Impact of audit committee characteristics on earnings management in Nigerian listed consumer goods firms

Author: Olabisi Jayeola, Kajola Sunday Olugboyega, Owoeye Segun Daniel, Agbatogun Taofeek Osidero

Journal: Вестник Волгоградского государственного университета. Экономика @ges-jvolsu

Section: Финансы. Бухгалтерский учет

Article in issue: 1 т.24, 2022.

Free access

This study assessed the impact of audit committee characteristics on earnings management of Nigerian listed consumer goods firms. The study adopted a correlational research design using secondary data extracted from the financial statement of selected 10 firms from 2010 to 2019. The selected firms were from 21 listed consumer goods firms listed in Nigeria as of 2019 using a judgmental sampling technique based on the availability of data. Correlation analysis, Unit-root test, Ordinary Least Squares (Fixed effects) regression were the statistical tools used for analysis with the aid of E-views Software, version 10. The study revealed a significant and negative relationship between Audit Committee Meetings, Audit Committee Size, Leverage, and Earnings Management (P 0.05). The study concluded that firms with adequate audit committees attribute moderate earnings management practices. The studysuggested that shareholders and regulatory bodies should ensure adequate and effective audit committee structure.

Audit committee meeting, audit committee size, audit committee financial expertise, audit committee independence, earnings management

Short address: https://sciup.org/149140087

IDR: 149140087 | UDC: 338.515:658(669)

Влияние комитета по аудиту на управление доходами в нигерийских компаниях, торгующих потребительскими товарами

В статье на основе проведенного исследования оценивается влияние аудиторского комитета на управление доходами нигерийских компаний, производящих потребительские товары. В исследовании был проведен корреляционный анализ с использованием вторичных данных, извлеченных из финансовой отчетности выбранных 10 фирм за 2010-2019 годы. Данные фирмы выбраны из 21, зарегистрированных в Нигерии по состоянию на 2019 г., с использованием метода субъективной выборки, основанного на наличии данных. Корреляционный анализ, критерий единичного корня, регрессия методом наименьших квадратов (фиксированные эффекты) были статистическими инструментами, использованными для анализа с помощью программного обеспечения E-views, версия 10. Исследование выявило значительную отрицательную взаимосвязь между частотой заседаний комитета по аудиту, численным составовом комитета по аудиту, кредитным плечом и управлением прибылью (Р 0,05). В ходе исследования выявлено, что фирмы с адекватными комитетами по аудиту осуществляют умеренную практику управления доходами. В исследовании был сделан вывод о том, что акционеры и регулирующие органы должны обеспечить надлежащую и эффективную структуру комитета по аудиту.

Text of the scientific article Impact of audit committee characteristics on earnings management in Nigerian listed consumer goods firms

DOI:

The urge to meet up with the projected earnings target motivates managers at various managerial levels to put pressure on accountants, auditors, and others to conceal the truthful position of the organization’s state of affairs. However, this unethical practice has inflicted a lot of havoc on companies all over the world. Earnings management is an attempt on the part of management to maximize management’s interest.

Earnings management suffices when managers use unscrupulous means to structure transactions to alter financial reports and misleading stakeholders about the economic performance of the company.

The alarming rate of corporate failures and accounting scandals has given attention to various ways of manipulating books of accounts despite regulations put in place to confront this unethical behaviour. Corporate scams and financial reporting malpractices are not restricted to any particular country. For example, Bala and Kumai [2015] posit that Nigeria has received its share of financial reporting failure. Companies such as Cadbury Nigeria Plc, Afri Bank Nigeria Plc, and Intercontinental Bank Plc faced the problem of financial reporting scandal in 2009. However, the regulatory bodies in most countries have put in place regulations, standards, and practices that address corporate governance and financial reporting anomalies and significantly improved ethical practices in the corporate environment. In Nigeria, the regulatory authorities confronted this malaise by compelling companies to conform to corporate governance codes with sanctions laid out for deviants.

Nigeria has put in place several codes of corporate governance with distinctive dissimilarities namely; the Security and Exchange Commission (SEC) code of corporate governance 2003 to guide the operation of public companies listed on the Nigerian Stock Exchange. In addition, Central Bank of Nigeria (CBN) code of 2006, National Insurance Commission (NAICOM) code of 2009. As pointed out, every public limited liability company is required to mount an audit committee under sections 358 (3) and (4) of the CAMA. The board must ensure that the audit committee undertakes its statutory duties as specified, and at least one board member of the committee should be financially knowledgeable and where necessary seek professional advice from experts.

