Adaptation of Russian ferrous metallurgy supply chains to geopolitical challenges: From reorientation of flows to changes in financial results

Author: Petrov S.P., Pechenskaya-Polishchuk M.A.

Journal: Economic and Social Changes: Facts, Trends, Forecast @volnc-esc-en

Section: Branch-wise economy

Article in issue: 6 т.18, 2025.

Free access

For the Institute of Economics and Industrial Engineering of the Siberian Branch of the Russian Academy of Sciences and Vologda Research Center of the Russian Academy of Sciences, the study of sectoral and corporate development in ferrous metallurgy and its impact on economic growth is of particular importance due to the territorial location of production facilities. Years of research have established a robust methodological and practical foundation for understanding the patterns of spatial distribution of flows within Russia's ferrous metallurgy supply chains. Concurrently, the transformation of external and internal conditions shifts the research focus to new aspects, broadening and deepening the inquiry. The paper examines the spatial reconfiguration of flows within the supply chains of the Russian ferrous metallurgy industry under the influence of recent geopolitical shocks and challenges. The analysis focuses on three key regions: Siberia, the Urals, and the Northwest, which represent major centers for the production and consumption of metallurgical products. Using these regions as case studies, the article analyzes changes in logistics linkages and in the directions of raw material and finished product supplies amid heightened geopolitical instability. It also identifies the factors that determined the effectiveness of the spatial redistribution of flows within the supply chains of one of the country's key industries. The work analyzes how geopolitical shocks stimulate the reorientation of flows. Particular attention is paid to assessing the impact of these changes on the final financial performance of industrial enterprises. The research is based on the analysis of statistics and corporate public reporting data. The article is of interest to specialists in economics, logistics, regional development, and representatives of the metallurgical industry.

Ferrous metallurgy, supply chains, material flows, financial flows, spatial distribution, focal firm, geopolitical shocks, external shocks, sanctions

Short address: https://sciup.org/147252995

IDR: 147252995 | UDC: 338.45 | DOI: 10.15838/esc.2025.6.102.5

Text of the scientific article Adaptation of Russian ferrous metallurgy supply chains to geopolitical challenges: From reorientation of flows to changes in financial results

In the late 20th and early 21st centuries, the dominance of the globalization concept in the world economy led to a high degree of spatial distribution of supply chains and their dependence on global markets. However, despite all the advantages, the formation of global chains has also become a cause of reduced economic security for individual countries, increasing their vulnerability to geopolitical events, global trends, and other challenges. To preserve the capacity to withstand these challenges, the need has grown for understanding both the factors destabilizing industry markets and external shocks, as well as the composition of supply chains, since their participants are interconnected technologically and economically. Consequently, the propagation of effects from shocks in one link of the supply chain determines the effectiveness of the entire chain.

The geopolitical events of 2022 led to the imposition of sanctions by a number of countries against specific individuals, enterprises, and industries in Russia. As a result, it became necessary to restructure certain parameters of the Russian economy, which was integrated into global markets. A wide range of industries faced serious challenges, including ferrous metallurgy, engineering, and energy, which had already encountered various restrictions on global markets since 2014. The economy’s adaptation to the new conditions, in particular, took the form of restructuring supply chains. This primarily manifested in the reconfiguration of inter-industry linkages, including changes in the composition of their participants and the spatial orientation of these chains’ operations. The reorientation toward new sales markets, prompted by imposed restrictions on exports to Western countries, was especially pronounced. Due to changes in various chain links, a redistribution of material and financial flows occurred. Furthermore, problems that were previously solved through imports intensified, primarily concerning equipment, materials for production activities, and service support. At the same time, despite the similarity of effects from the imposed sanctions, the depth of changes varied significantly among different economic entities and within the supply chains they participated in.

In the conditions described above, the issue of identifying the factors determining changes in flows within the supply chains of Russia’s ferrous metallurgy under the influence of the imposed sanctions, which served as external (geopolitical) shocks for the industry, has become particularly relevant. This constitutes the objective of the present study.

Theoretical foundations and the state of research on the topic

An emerging supply chain within an industry complex represents a system of economic agents, activities, information, and resources involved in moving a product or service from a supplier to a consumer (Dametew et al., 2016). In essence, these are ordered sequences of suppliers and consumers, where each consumer is also a supplier, and so on until the finished product reaches the end user. Furthermore, modern supply chains may not end with the final consumption process but can include after-sales support and product disposal services.

Supply chains consist of entities that facilitate the movement of goods from suppliers to end consumers. Key participants in these chains include suppliers of raw materials and components, equipment suppliers, producers of the product or service, distribution firms, financial institutions, and so on. In this context, consumers also become important participants in the chains built around the enterprises in question, serving as a source of information necessary for enhancing firms’ competitiveness (Prigulniy, 2021). This underscores the strong link between supply chain organization and end-customer satisfaction (Abd et al., 2016). A special place in the supply chain is occupied by the focal firm, the entity around which the entire chain is structured. Essentially, this is the firm that determines the chain’s configuration, and its goals influence the structure, forms of interaction among participants, and the overall organization of the chain (Lyubyashchenko, 2023). Typically, the manufacturer acts as the focal firm, concentrating flows of raw materials, components, equipment, necessary services, etc., and serving as the starting point for the movement of the product created within the supply chain.

