Reducing the cost of production of a metallurgical enterprise

Author: Zharova A.O., Zharikova E.G.

Journal: Экономика и бизнес: теория и практика @economyandbusiness

Article in issue: 11-1 (117), 2024.

Free access

A theoretical study of the methodological aspects of cost formation, including the types and structure of cost is discussed. The analysis and assessment of the current state of the financial situation in PJSC RUSAL Bratsk is carried out, the company’s activities and its financial and economic indicators are described, the problems and advantages of the company are identified. Recommendations are developed contributing to reduction of production cost.

Cost, types of cost, shop cost, production cost, total cost

Short address: https://sciup.org/170207929

IDR: 170207929 | DOI: 10.24412/2411-0450-2024-11-1-128-133

Снижение себестоимости продукции металлургического предприятия

Проведено теоретическое исследование методических аспектов формирования себестоимости, включая виды и структуру себестоимости. Проведен анализ и оценка текущего состояния финансового положения в компании ПАО «РУСАЛ Братск», описана деятельность компании и ее финансово-экономические показатели, выявлены проблемы и достоинства компании. Разработаны рекомендации, способствующие снижению себестоимости продукции.

Text of the scientific article Reducing the cost of production of a metallurgical enterprise

Cost is one of the main indicators affecting the efficiency of the company's economic activities. An exceptionally detailed cost analysis enables to identify reserves for its reduction and to classify the ways to increase the final results with minimal labor, materials and finance. In addition, cost is the basis of pricing and affects the profit and financial performance of the enterprise. Thus, cost is of great importance for the development of the enterprise.

The relevance of the research topic implies the purpose of the work: to propose measures aimed at reducing the production cost at PJSC RUSAL Bratsk.

To achieve the research, aim the following objectives are required to be solved:

-

1) discussion of the theoretical aspects of the formation of the production cost, including the definition of its essence and types;

-

2) comprehensive analysis of the production cost at PJSC RUSAL Bratsk;

-

3) development of measures aimed at reducing the production cost at PJSC RUSAL Bratsk.

The object of the study is the public joint stock company RUSAL Bratsk, whose main activity is aluminum production.

The subject of the study involves the annual financial statements of PJSC RUSAL Bratsk for 2020-2023.

In the scientific and professional literature, the concept of cost is fundamental especially in terms of optimizing the cost at an enterprise. It has been considered by many domestic and foreign economists (Kalmes A., Harrison Ch., Leon Sey J., Rudansky S.V. and others).

-

1) Shop cost is the cost of the shop, which is directly related to the production of products, consisting only of direct production costs. It includes the cost of raw materials, material supplies, components, labor resources and expenses directly related to the production process.

-

2) Production cost includes shop cost, overall production and overall economic expenses.

Overall economic expenses are expenses that are not directly related to the production process, they are determined by the needs of management activities. They integrate administrative and managerial expenses; payment for information, audit and consulting services; depreciation and repair costs of fixed assets, as well as other similar management costs.

Overall production costs are associated with the maintenance of the main production and management of departments, workshops and sectors. They comprise depreciation of fixed assets in the industry, costs of occupational safety and health measures, wages and social contributions of employees of the administrative apparatus of divisions and departments, transportation costs and other costs associated with sectors servicing the main production.

-

3) The total cost price reflects all costs of production and sale of products, calculated by summing production costs, sales costs and nonproduction costs. The indicator enables to estimate the total cost of production [2].

Sales expenses are the monetary costs of material, labor and other types of resources of trade organizations for the provision of products to the final consumer. They include the costs of storage, delivery, performance of works, provision of services, purchase and sale of goods, research and development and other costs associated with the production and sales processes [3].

Non-production costs are the costs of an organization that are not related to the production of products. Non-production costs comprise payment for labor downtime; overtime surcharges, excess losses from rejects; losses from rejects and damage to materials; losses incurred from writing-off under-amortization of fixed assets; fines paid to other organizations; losses from writing-off bad debts, etc. [4].

Calculating different types of costs allows companies to analyze the list of expenses more accurately, make informed and effective decisions and improve business processes, as Lvutin P. E. emphasized in his research [5].

The list of costs that form the production cost, when accounting is divided into groups in accordance with the economic elements and calculation items. The nomenclature of elements and articles makes up the cost of production, and the cost structure reflects the ratio of these elements and articles as a percentage of the total cost.

The calculation articles are used to generate the cost of various types of products. The list of articles is determined for each industry sector, taking into account the specifics of technology and organization of production.

