Features of operational costs decomposition by carrying out of ship-repair works

Author: Filko S.V.

Journal: Сибирский аэрокосмический журнал @vestnik-sibsau

Section: Экономика

Article in issue: 5 (26), 2009.

Free access

Types of costs decomposition at the ship-repair enterprises are offered, considering individual character of works and allowing improving qualitative characteristics of cost management.

Operating costs

Short address: https://sciup.org/148176085

IDR: 148176085

Text of the scientific article Features of operational costs decomposition by carrying out of ship-repair works

The management of an industrial enterprise on the toughly competitive market and amid the general stagnation of Russian economy demands the revision of approaches to business dealing.

The most important task for the moment is the increase of cost management efficiency. The specified problem gets a special topicality for the domestic ship-repair facilities, because the influence of the world financial crisis has extremely negatively affected the quantity and volumes of services rendered by them.

Russian ship-owners due to the pressure for money have no possibility to carry out full-fledged repair of ships; they postpone it for the vast future, or carry out it abroad. Therefore modern practice of the ship-repair enterprises management should be built on daily work with the expenses, aimed at their optimization that will provide stability of market positions and rise of profitability level.

The efficiency of functioning of the cost control system depends on qualitative and quantitative characteristics of cost information. The method of cost calculation and accounting actually applied at the shiprepair enterprises does not allow to solve the specified problems in complex. Therefore, by working out and improving the cost management system of the ship-repair enterprises, the definition of the cost decomposition method meeting the above-stated requirements is of great importance.