The audit committee promotes the integrity of financial reports and lessens the audit risk, which in turn improves the quality of reported figures [Contesotto et al., 2013]. The audit committee subsumes in the board and ensures the accuracy and reliability of the financial statements presented by management. The audit committee is liable for any anomaly in accounting information because the audit committee is expected to provide oversight functions on the financial reports of an organization. Although companies may comply with the regulatory requirements to avoid disciplinary actions, efforts are exerted to supervise the effectiveness of the audit committee to ensure that financial statements are fairly stated, and free from all forms of manipulation.

Bala and Kumai [2015] posited that for quality financial reporting to be achieved, a monitoring committee should be in place as an ombudsman that ensures firms produce relevant and reliable information that protects the existing and prospective investors’ interests. The audit committee is one of the most important watchdogs that minimize the possibilities of unethical accounting practices. It reviews audited and unaudited financial statements of an organization, thereby improving the quality and reliability of the financial statement. The independence of the audit committee provides a key factor to the effectiveness of the committee. Olabisi, Kajola, Abioro, and Oworu [2020] submit that an auditor who requires independence and protection to carry out the assignment without fear of coercion by the management must have unhindered access to the organization’s books, and report thereon without fear of those whose interest may conflict with auditor’s opinion.

Various studies conducted on audit committee characteristics have provided mixed opinions on the direction of association [Nelson et al., 2012]. This has inspired this study to determine the possibility of audit committee characteristics to reduce earnings management in different economies. This further demands the need to explore the likely impact of audit committee characteristics on earnings management of Nigerian listed consumer goods firms. Considerable studies have been conducted in the conglomerate sector and financial sector. Several studies have examined the effect of the existence of an audit committee on organizational performance. However, this has driven this study to examine audit committee characteristics rather than audit committee existence in Nigerian listed consumer goods firms. Consequent to this, the main objective of this study is to examine the effect of audit committee characteristics on earnings management of Nigerian listed consumer goods firms. The specific objectives are to:

-

1) assess the impact of audit committee size on earnings management of Nigerian Listed Consumer Goods Firms;

-

2) evaluate the extent to which audit committee financial expertise affect earnings management of Nigerian Listed Consumer Goods Firms;

-

3) assess the effect of audit committee independence on earnings management of Nigerian Listed Consumer Goods Firms; and

-

4) examine the impact of audit committee meetings on earnings management of Nigerian Listed Consumer Goods Firms.

The second part of the paper dealt with the conceptual and empirical review. While part three enumerated the research methods adopted, the fourth section presented the results of the study and the last part discussed the findings, provided conclusions, and made recommendations.

Literature Review Conceptual Review

The members of the audit committee are part of the board of directors formulating strategies to improve the financial health of the firm. Ayinde [2002] describes audit committee as a standing committee with responsibility of improving the credibility of financial statement by liaising with internal auditors and management. This ensures good conduct of corporate responsibility that conforms to accepted ethical and legal standards. The audit committee’s role is crucial to every organization because it examines the auditors’ report, makes recommendations, and performs an oversight function on financials. It monitors accounting policies, external auditors, and makes sure that regulatory compliance is complied with, and discusses risk management policies with management. The committee has the authority to initiate special investigations in cases where it is suspected that accounting practices are violated or perceived to be problematic. The audit committee maintains a good communication level with the organization’s Chief Financial Officer (CFO) and Controller in other to give recommendations and advice to the board. This may lead to a review of the scope and planning of audit requirements to include the suspected aspects.

The audit committee size is the total numbers of directors appointed in line with the stipulated law not exceed the stipulated numbers. In Nigeria, the Companies and Allied Matters Act, 2004 as amended, requires every public limited liability company to appoint an audit committee of seven shareholders and not directors of the company. The appointed members are expected to be conversant with basic financial statements. The size of the audit committee determines the quality of financial reports because larger audit committees may have advantage of a wider knowledge-based and varied expertise; thereby undertake their role effectively [Vafeas, 2005].

Audit committee independence implies that its members do not have any relationship with the management of a company alongside no influence from any of the majority shareholders, officers, and executive directors of the company on the audit committee [Ibrahim, 2016]. The role of the audit committee is to certify the quality of financial reporting, which in turn reduces the level of earnings manipulations. The act imposes obligations on independent audit committee to be in charge of monitoring the financial reports [Klein, 2002]. The audit committee’s role will be eroded if independence is absent or the audit committee activities are influenced by members outside the committee.