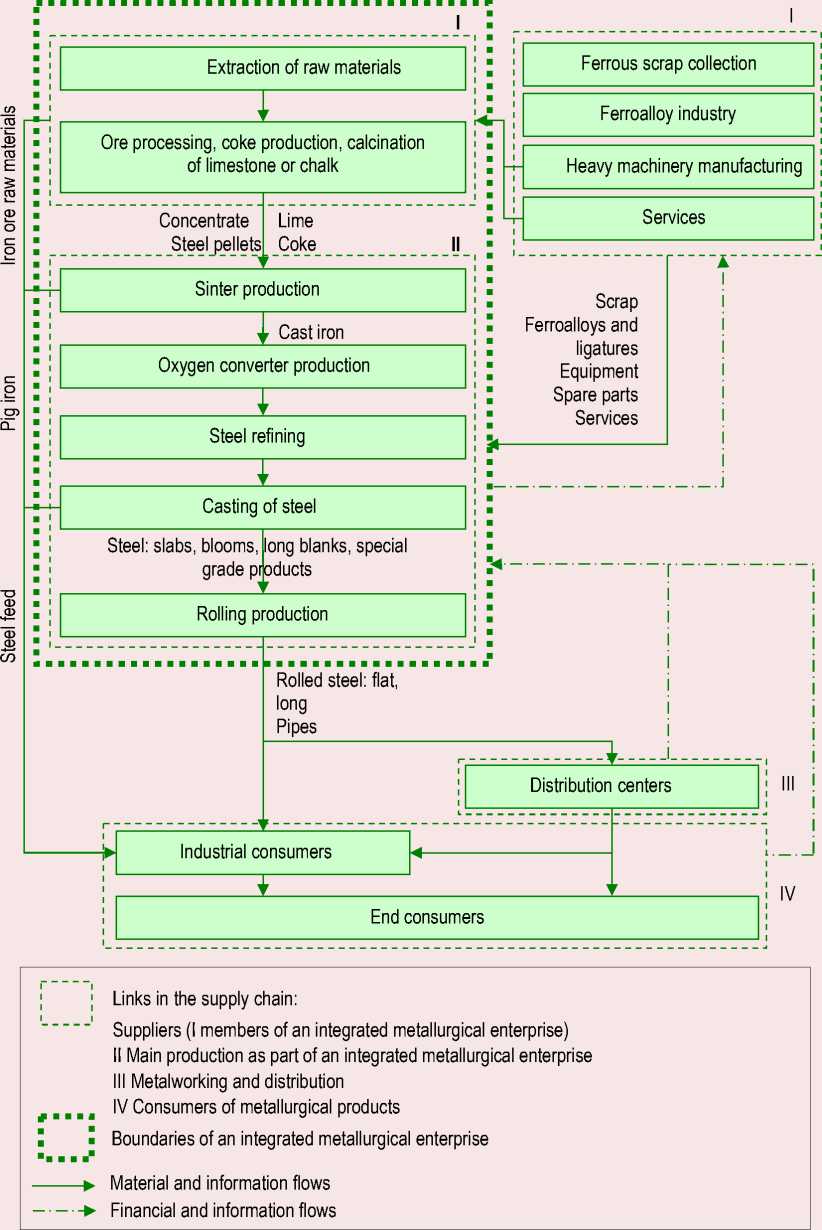

In turn, the interconnections between supply chain participants are expressed in the material, financial, and information flows existing within them ( Fig. 1 ). The study of these flows is fundamental to understanding how supply chains are formed, how their organizational forms influence the chain participants and the industry markets they operate in (and vice versa), what problems and failures exist in chain operations, and what determines their effectiveness, among other things. Furthermore, considering the role of various participants in the form of a multi-level organization of supply chains determines the spatial distribution of flows within them (Tyapukhin, 2021). As seen in Figure 1, supply chains can be described as a flow of materials, information, payments, and services from raw material suppliers through manufacturers and distributors to end consumers (Dametew et al., 2016). It should be noted that focusing attention either on the participants of supply chains or on the flows between them leads to the identification of two approaches to defining, constructing, and analyzing supply chains: the object-based and the processbased approaches (Kireeva, 2012).

The primary methodological toolkit for studying supply chains is established within the management discipline of supply chain management (SCM). A wide range of works on SCM presents fresearch aimed at forming the concept of supply chain management, defining its object and methods of study, identifying general directions for the discipline’s development, and so on. Typically, such research is applied in nature and involves studying the organization and functioning of specific chains, the experience of

Figure 1. Components and flows of a manufacturing firm’s supply chain

S U P P L I E R

Information flow <----------------------------------------->

Planning and forecasting

Supply

Production

Distribution and logistics

Customer Assessment of service the works performed

^ material flow

financial flow <

C O

N S

U M

E R

Source: (Spekman et al., 1998).

individual firms or firms within a particular industry, and developing tools for efficiently conducting transactions with suppliers and customers (Donohue, Croson, 2002; Cheng, Grimm, 2006; Kireeva, 2012; Chopra, Meindl, 2013).

The focus of supply chain management as a discipline on researching and developing tools for managing specific chains has become the basis for its criticism as a scientific field with a weakly formed paradigm from the perspective of economic theory representatives (see, for example, Williamson, 2008; Storchevoy, 2014). At the same time, the analysis of supply chains using the tools of economic theory is less common. However, both theoretical and applied research is being conducted. Within economic works, one can identify the application of tools from industrial organization theory (Ralston et al., 2015; Delgado, Mills, 2020), game theory (Um et al., 2010; Zinovieva, Savin, 2020), input-output modeling (Thekdi, Santos, 2016), and network modeling (Pazoki et al., 2011). It should be noted that the presented works examine either a separate aspect of supply chain functioning and its impact, for example, on firms’ profitability, or specific industry markets and firms. In our view, this is due, firstly, to the absence of a well-developed toolkit within economic theory specifically designed for supply chain analysis, and secondly, to significant differences in the applied aspects of industry market structures and firm behavior within them. Therefore, applying the supply chain concept is currently only feasible at the level of individual industry markets. For instance, one can highlight works dedicated to researching the construction industry using industrial organization theory tools (London, 2008), the oil industry (Chima, 2007; Li et al., 2021), and the automotive industry (Ambe, Badenhorst-Weiss, 2011). Among domestic studies, there is research focused on modeling supply chain operations in food production (Fetyukhina, 2007), mechanical engineering (Kovalev, 2014), and the coal industry (Solodovnikov, 2018).

Works aimed at researching supply chains in ferrous metallurgy are primarily related to supply chain management. For example, V.V. Solodovnikov presented an overview of supply chain development in ferrous metallurgy, built a generalized supply chain model for metallurgical enterprises, and identified tools for integrated supply chain planning (Solodovnikov, 2017a; Solodovnikov, 2017b). A number of works are dedicated to the issue of supply chain integration in the steel industry, including on global markets (Pleshchenko, 2013; Dametew, Ebinger, 2017; Fregoso, 2019). However, in our opinion, they do not pay sufficient attention to spatial aspects and the influence of various factors, such as geopolitical events, on the functioning of supply chains in ferrous metallurgy.

Methodological aspects of the research

This study is applied in nature and utilizes categories of industrial organization theory within the process-based approach to supply chain analysis. The methodological foundation of this work is an expert-analytical approach to assessing changes in flows and their spatial distribution within the supply chains of Russia’s ferrous metallurgy. The information base included publications by domestic and foreign authors on the development of supply chains and Russia’s ferrous metallurgy. Furthermore, the work utilized annual, public financial reports of Russian metallurgical enterprises, data from Rosstat, as well as information and data from official media websites (Kommersant, Interfax, RBC, Vedomosti, etc.).