The calculation articles in a generalized form represent:

-

1) raw materials and supplies;

-

2) fuel and energy for technological purposes;

-

3) accrued wages to production workers;

-

4) insurance premiums from the wages of production workers;

-

5) overall production expenses;

-

6) overall business expenses;

-

7) other production expenses;

-

8) commercial expenses.

The distribution of costs by calculation items permits to identify specific objects and origin of costs, calculate the cost of a production unit, as well as to estimate profit, profitability of products and production.

In the course of the study, the cost of production of a metallurgical enterprise was analyzed using the example of PJSC RUSAL Bratsk. Public Joint Stock Company RUSAL Bratsk Aluminum Plant is the largest aluminum plant in Russia and one of the leading aluminum producers in the world. The Company produces 30% of all Russian aluminum and 5.5% of the world's. The company is part of the RUSAL Aluminum Company [6].

Tables 1-2 below show the shop production cost at PJSC RUSAL Bratsk by stages of the technological processes for 2022-2023.

The conversion is a complex of technological processes that ends with the creation of an intermediate product (semi-finished product), which is then transferred to the next stage, where it undergoes additional processing and acquires new properties. As a result, the finished product is ready at the last stage. In such production, production costs are recorded separately for each stage.

Table 1. Shop cost of production at PJSC RUSAL Bratsk by stages of the technological process for 2022 [7, 8]

|

Name |

Cost of 1 ton, rub. |

Including by cost items, % |

||||

|

Raw materials |

Energy costs |

Wages |

Depreciation |

Workshop expenses |

||

|

Raw aluminum |

115,002.4 |

53.7 |

33.4 |

3.7 |

1.4 |

7.9 |

|

Foundry (cost excluding raw aluminum) |

4,571.7 |

49.1 |

5.7 |

16.6 |

3.2 |

25.5 |

|

Cryolite mixed |

25,047.0 |

47.5 |

18.8 |

5.2 |

1.0 |

27.5 |

|

Anode mass |

26,800.0 |

94.5 |

0.2 |

0.4 |

0.1 |

3.5 |

|

Calcined coke |

13,529.1 |

91.1 |

0.8 |

1.3 |

0.4 |

6.5 |

Table 2. Shop production cost at PJSC RUSAL Bratsk by stages of the technological processes for 2023 [9, 10]

|

Name |

Cost of 1 ton, rub. |

Including by cost items, % |

||||

|

Raw materials |

Energy costs |

Wages |

Raw materials |

Workshop expenses |

||

|

Raw aluminum |

150,081.0 |

6.8 |

28.4 |

2.9 |

1.6 |

6.2 |

|

Foundry (cost excluding raw aluminum) |

3,549.0 |

32.6 |

7.3 |

22.1 |

5.1 |

32.8 |

|

Aluminum DEOX |

173,684.2 |

75.7 |

0.4 |

3.2 |

0.6 |

20.1 |

|

Cryolite mixed |

25,421.5 |

54.9 |

17.5 |

5.3 |

1.1 |

21.2 |

|

Anode mass |

28,587.7 |

95.9 |

1.4 |

0.4 |

0.2 |

2.6 |

|

Calcined coke |

14,461.4 |

90.1 |

0.7 |

1.3 |

0.3 |

6.0 |

Analysis of the data in the tables enables to conclude that overall, the shop cost in 2023 increased by 114.0% (210,834.6 rub) compared to 2022, since the company decided to recycle aluminum waste through remelting slags and scrap aluminum products in 2023.

In 2023 in the production of raw aluminum as part of the shop cost, the costs of raw and basic materials (60.8% or 91,249.2 rub) and energy costs (28.4% or 42,623.0 rub) had a greater share in the production of raw aluminum. In 2023 relative to 2022, the costs of raw materials and production materials increased by 7.1% (29,493.0 the share of energy costs decreased by 5.0%, but at the same time the cost increased by 4,212.2 rub.

In 2023 the cost of raw materials (32.6% or 1,157.0 rub) and workshop costs (32.8% or 1,164.1 rub) have a greater share in the cost of foundry conversion (excluding the cost of raw aluminum). In 2023 compared to 2022, the cost of raw materials decreased by 16.5% (-1,087.7 rub.), and the share of shop expenses as a part of the shop cost increased by 7.3%, while the cost decreased by 1.7 rub.