Audit Committee meetings are essential as various critical matters concerning the financial statement, strengthening of the internal control system, and fraud prevention strategies are discussed in the meetings. This will ensure that members are up to date with happenings in the organization and apt in tackling them as they arise. An audit committee that meets frequently can reduce the possibility of earnings management [Abbott et al., 2004]. Bryan, Liu, and Tiras [2004] posited that an audit committee that meets regularly is expected to monitor tasks more effectively than an audit committee that seldom holds meetings. In a firm where the audit committee meets regularly, earnings management is less likely to be operational [Xie et al., 2003; Vafeas, 2005].

The audit committee is expected to be made up of shareholders with considerable knowledge in finance and accounting as this is important to even assess better the tricks or misstatements that may have occurred in the organization’s book. Without having financially literate members, it may not be easy to oversee the financial report process which is important in establishing good corporate governance. Audit committee financial expertise is expected to reduce corporate fraud [Abbott et al., 2004]. The effect of audit committee financial expertise on earnings management will also be expected to increase due to the relatively high status of the audit committee relative to management.

Earnings management is an unethical way of using accounting knowledge to overly present a positive view of the company’s earnings done by structuring transactions to alter financial reports in a shameful way to cover up their inability to meet up with the predetermined target which in turn misleads stakeholders of the organization that the economic performance of the organization has been on the good side and also serves as a way to affect the decisions of users of financial information. Earnings management at times is not willingly carried out by the accountants who know the inherent risks associated with such practices but many succumb to the threats and pressures by the top officers to deliberately mislead the users of their financial information to override the ethical principle of Integrity, Objectivity, Professional competence and due care, professional behavior.

Theoretical Review

The study found agency theory more relevant to underpin this study on audit committee structure which functions as a monitoring mechanism and watchdog that reduces agency costs [Menon et al., 1994].

Agency theory provides a contextual appreciation of the alignment of information asymmetry that influences managers’ decisions. Agency theory predicts behaviour when a principal delegates work to an agent with the expectation that the agent will undertake the assignment in the best interest of the principal [Jensen et al., 1976; Eisenhardt, 1989]. A company is a network of bonds comprising group of suppliers, bankers, customers, employees, and each group makes certain contribution to the company at a sacrifice. The task of a manager is to coordinate these groups to achieve low price for goods supplied, high price for goods sold, low interest rates for loans obtained, high share prices, and affordable wages. In these chains of relationships, the manager is the agent, who tries to obtain maximum benefits for the principal.

The agency theory simply highlights the fact that the audit committee is in existence to perform some duties on behalf of or for the good of the users of the entity’s financial information. Since managers (agents) may mislead the shareholders (principals) using earnings management to distort the image of the organization’s financial status, the audit committee (agents) would be set up to checkmate the activities of the managers and other units to ensure an honest representation of the financial reports.

Previous Studies

Several researchers have conducted series of researches which have resulted in different opinions and results.

Juhmani [2017] examined audit committee characteristics and earnings management: the case of Bahrain. The study covered Bahrain-listed companies on Bahrain Bursa from 2012 to 2014. The proxies for audit committee characteristics were audit committee independence, audit committee size, audit committee meetings, and audit committee financial experts while discretionary accruals were used to measure earnings management. A multivariate regression model was used to determine the relationship between audit committee characteristics and earnings management. The results showed that audit committee size and financial experts have a negative and significant association with discretionary accruals. However, there was an insignificant relationship between audit independence, audit meeting, company size, and earnings management. The study suggested that an oversight function is to be performed by an audit committee to moderate earnings management practices and the financial reporting process should be adequate to provide useful information about the earnings management to the users of accounts and regulatory authorities.

Siagian and Siregar [2018] examined the effect of audit committee financial expertise on earnings management. The sample adopted was 384 observations from the listed Indonesia Stock Exchange from 2012 to 2014. The study used descriptive statistics and regressions models for the analysis. Audit committee experience in accounting, supervision, and financial audit committee status were used to proxy for audit committee financial expertise. The study found that audit committee financial expertise has a positive effect on income decreasing accruals. This finding indicated that the audit committee may perceive conservatism as one of the mechanisms to restrict management opportunistic behaviour.

Mishra [2016] investigated audit committee characteristics and earnings management: Evidence from Indian. The study collected secondary data from 130 companies listed on the BSE over three years (2013 to 2015). The study adopted Univariate correlations, Multivariate Linear regression, and logistic regression models for analysis. The results of the study showed that there was a significant impact of audit committee size, multiple directorships, audit committee meetings on earnings management. However, there was an insignificant relationship between audit committee independence, audit committee expertise, and earnings management. The study concluded that the regulators and companies’ boards should continuously evaluate the efficacy of the audit committee and implement additional governance measures to preserve the integrity of the financial statement.