Research results

Organization of flows in the supply chains of Russia’s ferrous metallurgy

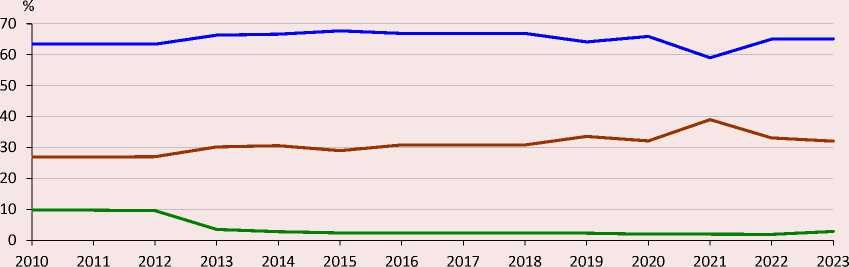

In light of technological and economic factors, ferrous metallurgy has become an industry with a high degree of integration of various stages of the supply chain. Consequently, the organizational form of ferrous metal producers based on large integrated plants, since the 2000s consolidated with suppliers of key raw material types into holding structures, has become most widespread in Russia. For instance, in 2020, the eight largest plants in the country accounted for 94% of pig iron production, 77% of steel, and 80% of rolled products (Katunin et al., 2021). However, a long-term trend of increasing the share of steel production using electric arc furnace capacities is evident (Fig. 2). This has manifested, in particular, in increased steel production by small, non-integrated plants, including through the launch of new enterprises (e.g., Tyumen Electrosteel, Abinsk ESW). As a result, two main schemes for organizing supply chains, differing in the spatial scope of the flows formed within the chains, have emerged in Russia’s ferrous metallurgy.

The primary scheme for organizing supply chains in Russia’s ferrous metallurgy is the supply chain of an integrated metallurgical enterprise with a metallurgical plant as the focal firm ( Fig. 3 ). On one hand, it centralizes flows from suppliers of raw materials, energy, services, etc. On the other hand, it generates flows towards end consumers. An important feature here is that the metallurgical plant’s output is intermediate. This leads, in the direction of flows to consumers, to predominant

Figure 2. Technological structure of steel production in Russia, 2010–2023

Year

^^^^^м Oxygen converter production ^^^^^^^^м Electric steelmaking

^^^^^^^^п Open-hearth production

Note: the structure for 2023 is estimated.

Source: World Steel in Figures. World Steel Association. Available at: (accessed: 17.08.2025).

Figure 3. Predominant scheme of the supply chain organization for an integrated metallurgical enterprise in Russia

Source: (Petrov, 2023).

interaction with producers engaged in further processing. The scale of operations of metallurgical plants (product range, production volumes) explains the broad spatial distribution of the supply chains built around them.

There is one integrated metallurgical enterprise each in Siberia and Northwestern Russia: JSC EVRAZ Consolidated West Siberian Metallurgical Plant (EVRAZ ZSMK) within EVRAZ, and Cherepovets Metallurgical Plant (CherMK) within PJSC Severstal, respectively. They have a similar organization of raw material, supply, and energy flows within their supply chains. The main raw material supply hub for EVRAZ ZSMK is internal suppliers based in the Kuzbass basin, integrated into the enterprise. However, while EVRAZ ZSMK is fully self-sufficient in coking coal, its selfsufficiency in iron ore raw materials is incomplete. Therefore, additional raw material flows come from the Irkutsk Region, the Republic of Khakassia, the Urals, and the Northwest of the country. CherMK is located at the intersection of ore, coal, and finished product flows. Ore flows come from the Republic of Karelia, Murmansk Region, and Belgorod Region. Coal flows arrive from the Urals, based on the Pechora coal basin, formed by the mining and processing capacities within PJSC Severstal. Ore is also supplied by external suppliers in the Murmansk and Kemerovo regions (Ilyin et al., 2021; Lukin, 2021; Pechenskaya-Polishchuk, Malyshev, 2022). Unlike these enterprises, the Ural plants have relatively low self-sufficiency in raw materials, leading to a broader spatial scope of flows from other regions, including Siberia and the Northwest of the country, as well as import supplies. For example, the primary portion of iron ore raw materials for the Chelyabinsk Metallurgical Plant (ChMK), part of PJSC Mechel, is supplied from the Irkutsk Region via the Korshunovsky Mining and Processing Plant (GOK), which is also part of Mechel1. Meanwhile, until 2022, the Magnitogorsk Metallurgical Plant (MMK) received the bulk of its ore from the Northwest of the country and from Kazakhstan.

Flows toward consumers, despite similar organizational forms among different ferrous metal producers, have several distinctive features. Overall, the main consumers of integrated metallurgical enterprises’ products are construction companies, engineering enterprises, metal product manufacturers, and the energy sector. This determines a wide spatial coverage of metallurgical product flows. The products of full-cycle plants are shipped to virtually all regions of Russia. The specialization of a particular enterprise is crucial here. For example, EVRAZ ZSMK specializes in semi-finished products, construction sections, and railway sections (these segments accounted for 37.1, 31.2, and 10.6% of sales revenue in 2021, respectively2). While construction sections primarily serve the needs of the Asian part of the country (estimated, based on Rosstat data for 2017–2019, an average of 55.6% of section supplies from Kemerovo Region went to Asian Russia), railway sections are widely supplied for export and across all of Russia, as the plant is a key supplier to Russian Railways (RZhD), as well as tram and subway rails. For instance, PJSC Severstal, specializing in flat and long steel products, until 2022 exported about 45% of its production, mainly to Europe (31% of the company’s total sales volume in 2021)3. MMK, also specializing in flat and long products, primarily focuses on domestic demand, exporting less than 20% of its output, with the group’s main foreign buyers, as with EVRAZ, being Eastern countries4.