In 2023 PJSC RUSAL Bratsk started the production of secondary aluminum DEOX, in the cost of which the costs of raw materials and sup- plies had a greater share (75.7% or 131.5 rub) and workshop costs (20.1% or 34,910.5 rub).

In 2023 in the production of cryolite, the costs of raw materials and production materials (54.9% or 13,956.4 rub) and shop costs (21.2% or 5,389.4 rub). In 2023 compared with 2022, the cost of raw materials and production materials increased by 7.4% (2,059.1 rub), and shop costs decreased by 6.3% (-194.7 rub).

In 2023 in the production of anode paste, the costs of raw materials have a bigger share (95.9% or 27,415.6 rub), compared to 2022. In 2023, raw material costs increased by 1.4% (2,089.6 rub). In the production of calcined coke, the costs of raw materials had a bigger share (90.1% or 13,029.7 rub). In 2023 compared to 2022, the share of raw material costs decreased by 1%, whereas the cost increased by 704.7 rub.

Thus, in the enterprise the share of total costs of material, energy and fuel costs occupies a big part of production costs. This mean that production is material-intensive and energy-intensive, and also has significant workshop costs, which include the costs of routine repairs of buildings and structures, maintenance costs of buildings and structures, safety costs and other expenses, which is typical for non-ferrous metallurgy enterprises.

Table 3. Dynamics of the cost of listed products at PJSC RUSAL Bratsk for 2020-2023, % [7-10]

|

Name |

2020 |

2021 |

2022 |

2023 |

Change in 2022 to 2023, % |

|

Expenses per ton, rub. |

109,190 |

117,930 |

152,225 |

189,100 |

24.22 |

|

Cost structure, including: |

100 |

100 |

100 |

100 |

|

|

- energy consumption |

30.1 |

29.1 |

26.1 |

24.2 |

-1.90 |

|

- alumina |

35.8 |

38.5 |

44.4 |

39.3 |

-5.10 |

|

- raw materials |

12.4 |

13.4 |

13.7 |

13.8 |

0.10 |

|

- wages |

4.1 |

4.7 |

4.9 |

4.1 |

-0.80 |

|

- repairs |

3.7 |

3.9 |

4.6 |

3.8 |

-0.80 |

|

- investment costs |

1.5 |

1.9 |

1.3 |

1.8 |

0.50 |

|

- major repairs |

2.9 |

3.1 |

2.8 |

2.3 |

-0.50 |

|

- transportation costs |

4.5 |

5.7 |

3.4 |

2.9 |

-0.50 |

|

- management expenses |

1.3 |

1.3 |

0.1 |

0.0 |

-0.10 |

|

- other |

3.7 |

-1.7 |

-1.2 |

7.7 |

8.90 |

According to the table, it can be concluded that the following items of expenditure have the biggest share in the cost of production in 2023 at PJSC RUSAL Bratsk: the cost of buying alumina (39.6% or 74,316.1 rub), energy costs (24.2% or 45,762.1 rub), the cost of purchasing raw materials (13.8% or 26,095.7 rub). In 2023 compared with 2022, the items such as the cost of buying alumina had a noticeable change, namely, a reduction in the specific gravity by 5.10%, electricity by 1.90%, and an increase in the specific wait of other expenses as part of the cost by 8.90%, the remaining expenditure items had small changes towards a decrease in the specific wait. However, in general, the cost in 2023 increased by 24.22% (36,874.0 rub) compared to 2022, which is due to an increase in other expenses, an increase in the cost of alumina, raw materials and negative exchange rate differences.

In conclusion, several measures have been proposed to reduce the production cost at the manufacturing enterprise.

Firstly, in order to reduce the production cost at any industrial enterprise, it is necessary to identify the main directions for its reduction, which are presented below. This involves improvement in the technical equipment of production. The use of innovative, more advanced technologies, mechanization and maximum automation of production processes certainly contribute to reducing costs and achieving set goals.

The second direction relates to raw materials and supplies. It is necessary to study scientific and technical achievements and analyze the impact of the best practices of enterprises in the non-ferrous metallurgy industry on the level of total costs.

To find ways to reduce costs, it is necessary to optimize the organizational structure of the company and the production process. It is important to identify key aspects that will help to achieve maximum efficiency of the enterprise, such as:

-

1) organization of the main production process, including technical preparation of production and continuous quality control of products.

-

2) maintenance of the main production process, including monitoring the continuity of supplies to the main workshops and monitoring the condition of material support, the level of reliability of tools, energy and repair shops.

