России.

Флорентийский банк uzzano

Short address: https://sciup.org/14031555

IDR: 14031555 | UDC: 336

Text of the scientific article The accounting archive of Fiorentine bank of uzzano (1363–1386) in saint-Petersburg

The company of Uzzano was founded in 50s o fi t t (

Terra Humana

Figure 1. Banker Niccolo da Uzzano [3].

The Uzzano’s archive was founded in Saint-Petersburg and published by the academician Rutenburg V.I. (1911–1988) in 1965 [3], but it has presentation and publication drawbacks, it is not translated into modern language, there are omitted documents; it is not provided with reliable accounting comments; the bank’ documents are referred to as trade. Accounting analysis effort was made by the author of this t of the documents (Fig. t the exhibition in the 2012).

nts had watermarks (not t up (sometimes with a es. The documents have timeters lengthwise and edgewise): 12 x 30 (1363), 15 x 23 (1377 and 1375, 1386). Large-sized d in double or four.

ake an absolutely profes-y are ranked on the text nts (to the right). Blank xt of the item and the es. In the documents to he items there are signs , [/] and cancellation by were designated shortly d – dinari, l – lire) and rrencies in totals were mon monetary measure s a fior ). Alignment for i – align left, for ciphers figures (1363 and Arab (ciphers) were used. In there are used only ci-lly took priority due to .

numbers of ledgers had ). In references the se- ublished again (with some r hive (1363–1386) – of sole

i

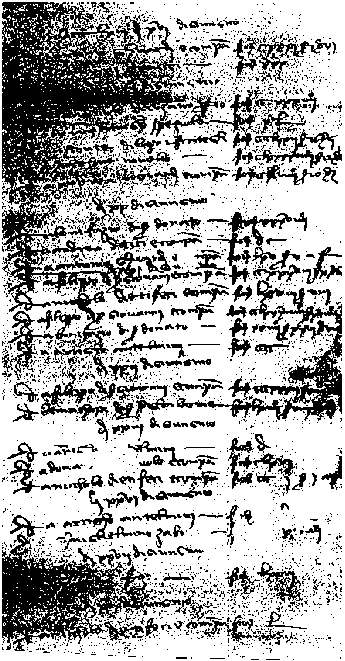

Figure 2. List of debtors at June 16, 1363 [3].

Figure 3. List of debtors and creditors at August 31, ‘ 1375 [3]. ‘

quence was observed, which confirms system accounting. The most informative documents are the ones from 1370-1377.

Research of these extraordinary documents produced an incredibly emotional experience for the author of the article: writers held them in their hands 650 years ago, it was they who turned over accounting books and made records from them, trying to miss nothing, and then checked them repeatedly; it was they who opened secret books and at one time saw in person anonymous debtors and creditors, screened themselves behind codes; they took care of their family business and kept accounting. Such emotions are only left by original sources.

The Accounting Archive of Fiorentine Bank of Uzzano 1363 . The document from 1363 is the earliest in the archive. Records are made on both sides of each list (head and back) and cover the period of 02–30.06.1363. The copybook sequentially includes the following – table 1.

The target of research is pages 3–5, 13–15, 22–29, 31. With a view to research we (M.T.) united them according to types of records and totals (conversion courses: f 1 = s 62; s 1 = d 12;/ 1 =5 20).

-

(1) List of cash in hand. Its name is - Questo e I’chonto che mi lascio Angniolo da Uzano (It is a count, which Angniolo da Uzano has left for me).

the list is – MCCCLXIII dм 2 di ne 2, 1363). The list recorded the results of cash account inventory and includes ranked on the items list of different types of coins ( ducati , gienovini , fiorini , libbri – grossi и quatrini ). Overall total can be designated as f4 323.

-

(2) The lists of debtors includes a list of names (of individuals and companies) ranked on dates and items, monetary measurer (fiorini), sums on types of coins (f, s, d). The title of the list is missing, but it is the list of debtors, that is clear from the term «debit» (da, from dare). Overall total is missing, it can be designated as f9 573. Format of the list of debtors has the following view (extract and Fig. 2) – table 2.

-

(3) The lists of creditors contain a list of names (of individuals and companies) ranked by dates and items, monetary measurer (fiorini), sums on types of coins (f, s, d). The title of the

Общество

list is missing, but it is the list of creditors, which is clear from the term “credit” (a or ad, from avere). Totals are shown only in two cases.

Overall total is missing, it can be designated as f7 441. Format of the list of creditors has the following view (extract) – table 3.