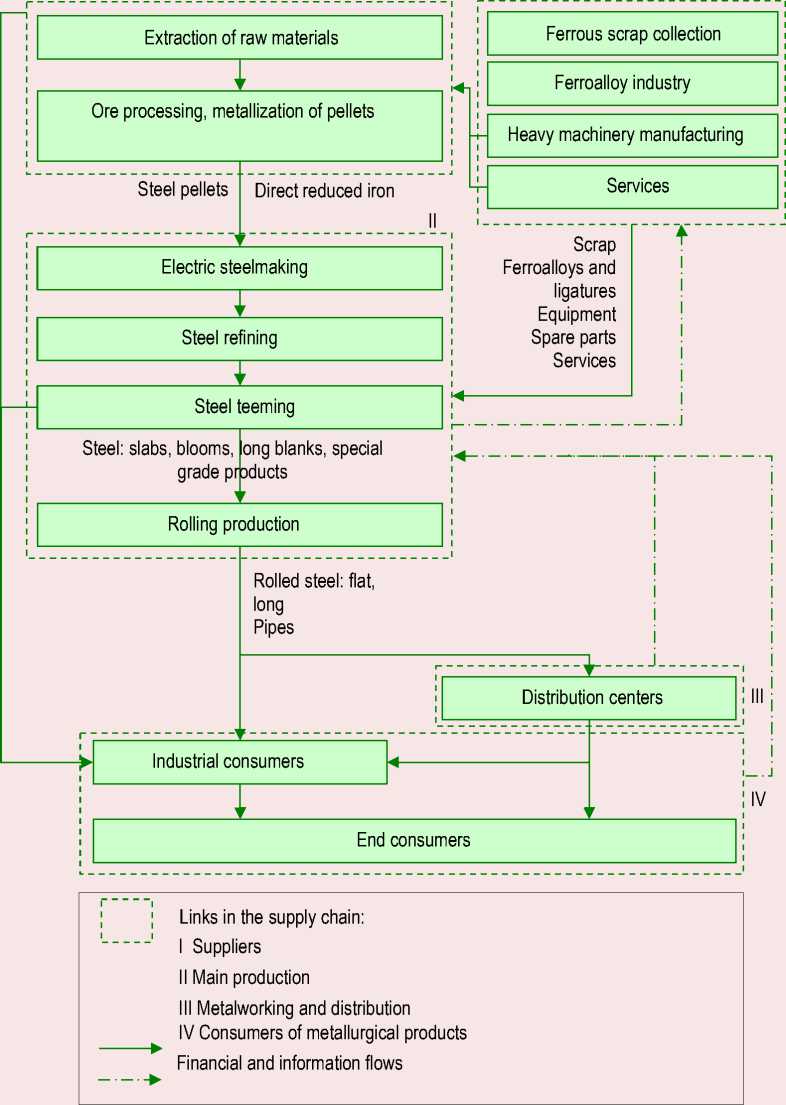

The second scheme for organizing supply chains in ferrous metallurgy is associated with the activities of small metallurgical plants, which act as the focal firms ( Fig. 4 ). Typically, such plants are electric

Figure 4. Predominant scheme of the supply chain organization around an electric steelmaking plant in Russia

Source: (Petrov, 2023).

steelmaking facilities, and unlike the supply chains of integrated metallurgical enterprises, their flows have a more limited spatial scope. Both flows from suppliers of raw materials and components and flows toward consumers are primarily concentrated within the region where the focal firm is located. The basic raw material for their operations is ferrous scrap metal, which is sourced from the federal district where the steelmaking plant is situated. The main products supplied to consumers within such a supply chain are long steel products for the construction industry and metal products aimed at the needs of engineering enterprises. For example, OOO UMK Tyumen Electrosteel in the Tyumen Region operates according to this scheme. Some plants focus on exporting their products, like OOO Amurstal in the Khabarovsk Krai, which supplies not only rolled products to regions of the Far East but also steel billets to China and Southeast Asian countries.

Sanctions imposed by western countries on Russia’s ferrous metallurgy industry

Ferrous metallurgy is one of the Russian economic sectors most affected by the sanctions imposed against the country since 2022. A series of sanctions packages adopted by Western countries contain restrictions on the free operations of Russian metallurgy on the global market. It is worth emphasizing that various forms of restrictions on the activities of Russian metallurgical companies began to be introduced as early as 2014, but until 2022, they primarily took the form of duties, quotas, etc., and did not lead to significant consequences for the established supply chains in Russia’s ferrous metallurgy. With the adoption of the 2022 sanctions, a situation emerged testing the capabilities of focal firms to restructure their chains in response to drastic changes in operating conditions. This restructuring of supply chains manifested itself primarily in a change in the spatial orientation of key flows.

In March 2022, as part of the fourth sanctions package, the European Union imposed sanctions against Russian steelmakers, restricting the import of certain types of steel products from Russia. In October 2022, EU countries adopted the eighth sanctions package against Russia, which included, among other things, restrictions on the supply of ferrous metal semi-finished products. The sanctions targeting slab supplies were structured in such a way that until September 30, 2024, Russia was allowed to export 3.75 million tons per year, as otherwise, a severe blow would have been dealt to European metallurgical enterprises dependent on supplies from Russia5. On December 16, 2022, the ninth sanctions package was adopted, affecting the mining sector. It introduced a prohibition on new investments in Russia’s mining industry, including the provision of loans for these purposes. However, a number of exceptions were specified for raw materials critical to Europe, including iron ore6. In December 2023, the 12th sanctions package banned supplies of pig iron (including refined/ spiegel iron), ferroalloys, and direct reduced iron from Russia7. Notably, under the 12th package, the deadline permitting the import of Russian steel slabs and billets into the EU was extended until 20288.

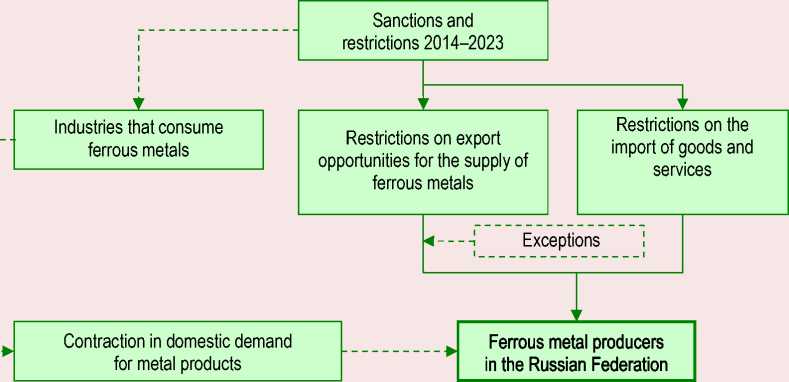

Based on the target of restrictions and their impact on supply chains in the ferrous metals industry, the sanctions can be divided into two types ( Fig. 5 ).

The first type encompasses sanctions related to industries that consume ferrous metals, which essentially affect domestic demand indirectly. These manifest both as bans on supplying products from Russian metal-consuming

Figure 5. External shocks of restrictions and regulation on Russia’s ferrous metallurgy

Sources: (Dranev, 2021; Petrov, 2023).

industries to external markets and as restrictions on the supply of components, technologies, and equipment, thereby reducing the production capacities of these industries. This, in turn, led to a contraction in demand for metal products. Firstly, there was a destabilization of already established linkages within supply chains. Secondly, limitations arose in the ability to build new connections between metal producers and domestic consumers to replace the lost flows. As a result, the alteration of supply chains from this type of sanction was expressed in a narrowing of material flows from primary production to consumers and of financial flows in the opposite direction along the chain linkages. For instance, in 2022, metal consumption by the engineering sector fell significantly due to a drop in automobile production (by 67% compared to 20219) following the halt in supplies of a range of foreign components and the exit of foreign manufacturers from Russia.

An important consequence of this type of sanction is that, under non-integrated forms of interaction, the risk of overall supply chain disruption increased due to a higher probability of bankruptcy for the focal firm. Since the profitability of such enterprises is several times lower than that of integrated ferrous metallurgy enterprises, the decline in revenue resulting from the imposed sanctions has a more pronounced impact on the financial stability of non-integrated companies.