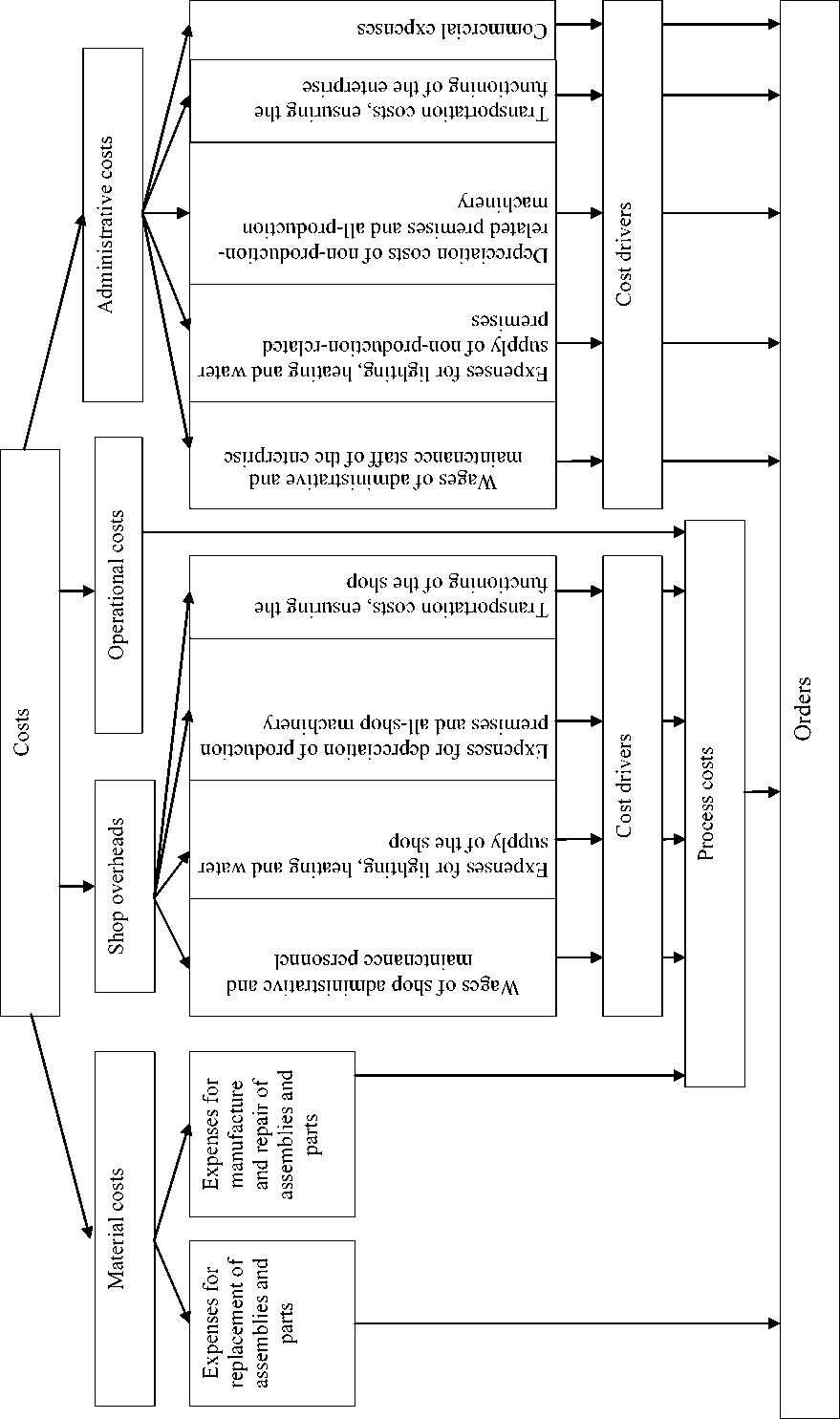

For cost calculation of ship-repair work the following sharing of production costs is proposed which, in our opinion, will considerably expand the possibilities of information processing for management targets: material, operational, shop and administrative expenses (tab. 1).

Thus, material costs are understood as the costs of raw materials, materials, semi-finished products, components, etc. i. e. all that makes the material basis of manufactured products. Material costs arising by renewal or manufacturing of assemblies and details are to be calculated by the processes which are planned and carried out according to repair sheets. If in the frames of ship repair work, the assembly was not restored, but replaced, the given expenses are charged not to the process, but to the order as a whole.

Operational expenses are understood as the cost of the basic technological operations which must be executed for the work (process) completion in full volume. The given expenses include:

-

– wages with taxes of the personnel directly participating in the process;

-

– expenses for the electric power and the fuel consumed by the equipment;

-

– equipment depreciation;

-

– auxiliary materials which can be charged directly to the given process;

-

– expenses for providing of processes with materials and their storage.

Shop overheads include:

-

– wages of shop administrative and support personnel;

-

– expenses for lighting, heating and water supply of the shop;

-

– expenses for depreciation of industrial premises and the equipment not belonging to the machinery, directly participating in the processes;

-

– transport expenses ensuring the shop functioning.

The structure of administrative expenses consists of:

-

– wages of administrative and maintenance staff of the enterprise;

-

– expenses for lighting, heating and water supply of nonproduction-related premises;

-

– expenses for depreciation of non-production-related premises and the equipment, not included into the process and shop equipment;

-

– transport expenses ensuring the enterprise functioning;

-

– commercial expenses.

Shop expenses are allocated on processes and administrative costs directly on fulfilled orders by cost drivers.

A cost driver is the basic indicator of the cost level: for the rent it is the area of the premise occupied by the given employee; for the cost of consumed electric power it is

Table 1

Process-focused cost classification of ship-repair enterprises

By process costing it is advisable to apply the cost decomposition by job specialization. Such breakdown is necessary for accumulation of statistical base by formation of the norms of resources consumption to realize production processes. In the system of standards with the aim of its simplification, the factors considering the characteristics of workplaces are developed. For example, the rate of work done by one welder during the fulfillment of similar works in the shop and directly on the repaired vessel can vary considerably because of different volumes of preparatory work or weather conditions complicating the work fulfillment.

Decomposition of expenses by executors and workplaces is necessary for control of labor productivity level and material consumption by each worker.

Thus, the offered defragmentation of processes will give the possibility for convenient costs distribution by cost centers – production shops.

Besides, it is reasonable to use such kind of decomposition, characteristic for job method of cost accounting, like repair work types and orders. The short substantiation of cost decomposition is given in table 2.

The presented cost decomposition has following advantages:

-

– first, such decomposition draws a parallel between the expenses for manufacture and principal activity types in the process of manufacture, regularizes the allocation of responsibility centers;

-

– secondly, the allocation in separate group of process costs simplifies the control over the productivity of workers;

-

– thirdly, material and process costs have the expressed variable character, therefore such sharing allows to use in the cost management the break-even analysis and directcosting method;

-

– fourthly, such cost sharing allows applying the process-focused approach to the definition of the production cost.