Table 1

|

(Pages) |

|

|

1 |

Fragmentarily extant ciphers |

|

2 |

Fragmentarily extant text and Latin figures – crossed |

|

3 |

List of cash in hand |

|

4–5 |

Lists of debtors with the term dare , in short da |

|

6–12 |

Seven blank pages (evidently, a reserve for six months up to the end of the year) |

|

13–15 |

Lists of creditors with the term avere, in short a (or ad before a vowel of a name) |

|

16–21 |

Six blank pages (evidently, a reserve for six months up to the end of the year) |

|

22–26 |

Lists of other transactions with terms dare, avere, entrata, uscita and reference to the page number (carta) of the ledger – crossed pp. 24–26 |

|

27–29 |

Lists of notes – receivable (per lettera mando) , payable (per lettera mandamo) and paid (per lettera avemo) – crossed |

|

30 |

Blank page |

|

31 |

Lists of transactions with term dare and reference to the page number (carta) of the ledger – crossed |

|

32 |

Fragmentarily extant Latin figures – crossed |

Table 2

|

MCCCLXIII di XVI di giungnio |

|||

|

da |

Antonio Ghuardi e comp |

fior |

CXXXI s I d VI |

|

da |

Giobanni di Nucci |

fior |

XXX |

|

di XVIIII di giungnio |

|||

|

da |

Angniolo da Uzano proprio |

fior |

CCXXXIIII |

|

da |

Giovanni di Tingho speziale |

fior |

XL |

|

da |

Visconte di Lapo e frategli |

fior |

CCCCLXXII s 26 d 5 |

|

da |

Michelone Novello |

fior |

CLXXXVIIII s 22 d 2 |

|

da |

Andrea Riccardi e comp |

fior |

CCXLVIIII s 20 d 2 |

|

di XXII di giungnio |

|||

|

da |

Filippo di ser Giovanni e comp |

fior |

CCCXXXII s XIIII d VI |

|

da |

Beninchasa di ser Piglialarme |

fior |

LXIIII s VIII d IIII |

|

di XXX di giungnio |

|||

|

da |

Niccholo Dietifeci e comp |

fior |

L |

Terra Humana

Table 3

|

MCCCLXIII di XII di giungnio |

|||

|

a |

Michelone Novello |

fior |

VI |

|

a |

Michelone ditto |

fior |

CC |

|

di XIII di giungnio |

|||

|

a |

Michelone ditto |

fior |

VII |

|

a |

Lui medesimo |

fior |

XX |

|

a |

Lui medesimo |

fior |

XL |

|

a |

Michelone Novello |

fior |

IIII |

|

a |

Ser Durante da Modigliana |

fior |

XII |

|

a |

Uberto Benvenuti |

fior |

X |

|

ad |

Antoni Ghuardi e comp |

fior |

CCCLXXX s 7 d 6 |

|

di XX di giungnio |

|||

|

a |

Ghalasso da Uzano |

fior |

DI s VII d III |

|

Somma |

fior |

MIIDCCCCXXXIII s XIIII d VIII a f |

|

-

(4) Lists of other transactions contain less formalized representation. Their generalization has the following view (for the sake of convenience the sums are separated by commas) – table 4.

Let’s generalize all amounts received on June 30, 1363 in a modern view – table 5.

It is pertinent to note cautious attitude of the banker to the notes, which appeared in petty cash (рiccolo) and in overweight of notes payable rather than notes receivable. It appears that cash in hand and data on the debtors’ and creditors’ lists provided Angniolo da Uzzano essential information, that’s why records on notes are crossed.

Copybook from 1363 was not the current ledger. It only contained selections from the latter. References to other ledgers are missing, that’s why it is permissible to conclude of using a single ledger Libro grande (compare with direct reference to separate ledgers – Red book and Copybook in 1364). But what did the lists of debtors and creditors contain – selections of turnovers or cash balances? In our opinion, the lists generalized account balances, as the sums and records are clearly insufficient for turnovers of a large company. Besides, copying of turnovers was not worth-while, if current accounting of transactions was made. But it had to be made in accordance with the requirements of commune authorities. The basis of debtors’ and creditors’ lists was their current accounts. But why did Angniolo da Uzzano compose the lists? There could be two goals. One of them was generalization of debts; the other – evaluation of the financial position of the company, that seems the most likely as for generalization of debts the list of cash is not required.

According to available data we can designate liquidity and quick ratios on June 30, 1363 – table 6.