The second type comprises sanctions directly targeting the ferrous metallurgy industry, which primarily affected export capabilities. In this case, the supply chains experienced a disruption of material flows from primary production toward consumers. In response, metallurgical holdings began forming new flows in two directions. The first direction involves establishing or expanding ties with consumers in friendly countries. However, the necessity of offering discounts on ferrous metal products for these new markets, which are less lucrative compared to the now-closed European ones, has led to a significant reduction in the volume of financial flows within the supply chains.

The second direction of countermeasures against the imposed sanctions has been the formation of flows enabling indirect supply of products to the global market. For instance, exports of raw materials and semi-finished products, previously shipped directly to the EU, are now partially routed through Turkiye, where they are processed and then exported to European countries10. Furthermore, new flows have been created or existing ones expanded on the domestic market to replace some of the lost export shipments.

Russian steel corporations are in acute need of a stable and uninterrupted financial settlement system to conduct any international trade and financial operations without hindrance. Sanctions have been imposed on individuals such as A. Mordashov, a shareholder of PJSC Severstal; R. Abramovich, co-owner of Evraz; V. Rashnikov, owner of the Magnitogorsk Iron and Steel Works (MMK); and A. Usmanov, owner of Metalloinvest11. At the same time, the owner of NLMK, V. Lisin, has avoided sanctions, partly because the holding has production facilities in Belgium, Denmark, Italy, and France, with a total annual output of 4.4 million tons and an average headcount of about 1.8 thousand people12. Among Russian metallurgical corporations, PJSC Severstal has been the most severely affected. Due to the imposed sanctions, supplies to Europe (34% of the company’s exports) were halted as early as March 2022. In just the period from February to November 2022, the corporation lost $400 million due to the seizure of its Western warehouses and accounts13. In turn, one of the earliest reactions to Western sanctions was the re-domiciliation of the charter capital of PJSC MMK to Russian jurisdiction – from the Cypriot Mintha Holding Limited to the Russian company Altair in Magnitogorsk – prompted by the risks associated with managing Russian investments14.

As a consequence of the imposed sanctions and the formation of new flows, 2022 saw a decline in metallurgical production and capacity utilization. In 2023, production began to recover, though not uniformly across all regions hosting metallurgical enterprises ( Tab. 1 ).

The contraction of primary production led to changes in the volume of flows along the linkages between suppliers and producers. In this case, however, the changes primarily concerned flows from foreign suppliers, which incentivized focal firms to reconfigure these flows towards domestic sources. For example, this issue manifested in 2022 when the Sokolov-Sarbai Mining and Processing Production Association (SSGPO) from Kazakhstan refused to supply iron ore raw materials to the Magnitogorsk Iron and Steel Works (MMK). Supplies from Kazakhstan had accounted for approximately 70% of the plant’s needs. PJSC MMK shifted to purchasing additional volumes of raw materials from Russian producers, including Metalloinvest, which found it advantageous to reorient its supplies to the domestic market due to a shortage of dry cargo ships for exporting raw materials from Russian ports15.

Table 1. Capacity utilization rate (% of average annual production capacity) for selected products

Region 2021 2022 2023 Unalloyed steel in ingots or other primary forms, and semi-finished products of unalloyed steel Kemerovo Region 69.5 59.6 54.9 Vologda Region 93.7 85.5 90.4 Chelyabinsk Region 95.9 83.7 - Finished rolled products Kemerovo Region 80.2 71 65.6 Vologda Region 72.5 63.1 65.4 Chelyabinsk Region 81.2 70.8 - Compiled from: Industrial Production. Territorial Branch of the Federal State Statistics Service for the Kemerovo Region – Kuzbass. Available at: (accessed: 29.08.2025); Industrial Production. Territorial Branch of the Federal State Statistics Service for the Vologda Region. Available at: (accessed: 29.08.2025); Industrial Production. Territorial Branch of the Federal State Statistics Service for the Chelyabinsk Region. Available at: industrial_production (accessed: 29.08.2025).

The ban on supplies of metallurgical equipment to Russia had an unambiguously negative effect on the interaction between suppliers and producers of ferrous metals. In 2021, imported products accounted for 70% of the metallurgical equipment market, and for 80–90% of most positions in the mining and processing equipment market16. The main suppliers were European enterprises. A similar situation was observed with service maintenance. While flows of raw materials, supplies, and metallurgical products can be restored in the short term, flows related to equipment and service maintenance require long-term investments.

As a result, the outlined dimensions of sanction impact allow us to identify a number of key factors that determined the degree of change in the flows within Russia’s ferrous metallurgy supply chains:

– type of product: low value-added (primary processing), general-purpose, specialized products;

– type of end consumers: large-scale or smallscale consumers;

– sales orientation: domestic market, exports to the West, exports to Asia and countries of the Global South;

– presence of assets abroad that are critical to the host countries;

– dependence on external supplies: metallurgical equipment, service maintenance, raw materials and supplies, etc.

Impact of sanctions on the financial performance of Russian ferrous metallurgy corporations

Based on the identified key factors that influenced the degree of change in the supply chain flows of metallurgical plants, a logical question arises: how did the impact of these factors during the sanctions period affect the operational and financial results of the enterprises? To answer this question, it is advisable to use the official public reporting of the companies themselves, compared with the pre-sanctions period. Given the available data, this analysis will be conducted for the first half-year periods of four years, starting from 2021, for the major companies PJSC Severstal, PJSC MMK, and PJSC EVRAZ. A large Russian company from the Central Federal District, PJSC NLMK, has also been added to the comparative analysis.

PJSC Severstal (Northwestern Federal District, Vologda Region)

The key factor driving changes for PJSC Severstal was the cessation of operations with the European market (34% of revenue), which negatively impacted almost all of the company’s