Baatwah, Ahmad, and Salleh [2016] assessed the influence of audit committee chair with financial expertise enhances the audit committee role in financial reporting quality in an emerging market. The study adopted the direct effect and moderating effect of audit committee chairs with financial expertise on financial reporting timeliness. The study collected Omani data and panel data while Descriptive statistics and Univariate were used for analysis. The study found that both accounting and non-accounting financial expertise has a positive and significant influence on the timeliness of financial reporting. The study documented associations between financial expertise and timeliness of financial reporting. It was suggested that financial expertise contributed when the chair of the audit committee has accounting expertise.

Miko and Kamardin [2015] investigated the impact of the audit committee and audit quality on earnings management prevention in pre and post-Nigerian corporate governance Code 2011. The study employed multiple regressions to assess the association between audit committees, audit quality, and discretion accruals in both periods. Modified Jones by Dechow, Sloan, and Sweeney [1995] was used to measure discretionary accruals. The proxies for the audit committee were audit committee financial expert, audit committee meetings, audit committee independence, and audit committee size. The study showed that audit committee size and audit committee meetings contributed to the reduction in accounts manipulation through discretionary accruals in pre- and post-Code 2011.

Madakawi [2012] conducted a study on the audit committee characteristics and financial reporting quality in Nigerian Listed companies. The study investigated the effect of audit committee characteristics on the quality of financial reporting of Nigerian-listed firms. The study made use of multivariate regression analysis with a sample of 101 firm-year longitudinal panels and 505 Nigerian non-financial listed companies from 2010 to 2014. The results of the study showed that control variables; company age, and company size are significant. The audit committee, share ownership and financial expertise was positively and statistically significant.

Methodology

The population of the study comprised all the twenty one (21) consumer goods firms listed on the Nigerian stock exchange website as of 2019. The judgmental Sampling technique was used to select ten (10) consumer goods firms. The sampling was based on 10 years of financial statements spanning from 2010 to 2019 to make valid conclusions. The study relied on secondary data and the data was sourced from the publication of the Nigerian Stock Exchange (NSE) and Annual Report and Accounts of the listed consumer goods firms as well as their respective notes to the accounts.

Model Specification

The general form of the panel data analysis for the regression models used to explain the audit committee characteristics and earnings management in listed consumer goods firms is specified in equation 3.1.

ERM = f (ACS, ACIND, ACFE, ACM, FSIZ, LEVG), (1)

where ERMit –Earnings Management; ACSit – Audit Committee Size; ACINDit – Audit Committee Independence; ACFEit – Audit Committee Financial Expertise; ACMit – Audit Committee Meetings; FSIZit – Firm Size; LEVGit – Leverage; β0 – Constant; β1 – β6 – Coefficients of explanatory variables; εit – Error term.

Hence, the specific model for the study is as presented in equation as follows:

ERMit= β0+ β1 (ACS) it+β2(ACIND) it+β3(ACFE) it +

+ β4(ACM) it+β5(FSIZ) it+β6(LEVG) it+ εit. (2)

Operationalization of variables

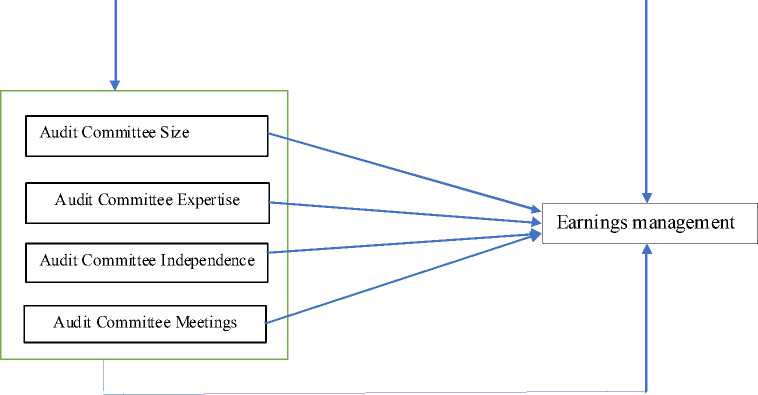

The study examines the relationship between audit committee characteristics and Earnings management in consumer goods firms in Nigeria. Earnings management is the dependent variables while the measurement for audit committee characteristics were audit committee size, audit committee expertise, audit committee independence and audit committee meeting (see Figure and Table 1).