It is not known exactly, whether Аngniolo da Uzzano used the ratios of financial position, but circumstances for that existed. It is known that the previous bank of Uzzano faulted in 1341 [3, p. 25]. There was the personal interest in financial analysis of liquidity of bank.

When calculating liquidity without other debtors and creditors, we obtain almost the same data as at June 30, 1363 – table 7.

Table 4

|

(Pages) |

Debit |

(Sum) |

Credit |

(Sum) |

|

22 |

Name. Expense items: equipment, duties, services. Expense record – page 175 (Рosti a uscita – carta 175) |

50,3,2 |

||

|

23 |

Name. Sum. Names. Sums. Name. f 150 and f 40. Received in cash (contanti) |

14,4,0 5,41,0 190,0,0 |

Name. Sum. Receipt record – page 16 (Рosti a entrata – carta 16) |

300,0,0 |

|

24–26 |

Named. Sums. Expense record – page 174 (Рosti a uscita – carta 174) |

32,57,4 |

Name. Sum. Receipt record – page 27 (Рosti a entrata – carta 27) |

234,0,0 |

|

27–29 |

Names. Sums (less avemo) |

1,43,0 |

Names. Sums |

7,50,0 |

|

31–32 |

Names. Sums |

689,45,0 |

||

|

Total other debtors |

981,26,6 |

Total other creditors |

541,50,0 |

Table 5

|

Cash |

4 323 |

Creditors |

7 441 |

|

Debtors |

9 573 |

Other creditors |

541 |

|

Other debtors |

981 |

Capital (assets less creditors) |

6 895 |

|

14 877 |

14 877 |

Table 6

|

Liquidity ratio |

(4 323 + 9 573 + 981) : (7 441 + 541) |

1, 9 times |

|

Quick ratio |

(4 323) : (7 441 + 541) |

0, 5 times |

|

Table 7 |

||

|

Liquidity ratio |

(4 323 + 9 573) : 7 441 |

1, 9 times |

|

Quick ratio |

(4 323) : 7 441 |

0, 6 times |

Общество

Last time the banker struck a balance of their family business on the threshold of his dead (on 27.06.1363 the expenses on sugar and capons were recorded due to illness of Angniolo da Uzzano in amount of f2, s15).

It is not an exclusion that in 1363, the capital also could be designated, at least an information basis for that existed (the term capitale was clearly used in a later document from 1370). It is known that the authorities of the commune checked up accounting books and called on companies pay profit taxes into the town budget. In response to that the companies began to keep secret books (segreto libri) for records of contracts of company foundation, fee into company, owners’ profit (capital), employees’ salaries, anonymous debtors and creditors.

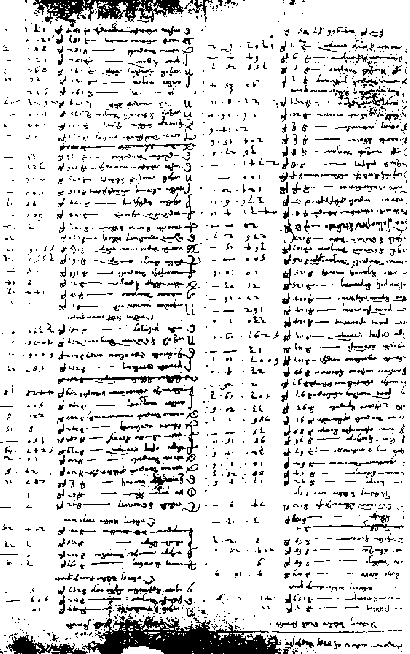

The Accounting Archive of Fiorentine Bank of Uzzano 1364. Accounting documents from 1364 has the name Ragione veduta (Calculation made) with designation of a period. Externally they are three separate sheets, folded four times with records on both front and back sides. They cover the period 08.03–29.12.1364 with discrete separation on more short periods. The terms “debit” and “credit” were not used, as the lists are named Debtors and Creditors . Clear stereotype of the lists shows a higher professional level of a new owner Ghaleazzo da Uzzano or a hired accountant.

Period discretion of generalization approves the conclusion on possibility of usage of accounting data for analysis of financial position made by us earlier. But the documents from 1364 are also of interest from the point of view of standardization of accounting books. It is this feature which positively distinguishes them from the documents from 1363 (the selection for November 30 – December 29, 1364 is instanced) – table 8.

Obviously, there were two ledgers – Red book and Copybook (so-called White , First white , Copybook ).