-

3) the work of all departments of the enterprise, including effective personnel management, control of economic and financial activities, analysis and use of information, activities of the management directorate, high-quality production management and other aspects.

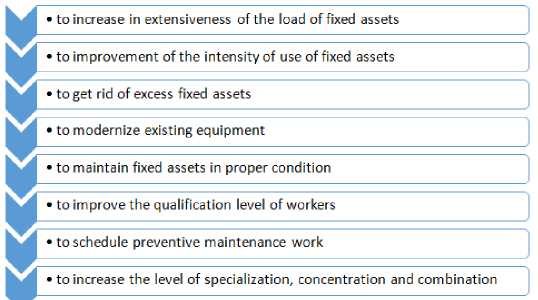

Turusov S.N. believes that it is necessary to develop automated management systems and introduce modern computer technologies to reduce the cost of products and improve the efficiency of the organization. The possibility of upgrading and improving existing equipment and technologies should also be considered. Measures that can be taken to improve production efficiency shown in figure 1.

Figure 1. Measures to improve production efficiency

Reducing the material consumption and labor intensity provides great opportunities for the organization in terms of reduction of the production cost. Reduction in transportation costs and optimizing logistics provide reduction of material consumption.

When analyzing costs, it is important to consider the share of unproductive costs in the cost structure. These include damage and loss of material assets, fuel and energy consumed during downtime and remuneration of downtime. It is also worth paying attention to the common problems of production rejected items.

References Reducing the cost of production of a metallurgical enterprise

- Vershinin O.E. What is the cost price and how to calculate it / O.E. Vershinin // Neiros. - 2022. - URL: https://neiros.ru/blog/business/chto-takoe-sebestoimost-i-kak-ee-schitat/(date of application: 22.09.24).

- Piperkova M. G. How to calculate the cost of production / M.G. Piperkova // Yandex Market blog. - 2023. - URL: https://partner.market.yandex.ru/blog/finance-on-marketplaces/sebestoimost-tovara/(date of application: 22.09.24).

- Galevsky, G.V. Metallurgy of aluminum. Technology, power supply, automation: a textbook / G.V. Galevsky, N.M. Kulagin, M.Ya. Mintsis, G.A. Sirazutdinov. - 4th ed. - Moscow: Flint, 2017. - 529 p. ISBN: 978-5-9765-0316-8

- Bondina, N.N. Cost accounting and cost calculation: a textbook / N.N. Bondina, I.A. Bondin, I.V. Pavlova, O.V. Lavrina. - Moscow: INFRA-M, 2023. - 254 p. - (Secondary vocational education). ISBN: 978-5-16-013932-6

- Galevsky, G.V. Metallurgy of aluminum. Technology, power supply, automation: a textbook / G.V. Galevsky, N.M. Kulagin, M.Ya. Mintsis, G.A. Sirazutdinov. - 4th ed. - Moscow: Flint, 2017. - 529 p. ISBN: 978-5-9765-0316-8

- Lvutin P.E. Cost price what is it? / P.E. Lvutin // Yandex Practicum. - 2023. - URL: https://practicum.yandex.ru/blog/chto-takoe-sebestoimost-chto-v-nee-vhodit-i-kak-ee-rasschitat/(date of application: 22.09.24).

- Annual Report of the Public Joint Stock Company Bratsk Aluminum Plant (PJSC RUSAL Bratsk) for 2020 approved on 30.06.21 № 186 // PJSC RUSAL Bratsk: [website]. - URL: https://braz-rusal.ru /(date of reference: 31.05.24).

- Annual report of Public Joint Stock Company Bratsk Aluminum Plant (PJSC RUSAL Bratsk) for 2021 approved on 30.06.22 № 217 // PJSC RUSAL Bratsk: [website]. - URL: https://braz-rusal.ru /(date of application: 31.05.24).

- Annual report of Public Joint Stock Company Bratsk Aluminum Plant (PJSC RUSAL Bratsk) for 2022 approved on 29.05.23 № 247 // PJSC RUSAL Bratsk: [website]. - URL: https://braz-rusal.ru /(date of issue: 31.05.24).

- Annual report of Public Joint Stock Company Bratsk Aluminum Plant (PJSC RUSAL Bratsk) for 2023 approved dated 05.03.24 № 282 // PJSC RUSAL Bratsk: [website]. - URL: https://braz-rusal.ru /(date of application: 31.05.24).