The Modified Jones of discretionary accruals adopted to measure Earnings Management (ERM) is given as:

= Q it +

+ Р / AREVit aRECjt \ + ^ GPPE^ + , (3.1) V TAiT 1 / TAir 1 lr where Totals accruals – Net Operating Income minus Cash flow from Operating Activities; Qit – Constant; ΔREVit – Changes in revenue in the current year from the previous year; ΔRECit – Changes in receivables in the current year from the previous year; GPPEit – Gross property plant and equipment of firm in the current year; TA – Total Assets; ε – prediction error.

Audit Committee Characteristics Earnings Management

Figure. Researchers Operationalized Model

Note. Source: Researchers Operationalized Model (2021).

Table 1. Measurement of Variables

|

S/N |

Variables |

Variable types |

Measurement |

|

1 |

Earnings management |

Dependent |

Using Modified Jones of discretionary accruals by Dechow, Sloan and Sweeney, 1995 |

|

2 |

Audit Committee Size (ACS) |

Independent |

Number of audit committee members to the total of board members |

|

3 |

Audit committee independence (ACIND) |

Independence |

The percentage of independent non-executive audit committee members to the total audit committee members |

|

4 |

Audit Committee Financial Expertise (ACFE) |

Independence |

The percentage of audit committee members having expertise in accounting or auditing to the total number of directors in the audit committee |

|

5 |

Audit Committee Meetings (ACM) |

Independence |

The number of audit committee meetings held during the financial year |

|

6 |

Firm Size (FSIZ) |

Control Variable |

The Company’s natural log of total assets |

|

7 |

Leverage (LEVG) |

Control Variable |

Measured as the ratio of the company’s total liabilities to the company’s total assets |

Note. Source: Compiled by the authors.

After applying the modified Jones models, the abnormal accruals are the prediction error:

Abnormal accruals

Total Accurals it =---------------- -

Total Assetsit 1

—

( a+et

I

AREV it AREC it

TA it 1 TA it 1

+e it

PPE. J. (3.2)

TA i, J

Data estimation techniques

Appropriate inferential and descriptive statistics were adopted in this study. Correlation analysis, Ordinary Least Squares (fixed effect) with the aid of Eviews 10, regression was used to also determine the relationship between the identified independent variable proxies and dependent variable proxy.

Data Presentation, Analysis, and Discussion

The main objective of this study is to examine the effect of audit committee characteristics on the earnings management of listed consumer goods firms in Nigeria. This was achieved by assessing the annual reports of ten (10) selected firms in Nigeria.

The independent variable measurements were Audit Committee Size (ACS); Audit Committee Independence (ACIND); Audit Committee Financial Expertise (ACFE); Audit Committee Meeting (ACM); while the dependent variable is Earnings Management (ERM) measured with the Modified Jones Model of Discretionary Accruals and the study control variables consist of: Firm Size (FSIZ) and Leverage (LEVG).

Descriptive statistics

The values of standard deviation indicated the degree of dispersal of observed variables or clusters around individual means. The descriptive statistic results showed that most of the series considered in this study dispersed from their mean values. The table 2 showed the descriptive statistics for the seven variables for the period of 2010 to 2019.

The results of Kurtosis tests of earnings management, audit committee size, audit committee meeting, and leverage were leptokurtic as they were below 3 while audit committee financial expertise, audit committee independence, and firm size were platykurtic as they were above 3. The insufficiency of Kurtosis tests in defining the series distribution informed the Jarque-Bera normality test. Jarque-Bera test was further carried out to determine the normality of the series. The Jarque-Bera tests revealed that earnings management, audit committee size, audit committee independence, audit committee meeting were significant at 5% level which indicated that the series did not pass the normality test. However, audit committee financial expertise, firm size, and leverage were not statistically significant at the 5% level and showed that those series were normally distributed.

Unit Root Test

The study performed a unit root test on the series. The test revealed the stationarity of the series adopted as a model estimation. The stationarity was confirmed to prevent the model from being spurious and misleading and thereby suitable for the forecast. This is because the