Table 2. Dynamics of financial results of PJSC Severstal for the first half-year, million RUB

|

Indicator |

H1 2021 |

H1 2022 |

H1 2023 |

H1 2024 |

H1 2024 vs H1 2021 |

|

Revenue |

383064 |

376893 |

339429 |

409138 |

1.1-fold |

|

Cost of sales |

158868 |

199472 |

193010 |

247591 |

1.6-fold |

|

Share of cost of sales in revenue, % |

41.5 |

52.9 |

56.9 |

60.5 |

+19 p.p. |

|

Gross profit |

224196 |

177421 |

256419 |

161547 |

0.7-fold |

|

General and administrative |

12330 |

13823 |

12246 |

15323 |

1.2-fold |

|

General & administrative expense-to-revenue, % |

3.2 |

3.7 |

3.6 |

3.7 |

+0.5 p.p. |

|

Selling expenses |

24327 |

30714 |

23141 |

28703 |

1.2-fold |

|

Selling expense-to-revenue, % |

6.4 |

8.1 |

6.8 |

7.0 |

+0.6 p.p. |

|

Operating profit |

187153 |

115329 |

100434 |

107007 |

0.6-fold |

|

Finance income |

247 |

2581 |

3738 |

14393 |

58.3-fold |

|

Finance costs |

5793 |

4990 |

5606 |

13689 |

2.4-fold |

|

Net foreign exchange result |

-909 |

37214 |

29695 |

-13437 |

14.8-fold |

|

Profit before tax |

171217 |

145423 |

122548 |

98764 |

0.6-fold |

|

Income tax expense |

33343 |

27743 |

17545 |

15446 |

0.5-fold |

|

Tax burden on the tax base, % |

19.5 |

19.1 |

14.3 |

15.6 |

-3.9 p.p. |

|

Profit for the period |

137836 |

117680 |

105003 |

83318 |

0.6-fold |

|

Net profit margin, % |

36.0 |

31.2 |

30.9 |

20.4 |

-15.6 p.p. |

|

Compiled from: PJSC Severstal IFRS data. |

|||||

operational and financial performance indicators ( Tab. 2 ). For instance, in the first half of 2024 compared to the first six months of 2021, consolidated revenue grew by only 7% – from RUB 383 billion to RUB 409 billion – while the cost of sales increased much more significantly, by 56%, ultimately reducing gross profit by almost one-third (-28%). In turn, the growth in production costs outpacing the company’s income led to an increase in the share of cost of sales in revenue from 41.5% to 60.5%. Simultaneously, sanctions against PJSC Severstal and its owner resulted in increased selling expenses for the company, both in the first half of 2022 (+26.3%, to RUB 30.7 billion) and in subsequent periods. To preserve corporate governance, the parent company Rutgers Severtar of A. Mordashov changed its jurisdiction from Cypriot to Russian. The Cherepovets-based LLC Rutgers Severtar changed its owner from the

Cypriot Severtar Holding LTD to the Russian MK LLC Severtar Holding and registered in a special economic zone in the Kaliningrad Region17.

Against the backdrop of all these trends, net profit volume decreased (by 40%), as did its profitability margin (from 36 to 20.4%), along with the tax burden. Thus, the company’s profit before tax by the end of the period showed a sharp decline of 42% compared to the first six months of 2021 (to RUB 98.8 billion), and income tax fell by 54% (to RUB 15.4 billion). This was reflected in the drop in the current income tax rate, which, compared to the standard 20%, decreased from 19.5 to 15.6%.

Following the 2022 sanctions, PJSC Severstal redirected its flows from external to domestic markets. Whereas before the restrictions the company sold up to 40% of its products on export markets, this share subsequently decreased to 10–15%18.

PJSC MMK (Ural Federal District, Chelyabinsk Region)

The imposed sanctions led to a decline in profitability ( Tab. 3 ). In 2021 the profit margin reached 20–25%, while by May–June 2022 it had shrunk to 1–4%. General and administrative expenses, as well as selling expenses, increased by 37% and 27%, respectively. Against the backdrop of a sharp rise in production costs (+34%), the share of cost of sales in revenue increased from 57.6 to 74.6%. In turn, the company’s tax base contracted by 53%, and income tax itself fell by 44%, while the effective tax rate remained relatively high (23.4%). Both the company’s consolidated net profit (down 55%) and its profitability (from 27.6 to 12%) also decreased.

It is important to note that PJSC MMK was among the first companies after February 24, 2022, to carry out re-domiciliation (a transfer from Cypriot to Russian jurisdiction). As a result of the transaction, 79.76% of PJSC MMK shares held by Mintha Holding Limited (Cyprus) were transferred to the ownership of Altair LLC (Russian Federation, Magnitogorsk)19. The decision to restructure was made considering the reduced attractiveness of Cyprus for holding and managing Russian investments, as well as to leverage the advantages created in Russia in the sphere of corporate regulation and the existing legal and investment norms in the Russian Federation20.

Table 3. Dynamics of financial results of PJSC MMK for the first half-year periods 2021–2024, million RUB

|

Indicator |

H1 2021 |

H1 2022 |

H1 2023 |

H1 2024 |

H1 2024 vs H1 2021 |

|

Revenue |

403851 |

403039 |

352708 |

417829 |

1.03-fold |

|

Cost of sales |

232801 |

288514 |

251816 |

311500 |

1.3-fold |

|

Share of cost of sales in revenue |

57.6 |

71.6 |

71.4 |

74.6 |

17 p.p. |

|

Gross profit |

171050 |

114525 |

100892 |

106329 |

0.6-fold |

|

General and administrative |

7774 |

8487 |

8827 |

10647 |

1.4-fold |

|

General & administrative expense-to-revenue |

1.9 |

2.1 |

2.5 |

2.5 |

+0.6 p.p. |

|

Selling expenses |

22995 |

24569 |

25701 |

29228 |

1.3-fold |

|

Selling expense-to-revenue |

5.7 |

6.1 |

7.3 |

7.0 |

+1.3 p.p. |

|

Operating profit |

141235 |

79740 |

65996 |

67364 |

0.5-fold |

|

Finance income |

843 |

3041 |

5099 |

9353 |

11.1-fold |

|

Finance costs |

1195 |

2471 |

3383 |

2713 |

2.3-fold |

|

Net foreign exchange result |

292 |

-1814 |

1899 |

-5992 |

-20.5-fold |

|

Profit before tax |

139097 |

72668 |

66892 |

65701 |

0.5-fold |

|

Income tax expense |

27495 |

15880 |

15274 |

15392 |

0.6-fold |

|

Tax burden on the tax base |

19.8 |

21.9 |

22.8 |

23.4 |

+3.6 p.p. |

|

Profit for the зeriod |

111602 |

56788 |

51618 |

50309 |

0.5-fold |

|

Net profit margin |

27.6 |

14.1 |

14.6 |

12 |

-15.6 p.p. |

|

Compiled from: PJSC MMK IFRS data. |

|||||

PJSC EVRAZ (Siberian Federal District, Kemerovo Region)

Due to PJSC EVRAZ’s inability to secure an auditor following sanctions against the company, the latest IFRS reporting available for analytical purposes is only for the first half of 202221.

Despite the sanctions pressure against Russia, the company’s revenue grew by 28%, reaching nearly RUB 593 billion. Unlike other companies, the increase in the cost of sales was similar (+31%), which did not lead to a significant rise in its share of revenue (+1.1 p.p., to 59.9%). Logistics problems were reflected in the company’s selling expenses, which increased by 61%, with their share of revenue rising from 6.7 to 8.4%. A key factor in reducing the taxable base was a 58.4-fold increase in the net loss on foreign exchange differences. As a result, profit before tax decreased by 79%, while income tax expense showed a smaller decline (-19%). Due to high income tax expenses, the company’s net profit plummeted 206-fold to RUB 439 million, with its net profit margin for the first half of 2022 amounting to just 0.1% (Tab. 4).