The Accounting Archive of Fiorentine Bank of Uzzano 1370– 1 377 . Accounting documents from 1370 and 1375 contain lists of debtors and creditors, their generalization; from 1377 – receipt and expense lists, cash list; without date – textile and expense items of the store; from (13)70 – debtors’ and creditors’ lists, including anonymous. In the document from (13)70 of the XIV century there is a reference to loss ( mancha chapitale ), and the same sum exists in the document from 1377. It is strangely enough that this document is kept together with ones from 1386: That is why the sequence of the documents must be the following – table 9.

The document from August 31, 1375 is extremely interesting by the general totals (the items – in fragment, the totals – in full, Fig. 2) – table 10.

Data generalization on August 31, 1375: debtors 60 054 (24 966 + 35 088), сash 3 254, total 63 308; creditors 56 819 (55 115 + 1 703); capital on May 1, 1375 (but the term «capital» is

Terra Humana

Table 8

|

(Ledger) |

(Name and Company) |

(Carta) |

(Sum) |

|||||||

|

Debtors |

libro Rosso |

Ghaleasso da Uzano Ghaleasso da Uzano е сhompagni 37 balle di lana Andrea Ricciardi e сhompagni |

c c c c |

3 56 57 75 |

f f f f |

7637 234 2003 10294 |

– 15 – 8 |

11 7 11 3 |

||

|

Debtors |

quaderno bi-ancho |

Manetto di messere Geri Franciesco di Vanni Rosellino Ghuccini al quaderno |

c cc |

4 72 – |

f f f |

30 500 2 |

s s |

13 – 10 |

d |

9 – |

|

Creditors |

libro Rosso |

Ghaleasso da Uzano е chomp. Ghaleasso da Uzano Andrea Ricciardi e сhompagni Filippo (далее стерто) Bartolomeo Bonetti |

cc c с c |

162 163 209 213 194 |

f f f f f |

7 981 1000 620 10844 – |

19 – – 6 3 |

0 – 9 10 |

||

|

Creditors |

quaderno bi-ancho primo |

Mazzetto di Gherardino Messere Amerigho Ciati Messere Nicholo da Uzano |

c с c |

122 152 220 |

f f f |

5 3 68 |

0 9 23 |

0 2 9 |

||

|

Debtors |

quaderno |

Manаtto di messere Gieri Uberto Benvenuti |

c с |

4 228 |

f f |

30 3 |

13 23 |

9 – |

||

|

Creditors |

libro Rosso |

Ghaleasso da Uzano е chomp. Ghaleasso da Uzano Bartolomeo Bonetti |

c с c |

162 163 224 |

f f f |

7981 1000 216 |

19 2–0 |

0 – 7 |

||

|

Creditors |

quaderno |

Michele di Vani Messere Amerigho Ciati |

c с |

72 152 |

f f |

72 3 |

– 9 |

d 2 |

||

Here we have a treatment to acknowledgment of profit as difference of net assets by the end and the beginning of the period without keeping Profit and Loss account. Such treatment was called later a simple double entry. Balance sheet did not have standardized presentation, but it was used in practice, and firstly formed in content and then – in form. Liquidity of bank on August 31, 1375 – table 12.

The receipt and expense list for October 1377 had interrelation with the cash in hand list from November 11, 1377 as it contained comparison of accounting and inventory cash balances – table 13.

The estimated difference 8,5,3 (66 283,5,9 – 66 275,0,6) is designated as deficiency of capital (mancha chapitale). At last we have the term for designation of capital, missing on default in the abovementioned document from 31.08.1375. The term «capital» (brought in business and earned profit) in archive of Uz-zano existed in 1377, that is testified directly and in writing. Cash in hand inventory list is interrelated with this document – table 14.

If understood as there was debtors’ cash in favour of creditors in the amount f30 s19, it is born in why in the previous document f1 609 и f1 639 were designated. The reasons of accounting mismatching were the object of an accountant consideration of the Uzzano’s company.

The similar documents with some date uncertainty (70-th of the XIV century) are of special interest as they contain codes of anonymous debtors (they are 27, including one from the Uzzano’s family) and creditors (they are 4). There were already on August 31, 1375. That’s why the date was uncertaint. These are just the extractions from the secret accounting books (segreto libri) for September 1–30, 70 (references at pages: L, RRR, VVV, XXX, ttt) – table 15:

Net profit (netto ad avanzo) with the distribution of months and inclusion of loss f 8,5,3 for October is a direct argument of financial results and capital categories usage. Balance sheet and liquidity ratios as on September 30, 1370 – table 16.