Table 2. Descriptive statistics of Variables

|

ERM |

ACS |

ACIND |

ACFE |

ACM |

FSIZ |

LEVG |

|

|

Mean |

0.00000 |

5.92 |

0.43053 |

0.31007 |

3.69121 |

24.93452 |

0.57913 |

|

Median |

-0.01492 |

6 |

0.5 |

0.33 |

4 |

25.04485 |

0.57918 |

|

Maximum |

0.83542 |

6 |

0.5 |

0.67 |

6 |

27.60771 |

1.00009 |

|

Minimum |

-0.41225 |

4 |

0.17 |

0 |

1 |

22.41892 |

0.34018 |

|

Std. Dev. |

0.15108 |

0.39389 |

0.09009 |

0.16153 |

1.00197 |

1.098265 |

0.11827 |

|

Skewness |

1.46378 |

-4.69486 |

-0.72789 |

-0.02758 |

-0.80322 |

-0.40131 |

0.05064 |

|

Kurtosis |

11.51604 |

23.04162 |

2.23120 |

2.20387 |

3.64512 |

2.67006 |

3.44104 |

|

Jarque-Bera |

337.8893 |

2040.979 |

11.2932 |

2.65360 |

12.48681 |

3.13770 |

0.85322 |

|

Probability |

0.00000 |

0.00000 |

0.00353 |

0.26533 |

0.00194 |

0.20829 |

0.65272 |

Note. Source: Researcher’s computation with the aid of EVIEWS10.

stationary variables feature cannot change as time progresses.

Panel Regression Results

Table 4 presented the panel regression results. The panel covered the fixed and random effect estimations. The essence of this was to adopt the best estimator that gave the most consistent result. The result of the Hausman test showed that a fixed effect estimate was found appropriate and was interpreted for the study.

The R square is approximately 41.6% which showed that the independent variables in this model accounted for about 41.6% of the variation in the dependent variable. In other words, the explanatory ability of the model for the systematic variations in the dependent variable is 41.6%. The F-statistics of 3.992838 with p-value (0.000021) revealed that the model specification was fit at predicting earnings management (ERM). The implication of this is that the explanatory power of the model is strong as the independent variables significantly explained the dependent variable.

The regression results showed that Audit Committee Size (ACS) had a negative and statistically significant relationship with earnings

Table 3. Levin, Lin & Chu Unit root test

|

Variables |

Level |

Order of Integration |

||

|

Model I |

Model II |

Model III |

||

|

ERM |

-3.85373 |

-7.03577 |

-5.93834 |

I (0) |

|

(0.0001) |

(0.0000) |

(0.0000) |

||

|

ACS |

-0.32005 |

-2.80911 |

-0.26898 |

I (0) |

|

(0.3745) |

(0.0025) |

(0.3940) |

||

|

ACIND |

-0.27676 |

-0.1244 |

-3.6819 |

I (0) |

|

(0.1694) |

(0.1303) |

(0.0016) |

||

|

ACFE |

-1.63959 |

-2.60369 |

-0.16323 |

I (0) |

|

(0.0505) |

(0.0046) |

(0.4352) |

||

|

ACM |

-3.2327 |

-5.62455 |

-0.47282 |

I (0) |

|

(0.0006) |

(0.0000) |

(0.3182) |

||

|

FSIZ |

-5.63215 |

-5.95916 |

4.92924 |

I (0) |

|

(0.000) |

(0.0000) |

(1.0000) |

||

|

LEVG |

-4.85224 |

-4.93735 |

0.02044 |

I (0) |

|

(0.0000) |

(0.0000) |

(0.5082) |

||

Note. Source: Researcher’s computation with the aid of EVIEWS10.

Table 4. Regression Results

|

Variables |

Fixed Effect |

Random Effect |

|||

|

Coefficient |

t-statistics (Prob.) |

Coefficient |

t-statistics (Prob.) |

||

|

C |

1.097384 |

2.261309 (0.0263) |

0.713381 |

2.009813 (0.0473) |

|

|

ACS |

-0.03842 |

-6.38815 (0.0000) |

-0.042217 |

-2.826143 (0.0058) |

|

|

ACIND |

0.021608 |

0.124157 (0.9015) |

-0.174647 |

-0.991543 (0.3240) |

|

|

ACFE |

0.101809 |

0.727776 (0.4688) |

0.019391 |

0.254992 (0.7993) |

|

|

ACM |

-0.054003 |

-4.790285 (0.00000) |

-0.04056 |

-3.058247 (0.0029) |

|

|

FSIZ |

-0.024145 |

-1.299541 (0.1973) |

-0.011036 |

-0.620568 (0.5364) |

|

|

LEVG |

-0.189068 |

-2.182091 (0.0319) |

0.052771 |

0.453913 (0.6509) |

|

|

R-Squared |

0.416231 |

0.086536 |

|||

|

Adjusted R-squared |

0.311987 |

0.027602 |

|||

|

F-statistics |

3.992838 |

1.468368 |

|||

|

Prob (F-stat) |

0.000021 |

0.197612 |

|||

|

Durbin-Watson Stat |

2.478316 |

1.902074 |

|||

|

Test summary |

Chi-Sq. Statistics |

Chi-Sq. d. f. |

Prob. |

||

|

Cross-sectional random |

5.131517 |

3 |

0.1624 |

||

Note. Source: Researcher’s computation with the aid of EVIEWS10.