Process as it has been described earlier, is understood as a circuit of interconnected operations (works) on manufacturing of ready-made goods or on rendering of services on the basis of resources consumption.

Taking into account job specialization one allocates production processes which if necessary are split into subprocesses. Subprocesses are understood as process stages, the process components characterized by the availability of a certain intermediate result and representing a circuit of works and operations.

In order to separate basic subprocesses from technology of ship-repair works, it is necessary to define, what criterion is to be used for cost decomposition. For process-focused costing the basic criterion of optimal decomposition is such splitting of technology of ship-repair works by which the separated parts – subprocesses would have the least degree of cost variability per time unit of process for different work types and objects of repair. In this case the repair sheets which are cost calculations in the ship-repair enterprises, calculated on the basis of the addition of the cost of the number of processes included in these sheets, adequately reflect the cost of each order, regardless the type of repaired vessel and repair work type.

Characteristic feature of the ship-repair facility is the big nomenclature of works. However they can be grouped into such work sets which are identical for any type of a repaired vessel and kind of repair. The differences between each specific repair order consist only in selection of these sets of processes, and the use of each specific process. So, for example, the replacement of the set for the ships under projects 866 and р-14Аisequaltothecostofanhourof works, both for interim overhaul, and for current repair.

So, the works meeting the specified requirements can be grouped inside of one process, in this case the requirements of the decomposition criterion formulated earlier, will be observed even in case of various disproportionate changes of the price of one hour of operation of each unit involved into the process.

At the ship-repair facilities of Krasnoyarsk region which are carrying out the majority of ship-repair works themselves, it is reasonable to allocate following processes:

Table 2

The Substantiation of cost decomposition

|

Decomposition type |

Decomposition purpose |

|

By orders |

The control of use of cost limit by each object of repair |

|

By types of repairs works |

For reception of the statistical information necessary for short-term and intermediate-term costs planning |

|

By processes |

Simplification of monitoring tasks, short-term and intermediate-term costs planning, fixing of production costs to the cost centers (shops) |

|

By subprocesses |

Increase of degree of costs controllability due to decrease of percentage of indirect (distributed) expenses. Harmonization and perfection of business processes of the enterprise to achieve more effective usage of the enterprise resources. The control of completion percentage for works planned in repair sheets, the possibility of comparison of actual expenses on each point of the repair sheet with the standards |

|

By job specialization |

For working out and specification of cost standards of processes |

|

By workplaces |

Application of the correction factors increasing standard labor inputs of the process depending on work conditions, the control of usage efficiency of the equipment |

|

By executors |

The control of working hours efficiency for each executor. Responsibility personification on effective use of resources |

Fig. 1. Diagram of process-focused costs allocation of the shop-repair enterprise

-

– repair of the ship hull and deck erections;

-

– repair of engines;

-

– repair of ship auxiliary mechanisms;

-

– repair of electrical and radio equipment;

-

– repair of ship systems;

-

– the interior outfitting;

-

– gleaning, painting, insulation works.

It allows providing the route of ship-repair works. The task of monitoring of the level and structure of costs becomes simpler. For each of the specified processes one can deduce by statistical way the factors of ratio of different material inputs to labor input. So, for example, in the process cost structure of the interior outfitting, cleaning, painting, insulation works, prevail the expenses for remuneration for labor. The most material-intensive are repair of the ship hull and deck erections and repair of engines. In the first of the specified processes the expenses for metal products dominate, in the second – for spare parts for the equipment.

In case of application of the offered process cost management system the structure of ship-repair works looks as follows (fig. 2).