In March 2023, the Cypriot company Streamcore, 50% of which was owned by PJSC EVRAZ, was re-registered under Russian jurisdiction in the Special Administrative District on Russky Island in Vladivostok, under the name MK OОО Streamcore. According to the Unified State Register of Legal Entities (EGRUL), 50% of Streamcore is owned by the Luxembourg-based company Evraz Group S.A., and 50% by LLC Invest-VK, whose primary owner is A. Rybkin (beneficial owner of JSC Siberian Mining and Metallurgical Company, Kemerovo Region)22.

Table 4. Dynamics of financial results of PJSC EVRAZ for the first half-year periods 2021–2022, million RUB

|

Indicator |

H1 2021 |

H1 2022 |

H1 2022 vs H1 2021 |

|

Revenue |

461136 |

592552 |

1.3-fold |

|

Cost of sales |

271173 |

354785 |

1.3-fold |

|

Share of cost of sales in revenue |

58.8 |

59.9 |

+1.1 p.p. |

|

Gross profit |

189963 |

237767 |

1.3-fold |

|

General and administrative |

21497 |

25833 |

1.2-fold |

|

General & administrative expense-to-revenue |

4.7 |

4.4 |

-0.3 p.p. |

|

Selling expenses |

30902 |

49764 |

1.6-fold |

|

Selling expense-to-revenue |

6.7 |

8.4 |

+1.7 p.p. |

|

Operating profit |

130548 |

28029 |

0.2-fold |

|

Finance income |

224 |

878 |

3.9-fold |

|

Finance costs |

9256 |

7830 |

0.9-fold |

|

Net foreign exchange result |

-2239 |

-130702 |

58.4-fold |

|

Profit before tax |

121741 |

25833 |

0.2-fold |

|

Income tax expense |

31275 |

25394 |

0.8-fold |

|

Tax burden on the tax base |

25.7 |

98.3 |

+72.6 p.p. |

|

Profit for the period |

90466 |

439 |

0.005-fold |

|

Net profit margin |

19.6 |

0.1 |

-19.5 p.p. |

|

Compiled from: PJSC EVRAZ IFRS data. |

|||

21 EVRAZ will not publish its annual report and IFRS financial statements due to the absence of an auditor. Available at: (accessed: 26.08.2025); EVRAZ will not be able to disclose the IFRS report for 2023. Available at: (accessed: 26.08.2025); EVRAZ will not publish its annual report and financial statements under IFRS for 2024 due to the absence of an auditor. Available at: news/evraz-ne-budet-publikovat-opublikovat-godovoy-otchyet-i-finansovuyu-otchyetnost-po-msfo-za-2024/ (accessed: 26.08.2025).

22 The joint venture between Evraz and the owner of SMMC was redomiciled from Cyprus to the Russian Federation. Available at: (accessed: 20.08.2025).

PJSC NLMK (Central Federal District, Lipetsk Region)

The consolidated revenue of the Novolipetsk Steel plant remained virtually unchanged (-0.4%), and the increase in its cost of sales was not as substantial as that of the other analyzed companies – 17% (rising from 49 to 57.6% of revenue). The taxable base was significantly impacted by a 1.5-fold increase in selling expenses and a 3.6-fold rise in the loss on foreign exchange differences. This led to a 47% decrease in the company’s profit before tax and a 40% reduction in income tax payments, even against a slight increase in the effective tax rate (from 18.6 to 21.2%). Meanwhile, the company’s consolidated net profit halved, and its net profit margin dropped from 30.6 to 15.8% ( Tab. 5 ).

In June 2023, the key shareholder of PJSC NLMK, V. Lisin, transferred his stakes in NLMK and First Cargo Company from Cypriot jurisdiction to structures named Serenity II Holdings and Nebula II Holdings, registered in Abu Dhabi (UAE). As of the end of 2022, control over 79.3% of PJSC NLMK shares was exercised through the Cypriot company Fletcher Group Holdings23.

It should be noted that PJSC NLMK has not been subjected to EU or US sanctions. For instance, Belgium did not vote for the eighth sanctions package against Russia because NLMK Group operates plants on its territory employing 1,200 people24. Furthermore, NLMK Group owns and operates plants in Italy and the USA25 with an annual production volume exceeding 4 million tons26.

Table 5. Dynamics of financial results of PJSC NLMK for the first half-year periods 2021–2024, million RUB

|

Indicator |

H1 2021 |

H1 2022 |

H1 2023 |

H1 2024 |

H1 2024 vs H1 2021 |

|

Revenue |

520017 |

no data |

444162 |

517789 |

0.99-fold |

|

Cost of sales |

255127 |

no data |

253396 |

298106 |

1.2-fold |

|

Share of cost of sales in revenue |

49.1 |

no data |

57.1 |

57.6 |

+8.5 p.p. |

|

Gross profit |

264890 |

no data |

190766 |

219683 |

0.8-fold |

|

General and administrative |

15804 |

no data |

13509 |

16388 |

1.0-fold |

|

General & administrative expense-to-revenue |

3.0 |

no data |

3.0 |

3.2 |

+0.1 p.p. |

|

Selling expenses |

29828 |

no data |

41326 |

44993 |

1.5-fold |

|

Selling expense-to-revenue |

5.7 |

no data |

9.3 |

8.7 |

+3 p.p. |

|

Operating profit |

216106 |

no data |

121808 |

132769 |

0.6-fold |

|

Finance income |

203 |

no data |

5048 |

8342 |

41.1-fold |

|

Finance costs |

5703 |

no data |

2981 |

547 |

0.1-fold |

|

Net foreign exchange result |

-3425 |

no data |

8244 |

-12463 |

3.6-fold |

|

Profit before tax |

195276 |

no data |

114651 |

103614 |

0.5-fold |

|

Income tax expense |

36390 |

no data |

27423 |

21967 |

0.6-fold |

|

Tax burden on the tax base |

18.6 |

no data |

23.9 |

21.2 |

+2.6 p.p. |

|

Profit for the period |

158886 |

no data |

91752 |

81647 |

0.5-fold |

|

Net profit margin |

30.6 |

no data |

20.7 |

15.8 |

-14.8 p.p. |

|

Compiled from: PJSC NLMK IFRS data. |

|||||

23 Billionaire Lisin transferred his stake in NLMK from Cyprus to Abu Dhabi. Available at: milliardery/492001-milliarder-lisin-perevel-dolu-v-nlmk-s-kipra-v-abu-dabi (accessed: 20.08.2025).