management (ERM) at a 5% level of significance, (β = -0.03842, p-value of 0.0000). This meant that a change in audit committee size has a significant effect on earnings management (ERM), specifically, a decrease in audit committee size by -0.03842 points leads to an increase in earnings management (ERM) by 1 unit and vice versa. Furthermore, Audit Committee Meetings (ACM) showed a negative and statistically significant relationship with Earnings Management (ERM) at a 5% level of significance, (β =-0.054003, p-value of 0.0000). Therefore, a change in audit committee meetings has a significant effect on earnings management (ERM). Specifically, an increase in audit committee meetings by -0.054003 points leads to a decrease in earnings management (ERM) by 1 unit and vice versa. The implication of the results showed that audit committee size and audit committee meetings contributed immensely to the reduction in accounts manipulation through earnings management.

The Audit Committee Independence (ACIND) showed a negative and statistically insignificant relationship with Earnings Management (ERM) at a 5% level of significance. (β = 0.021608, p-value of 0.9015). Therefore, a decrease in audit committee independence by 0.021608 points leads to an increase in earnings management (ERM) by 1 unit and vice versa. This negative association between audit independence and earnings management showed that audit committee independence contributed to the reduction of earnings management practices among the firms in a little manner. Audit Committee Financial Expertise (ACFE) showed a positive and statistically insignificant relationship with Earnings Management (ERM) at a 5% level of significance, (β = 0.101809, p-value of 0.4688). Therefore, a decrease in Audit committee financial expertise by 0.101809 points leads to a decrease in Earnings Management (ERM) by 1 unit and vice versa. The result indicated that audit committee financial expertise contributed in a little manner to the practices of earnings management among consumer goods firms in Nigeria.

Discussion

The study submitted that audit committee size, audit committee meeting, and audit committee independence influence earnings management practices among consumer goods firms in Nigeria. The result of this study is in line with the works of Juhmani [2017]; Miko and Kamardin [2015] who found that audit committee size has a negative and significant relationship with earnings management. Vafeas [2005] opined that a moderate size of the committee will be able to monitor the directors’ activities. It is believed that fewer committee members may not be sufficient to perform a good job, and the larger committee may also perform poorly because of poor coordination and weak monitoring. Furthermore, auditors’ independence is an ethical issue when discussing audit committee assignments like earnings management. The audit committee relates to the legislative arm of government that upholds the laws with objectivity. The study finding is also in line with the study of Siagian and Siregar [2018] who found a positive and insignificant association between audit committee financial expertise and earnings management but contrary with Juhmani [2017] that found a negative association between the variables. Financial literacy helps audit committee members to identify unethical practices in the financial statement prepared.

Furthermore, the result of the study is similar to the study of Juhmani [2017] who found a negative and insignificant association between audit committee independence and earnings management. Also, the study complied with the works of Mishra [2016] who submitted that there is no significant association between audit committee independence and quarterly discretionary accruals, however contrary to the study of Baatwah, Ahmad, and Salleh [2016].

Finally, the result of the study is in agreement with the study of Mishra [2016] who found a significant and negative association between audit committee meetings and earnings management practices which are in line with the decisions made in this study. It is concluded that the frequency of meetings by the audit committee plays a huge role in reducing the possibility of earnings management practices among consumer goods firms. For example, new issues arise in interim and final audit and these cases would have come up and resolved in regular audit committee meetings as, without frequent meetings, it is unlikely that suitable policies will be formulated on how to checkmate the activities of managers, accountants, or even CEO(s) who may want to involve in unethical practices.

Conclusion and Recommendations

The study examined the effects of audit committee characteristics on earnings management in listed consumer goods firms in Nigeria, using a sample of ten (10) consumer goods firms in Nigeria from 2010 to 2019. The study concluded that audit committee attributes are germane to the reduction and moderation of earnings management among Nigerian listed consumer goods firms. In line with the findings of this study, the study recommended that shareholders and regulatory authorities responsible for the selection of audit committee members should ensure adequate membership, also ensures that at least one member of the audit committee is financially literate, hold at least four meetings within a financial year. Finally, the regulatory authority should enforce strict compliance with the codes of companies’ laws on matters relating to audit committee composition. The regulatory agencies in Nigeria should increase surveillance on audit committee composition among Nigerian listed consumer goods firms to reduce opportunities for managers and others who may wish to engage in earnings management.