Hull preparation works

Preassembly and welding

Hull repair on the stocks

Set replacement and welding of sections

Г Preparation of Diesel engines to repair

Repair of base frames and cylinder blocks

Repair of crank shafts

Repair of piston rods

Repair of cylinder liners and pistons

Repair of eccentric shaft and cam plates

Repair of friction bearings

Repair of fuel-feed pumps

Repair of nozzles

Assembly of parts of connecting rod and piston group

Repair of propeller pump

Repair of cog wheel pump

Repair of anchor windlass and of winch

Repair of steering engine and steering arrangement

Repair of ground tackle, docking device, tow gear and boat gear

Repair of shaft lines, propulsion devices and buzzers

Repair of electrical system

Repair of ship radio outfit

Repair of heat-exchange apparatus

Manufacture and repair of metal pipe-lines

Metal pipe laying

Plastic and polypropylene pipe laying

Repair of wirework and wiring

Finishing of ship premises

Repair of wooden deck sheathing

Coating of the deck and the floor of ship premises

Cleaning

Filling and primary painting Painting

Fig. 2. The structure of ship-repair works

The offered cost decomposition gives the possibility to realize the process-focused approach to cost controlling, it makes possible the analytical processing by orders, by types of repair, by production processes, by subprocesses, by job specialization, by workplaces and executors.

Today implementation of the process organization of management in different forms takes place at Public Corporation “Novorossiysk ship-repair factory”, Federal State Unitary Enterprise “Admiralteyskiye verfy”, Public Corporation SRK “Sevmorsudoremont”. The employees of all above-stated enterprises noted positive administrative effect, but it is necessary to say that management techniques used at these factories, are focused, mainly, on optimization of processes, improvement of their quality. The cost management is considered as auxiliary, derivative function. Within the offered process-focused approach, conversely the main objective is first of all the production cost management, and the process decomposition is the basis of this system allowing achieving more effectively of assigned administrative tasks.

Krasnoyarsk State Trade and Economic Institute, Russia, Krasnoyarsk

PRINCIPLES AND METHODS OF CONSTRUCTION AND FUNCTIONINGOF SERVICE ENTERPRISE’S MANAGEMENT SYSTEM IN MARKET CONDITIONS

Principles of construction and functioning of management system by the enterprise of service sphere in conditions of the market, are considered. The model of relationships between causes and effects, reflecting influence the administrative actions on business-processes, that maintenances the appeal offirm S services is presented. The technique of estimation of quality of management system by the service firm is resulted.

Development of integration processes in the economy and interconnections between the territories implies a high level of services and trade as a link economic mechanism. The prospects of growth of volumes of services make this sector very attractive for investment and the application of entrepreneurial activity. Obviously, the businesses which whose services are consistent with international quality standards and have high value to consumers, the benefits of its acquisition will reach this market and build on it the positions.

Analysis of the problems of improving the system of enterprise management services showed that, firstly, the needs of formation and development of quality management on aggregate characteristics are currently neglected. Secondly, existing approaches to understanding the quality of company management is not fully focused on particular services. As a result, enterprise management services often fail to ensure the receipt of the required result – services that meets the requirements of consumers in all components. In the end, when the current high level of competition in the consumer market, reduce business risk or lose the main competitive advantage – the quality of services offered. Third, when evaluating and designing management systems company does not take into account the effect of quality management on service quality which makes following conversion of resources in the process of outlet to receive services demanded by consumers, as at present, as well as strategically.

It should be noted that much attention in research and publications are focused on such areas of knowledge, as an efficient and competitive management, quality control, while the quality of the management system note only a few scientists. At the same time, considering the dependence of the quality of the nature of management processes, it may be noted that not all areas were adequately covered in the research.

Analysis of existing approaches to improve the management showed that they did not fully take into account the need for quality control as a condition for improving services, reducing the possibility of designing an integrated management system in the context of three dimensions: efficiency, competitiveness and quality. Developed methodical, organizational and economic approaches in order to improve the enterprise management services that improve quality, must take into account the specific characteristics of the management object and provide better services and more fully satisfy the demand.

To solve the above-mentioned problems should be developed theoretical and methodological position to improve governance, to reflect better the characteristics of service industries and the need to improve the quality of services offered on the market. This led to the relevance of research performed, the object of which were service industries, operating in market conditions. Subject of study – management relations arising in the functioning and development of service industries.

The existing conditions of service are aiming to improve the quality of management in improving the business management system that is essential to increase the quality of the services market to the changing needs of clients. Achieving