The Liquidity of Uzzano’ bank fallen steadily.

The Accounting Archive of Fiorentine Bank of Uzzano 1386. The document from

Общество

|

(Ledger) |

(Name and Company) |

(Carta) |

(Sum) |

|||||||

|

Debtors |

libro giallosecondo |

Lorenzo Lassolini Il commune di Firenze |

с с |

5 159 |

f f |

10 141 |

∙ ∙ |

1 |

∙ |

8 |

|

libro biancho quinto |

Messere Lucha de Totto |

c |

49 |

f |

4 |

∙ |

16 |

∙ |

9 |

|

|

libro nero terzo |

Ghabriello e Girolamo Arighi |

c |

107 |

f |

6007 |

∙ |

10 |

∙ |

1 |

|

|

Filippo Astai e compagni |

c |

113 |

f |

5297 |

∙ |

19 |

∙ |

1 |

||

|

Antonio d’Angnolo da Uzano proprio |

c |

126 |

f |

500 |

– |

– |

||||

|

Simone di Renzo e compagni |

c |

11 |

f |

1303 |

∙ |

6 |

∙ |

2 |

||

|

Somma f 24966 s 7 d 5 in f |

||||||||||

|

Creditors |

libro giallo secondo |

Ghaleasso da Uzano |

c |

312 |

f |

509 |

– |

4 |

||

|

libro biancho quinto |

Rinieri d’Acciolini |

c |

193 |

f |

3 |

∙ |

23 |

∙ |

3 |

|

|

Somma f 55115 s 27 d 4 in f |

||||||||||

|

Debtors more |

libro rancio quarto |

Filippo Astai e compagni |

c |

14 |

f |

541 |

∙ |

2 |

∙ |

– |

|

Somma f 35087 s 17 d 9 a f |

||||||||||

|

E nella faccia de sotto f 24966 s 7 d 3 a f |

||||||||||

|

Somma tutti debitori f 60053 s 15 d 2 a f |

||||||||||

|

E in contanti f 3254 s 18 – a f |

||||||||||

|

Somma tutto f 63308 s 14 d 2 a fior |

||||||||||

|

Creditors more |

Orange fourth book (libro rancio quarto) |

Filippo di Stai e compagni |

c |

185 |

f |

10 |

7 |

8 |

||

|

Giotto Ricci |

c |

186 |

f |

254 |

23 |

∙ |

6 |

|||

|

Somma 1703 s 4 d 3 a fior |

||||||||||

|

E nella faccia di sotto 55115 s 7 d 4 a fior |

||||||||||

|

Somma tutti creditori f 56819 s 2 d 7 a fior |

||||||||||

|

6435 s 6 d 7 a fior |

||||||||||

|

Somma tutto f 63254 s 9 d 2 a fior |

||||||||||

|

Avanzi f 54 s 5 – – a fior |

||||||||||

Table 11

|

Cash |

3 254 |

Creditors |

56819 |

|

Debtors |

60 054 |

Capital (6 435 + 54) |

6489 |

|

63 308 |

63 308 |

Table 12

|

Liquidity ratio |

(3 254 + 60 054) : (56 819) |

1, 1 times |

|

Quick ratio |

(3 254) : (56 819) |

0, 1 times |

|

Cash in hand ( contanti ) at November 1, 1377 |

|||||||

|

Fiorini |

835 in sugiello |

f |

835 |

||||

|

Ducati |

8 a Ѕ quattro vaglono |

f |

8 |

s |

5 |

||

|

(etc) |

|||||||

|

Libri |

474 s 10 di quattrini s 71 d 9 |

f |

132 |

s |

8 |

||

|

Somma f 1639 s 4 |

|||||||

|

Abattesene per creditori del quadernuccio che sono piщ che debitori f 30 s 19. In contanti f 1639 s 5 |

|||||||

Table 15

|

(Ledger) |

(Name and Company) |

(Carta) |

(Sum) |

||||||||||||||

|

Дебиторы |

Оранжевая четвертая книга |

Antonio da Uzano per panni comuni Angnolo di Latinuccio e comp Benedetto di ser Pagolo |