References Impact of audit committee characteristics on earnings management in Nigerian listed consumer goods firms

- Abbott L.J., Parker S., Peters G.F. Audit Committee Characteristics and Restatements. Auditing: Journal of Practice & Theory, 2004, 23 (1), pp. 69-87

- Ayinde I. Audit Committee: History and Evolution. National Seminar on Enhancing Audit Committee Effectiveness, 2002, pp. 257-271.

- Baatwah S.R., Ahmad N., Salleh Z. Audit Committee Financial Expertise and Financial Reporting Timeliness in an Emerging Market: Does Audit Committee Chair Matter? Issues in Social and Environmental A ccounting, 2016, 10 (4), pp. 63-85.

- Bala H., Kumai G.B. Board Characteristics and Earnings Management of Listed Food and Beverages Firms in Nigeria. European Journal of Finance and Accounting, 2015, 9 (1), pp. 11-31.

- Bryan D., Liu C., Tiras S.L. The Influence of Independent and Effective Audit Committees on Earnings Quality. SSRN Electronic Journal. DOI: 10.2139/ssrn.488082.

- Contessotto C., Moroney R. The Association Between Audit Committee Effectiveness and Audit Risk. Accounting and Finance, 2013, 54 (2), pp. 393-418.

- Dechow P.M., Sloan R.G., Sweeney A.P. Detecting Earnings Management. The Accounting Review. S. l., American Accounting Society, 1995, 70 (2), pp. 193-225.

- Eisenhardt K.M. Agency Theory: An Assessment and Review. Academy of Management Review, 1989, vol. 14, no. 1, pp. 57-74. DOI: 10.2307/258191.

- Ibrahaim M.A. Effects of Characteristics of the Audit Committee on Earnings Management in Nigeria Quoted. Sokoto Journal of Management, 2016, 10 (1), pp. 140-141.

- Jensen M.C., Meckling W.H. Theory of the Firm: Managerial Behavior, Agency Costs, and Ownership Structure. Journal of Financial Economics, 1976, 3 (4), pp. 305-360.

- Juhmani O. Audit Committee Characteristics and Earnings: The Case of Bahrain. International Journal of A ccounting and Financial Reporting, 2017, vol. 7, no. 1, pp. 11-31. DOI: 10.5296/ijafr.v7i1.10447.

- Klein A. Audit Committee, Board of Director Characteristics, and Earnings Management. Journal of Accounting and Economics, 2002, 33 (3), pp. 375-400. DOI: 10.1016/S0165-4101(02)00059-9.

- Madakawi A. Audit Committee Characteristics and Financial Reporting Quality: Evidence from Nigerian Listed Companies (Doctoral dissertation, Universiti Utara Malaysia), 2012, p. 42.

- Menon K., Williams J.D. The Use of Audit Committees for Monitoring. Journal of Accounting and Public Policy, 1994, 13 (2), pp. 121-139.

- Miko N.U., Kamardin H. Impact of the Audit Committee and Audit Quality on Preventing Earnings Management in Pre- and Post-Nigerian Corporate Governance Code 2011. Procedia-Social and Behavioral Sciences, 2015, 172, pp. 651-657.

- Mishra M. Audit Committee Characteristics and Earnings: Evidence from India. International Journal of Accounting and Financial Reporting, 2016, 6 (2), pp. 247-249. DOI: http:// dx.doi.org/10.5296/ijafr.v6i2.10008.

- Nelson S.P., Jamil N.N. An Investigation on the Audit Committee's Effectiveness: The Case for GLCs in Malaysia. 2nd Accounting Research Education Conference (AERC), 2012. URL: ssrn. com/abstract=2020184.

- Olabisi J., Kajola S.O., Abioro M.A., Oworu O.O. Determinants of Audit Quality: Evidence from Nigerian Listed Insurance Companies. Journal of Volgograd State University. Economics, 2020, vol. 22, no. 2, pp. 182-192. DOI: https://doi.org/ 10.15688/ekjvolsu.2020.2.17.

- Siagian D., Siregar S.V The Effect of Audit Committee Financial Expertise and Relative Status on Earnings Management: Case of Indonesia. Jurnal RisetAkuntansi Indonesia, 2018, 22 (3), pp. 321-336.

- Vafeas N. Audit Committees, Boards, and the Quality of Reported Earnings. Contemporary Accounting Research, 2005, 22 (4), pp. 10931122.

- Xie B., Davidson W.N., Dadalt P.J. Earnings Management and Corporate Governance: The Role of the Board and the Audit Committee. Journal of Corporate Finance, 2003, 9 (3), pp. 295-316.