24 Europe has released NLMK’s steel exports from restrictions: is there anything to be happy about? Available at: (accessed: 20.08.2025).

25 NLMK has maintained its supply regime to Europe and the United States. Available at: article/6244248d9a79474d63f980ed (accessed: 20.08.2025).

26 Analysts have named the companies that will be most affected by EU sanctions. Available at: biznes/459489-analitiki-nazvali-kompanii-kotorye-bol-se-drugih-postradaut-ot-sankcij-es (accessed: 20.08.2025).

Conclusions and discussion

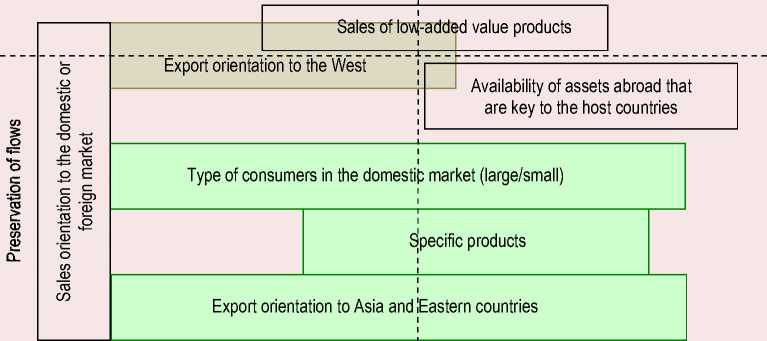

Thus, the factors of sanction impact on the flows within Russia’s ferrous metallurgy supply chains, as presented in the study, have two main dimensions of influence. Their intersection creates four types of consequences (four quadrants in Figure 6 ). The first dimension is related to the very existence of flows and, under the impact of sanctions, determines either the disruption or the preservation of flows. The second dimension is related to the impact on flow volumes, as some flows decreased, while others were either preserved at previous levels or decreased insignificantly.

As can be seen from the framework in Figure 6, the primary quadrant of influence is “Flow preservation – Production capacity reduction”.

The factors contained within it determine the impact predominantly of the first type of sanctions (see Fig. 5), which are associated with reduced demand from the main consumers of metal products. As a result, material flows were preserved but narrowed. Therefore, supply chains that were oriented more towards either domestic market sales or exports to Asia and Eastern countries turned out to be more resilient to external shocks. In a number of cases, alignment with the specified factors allowed flow volumes to be preserved as well, which is particularly evident in sales of specialized (non-commodity) product types. Such shocks had a greater impact on financial flows, which was expressed in a reduction in the sales margin of ferrous metal producers.

Figure 6. A framework of the combined influence of factors on material flows in the supply chains of Russia’s ferrous metallurgy in the coordinates of Flow Existence / Flow Volume

Import supplies of equipment, service, raw materials, etc.

Production capacity reduction

Production capacity preservation (low reduction)

Source: own compilation.

The impact of sanctions belonging to the second type is more ambiguous and manifests when export orientation is toward the West. An important feature is that the non-uniformity of the impact is due to the interconnectedness of this factor with others. Thus, a more significant disruption of material flows occurred. The fact that exports to Europe consisted mainly of low value-added (primary) products also had an influence. However, some flows, related, for example, to specialized (non-commodity) products, were preserved. Vanadium-containing products were not included in the list of prohibited goods. A portion of semi-finished product exports (slabs and square billets) to European plants, which represent key metallurgical production capacities in their respective regions, also continued. A special case is the disruption of flows while maintaining their volumes. This can be explained by the restructuring of these flows from direct supplies to indirect ones via third countries, which process the previously exported raw materials into finished products and ship them to countries that have imposed sanctions.

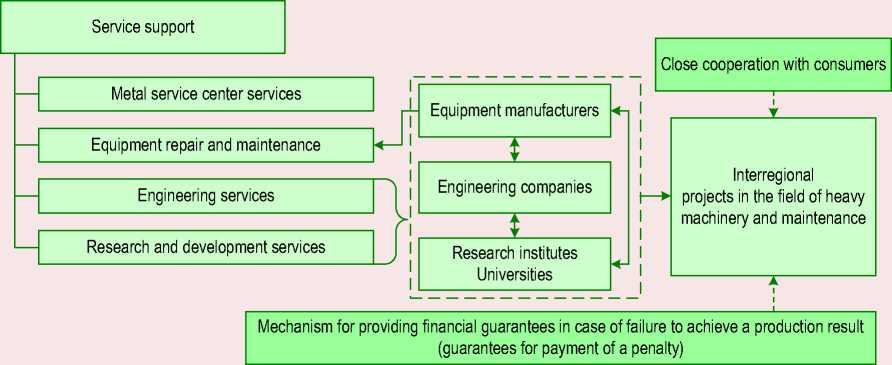

A crucial factor negatively affecting both the existence and the volume of flows was the dependence of Russian metallurgical enterprises on imported supplies of metallurgical equipment and service support. The peculiarity of this factor is that, despite the disruption of material flows, a reduction in production capacity can be expected in the long term as the previously acquired foreign equipment wears out. In the short and medium term, servicing this equipment may become a problem, as foreign suppliers, among other things, have ceased repair and maintenance activities in Russia. Therefore, an important tool for rectifying this situation is the development of projects in heavy machinery manufacturing and a service support system that will include engineering services, research and development services, equipment repair, etc. ( Fig. 7 ).

Figure 7. General framework for comprehensive service support in Russia’s ferrous metallurgy

Compiled from: (Nikolaev, 2010; Khayrullina, 2016; Romanova, Sirotin, 2022); Metallurgy companies seek financial guarantees when ordering domestic equipment. Available at: (accessed: 10.09.2025).

This requires not only developing the activities of enterprises that can replace departed foreign players in the service market (such as the production of specific components and spare parts27), but also forming an integrated system based on the interconnections between scientific institutions, engineering companies, and equipment manufacturers. This system should be oriented towards customer needs and operate within a supportive institutional environment.

This study contributes to the development of applied aspects of the process approach in the industry analysis of supply chains under new challenges. It clearly demonstrates the impact of geopolitical shocks on the distribution of commodity, logistical, financial, and other flows within the supply chains of Russia’s ferrous metallurgy corporations. As part of developing this research direction, we plan to obtain quantitative estimates of the impact of geopolitical shocks on the financial flows of both individual companies and the ferrous metallurgy industry as a whole. Another important prospective direction will be substantiating recommendations for ensuring the adaptability of Russia’s ferrous metallurgy to geopolitical challenges, optimizing logistics chains, reducing risks, and ensuring supply stability under conditions of uncertainty.