с с с |

L RRR VVV |

f f f |

214 2757 4870 |

25 28 28 |

1 11 – |

|||||||||

|

Кредиторы |

Оранжевая четвертая книга |

Domenicho di berto Galigaio Niccholo di Giovanni da Uza- no |

с |

XXX ttt |

f f |

18 624 |

16 13 |

6 – |

|||||||||

|

Somme f 20231 s 3 d 8 a fior Segreto f 6944 s 6 d 11 Somme in tutto f 27175. 10. 7 a fior Atti d’avanzo f 29. s 26 d 9 a fior е per entrata e uscita f 39. f 27 d. 3 Somme f 20231 s 3 d 8 a fior Segreto f 6944 s 6 d 11 Somme in tutto f 27175. 10. 7 a fior Atti d’avanzo f 29. s 26 d 9 a fior е per entrata e uscita f 39. f 27 d. 3 |

|||||||||||||||||

|

е questi netto ad avanzo |

|||||||||||||||||

|

Settenbre |

f |

22 |

s |

20 |

d |

10 |

|||||||||||

|

Novembre |

f |

6 |

s |

24 |

d |

4 |

|||||||||||

|

Dicembre |

f |

18 |

s |

16 |

d |

4 |

|||||||||||

|

f |

48 |

s |

3 |

d |

6 |

||||||||||||

|

Ottobre mancha |

f |

8 |

s |

5 |

d |

3 |

|||||||||||

|

Novembre |

f |

8 |

s |

24 |

d |

4 |

f |

39 |

s |

24 |

d |

3 |

|||||

Table 16

|

Cash |

3 057 |

Creditors |

27 175 |

||

|

Debtors |

24 047 |

Capital (profit) |

30 |

||

|

27 205 |

27 205 |

||||

|

Liquidity ratio |

(3 057 + 24 047) : (27 175) |

1, 0 times |

|||

|

Quick ratio |

(3 057) : (27 175) |

0, 1 times |

|||

Terra Humana

Table 13

|

Receipt for October 1377 (entrata) 1 Expense for October 1377 (uscita) |

|||||||||||||

|

. 4714 |

11 |

6 |

.1656 |

1 |

6 |

||||||||

|

. 2970 |

19 |

9 |

.1672 |

14 |

9 |

||||||||

|

(etc) |

(etc) |

||||||||||||

|

66283 |

5 |

9 |

64665 |

24 |

6 |

||||||||

|

Mancha chapitale f 8 s 5 d 3 a f |

1609 (66)275 |

5 0 |

6 |

||||||||||

1386 poses a part of an unsaved document and contains receipt and expense for January 27 and 29. The terms «debit» ( da ), «credit» ( a or ad ) and Latin figures on items are used in it. There is also a fragment of the receipt and expense generalization with Arabic ciphers. There is some archaism in the documents. On the whole, the information of this document is not enough to make particular judgements.

Conclusions. As can be seen from above, the documents from the Uzzano’s bank for 1363–1386 contained analytic information, extracted from the accounting books for purposes of supervision over its financial position. In this regard the analysis of the financial position of companies on the published archives of Datini and Medichi is of great interest.

Общество

Professional accounting was taught at Italian universities (they played the leading role in Western Europe) and commercial schools (in XIV century Venice and Florence there were few of them). Role of teachers in developing of accounting methodology, formalization of accounting procedures and stereotypes was extraordinary. Double entry ( la partita doppia ) was brought up to logically correct procedure by the intellectual efforts also.

Another feature of those documents was the simultaneous usage of terms: dare and uscita ; avere and entrata . Dare (debit) and avere (credit) are the terms of bank accounting ( conto

References The accounting archive of Fiorentine bank of uzzano (1363–1386) in saint-Petersburg

- Archive of Saint-Petersburg Institute of History of the Russian Academy of Science. -Fund 5. Cardboard 5. File 1. -[literally: Arhiv Sant-Peterburgskogo instituta istorii RAN. Zapadnoevropeyskaya sektsiya. Fond 5. Karton 5. Delo 1]

- Mal'kova T.N. The History of Accounting [literally: Istoria buhgalterskogo uchota]/Review: PhD, professor of Vilniaus Universitetas J. Mackevicius. -Moscow: Vysshaya shkola, 2008.

- Rutenburg V.I. Trade books of Florence/Italian communes of the XIV-XV centuries. Collection of documents from the archive of Leningrad institute of history of the Academy of Science of USSR. -Moscow-Leningrad: Nauka, 1965. -[literally: Torgovye knigi Florentsii/Ital'yanskii kommuny XIV-XV vekov. Sbornik dokumentov iz arhiva Leningradskogo institute istorii Akademii nauk SSSR), Moscow-Leningrad, Nauka]